Bitcoin (BTC) holds the $40,000 mark. As the market consolidates again, the spending behavior of participants indicates a willingness to accumulate and save BTC without suggesting a bullish bias. With a third of the supply in a state of latent loss, selling pressure is non-negligible and a more pronounced price decline is not an impossible scenario. On-chain analysis of the situation

Bitcoin holds $40,000 mark

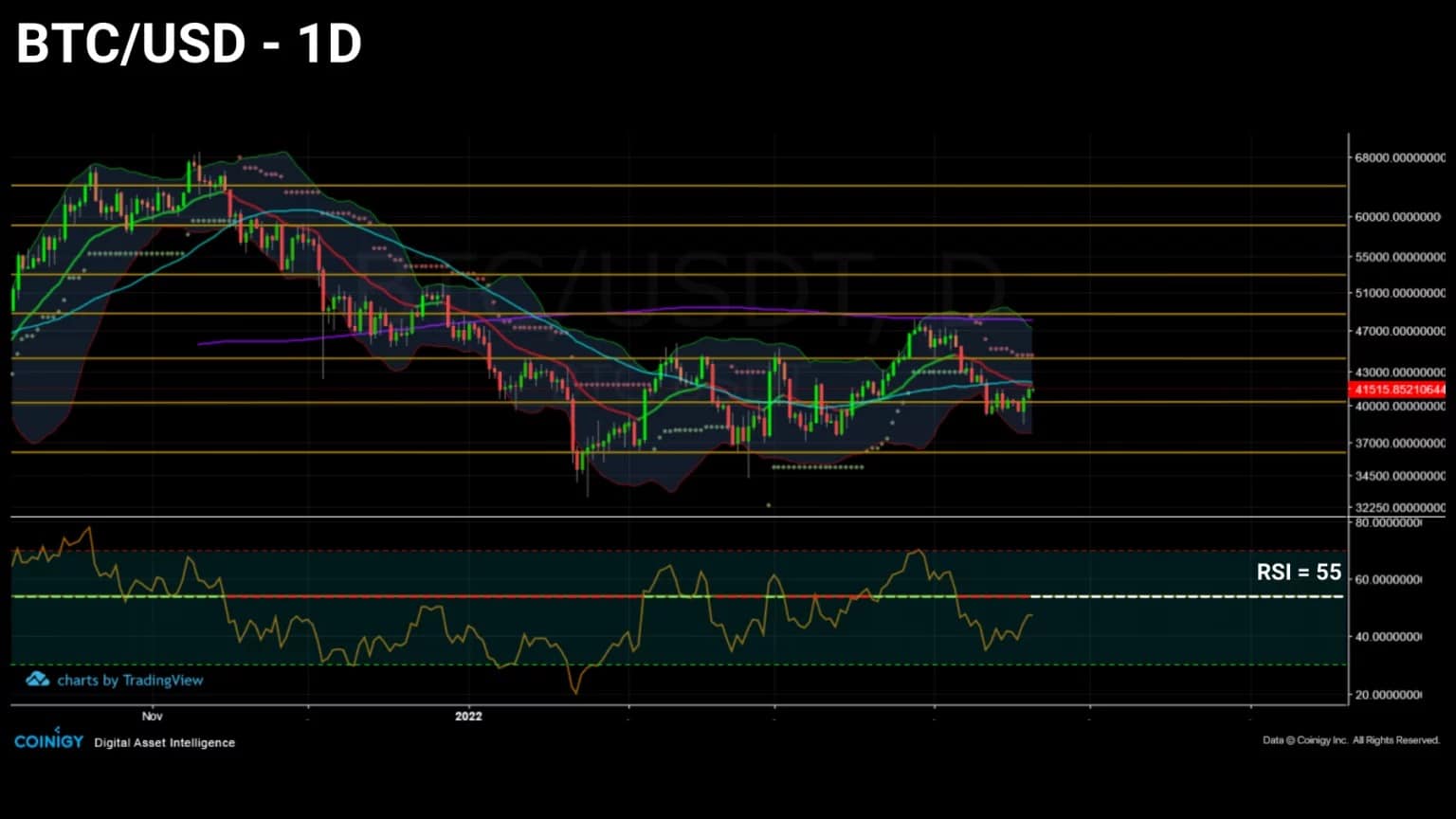

The price of Bitcoin (BTC) is hovering around the $40,000 support and adopting a particularly indecisive price structure.

In a state of consolidation throughout the first quarter of 2022, bitcoin is however printing successive higher and higher lows, casting doubt on its short and medium term trend for many investors.

Figure 1: Daily Bitcoin (BTC) price

This week we look at the life of spent BTC and then the state of profitability for investors in the short and long term before looking at network security and the behaviour of the mining cohort.

Spending age drops

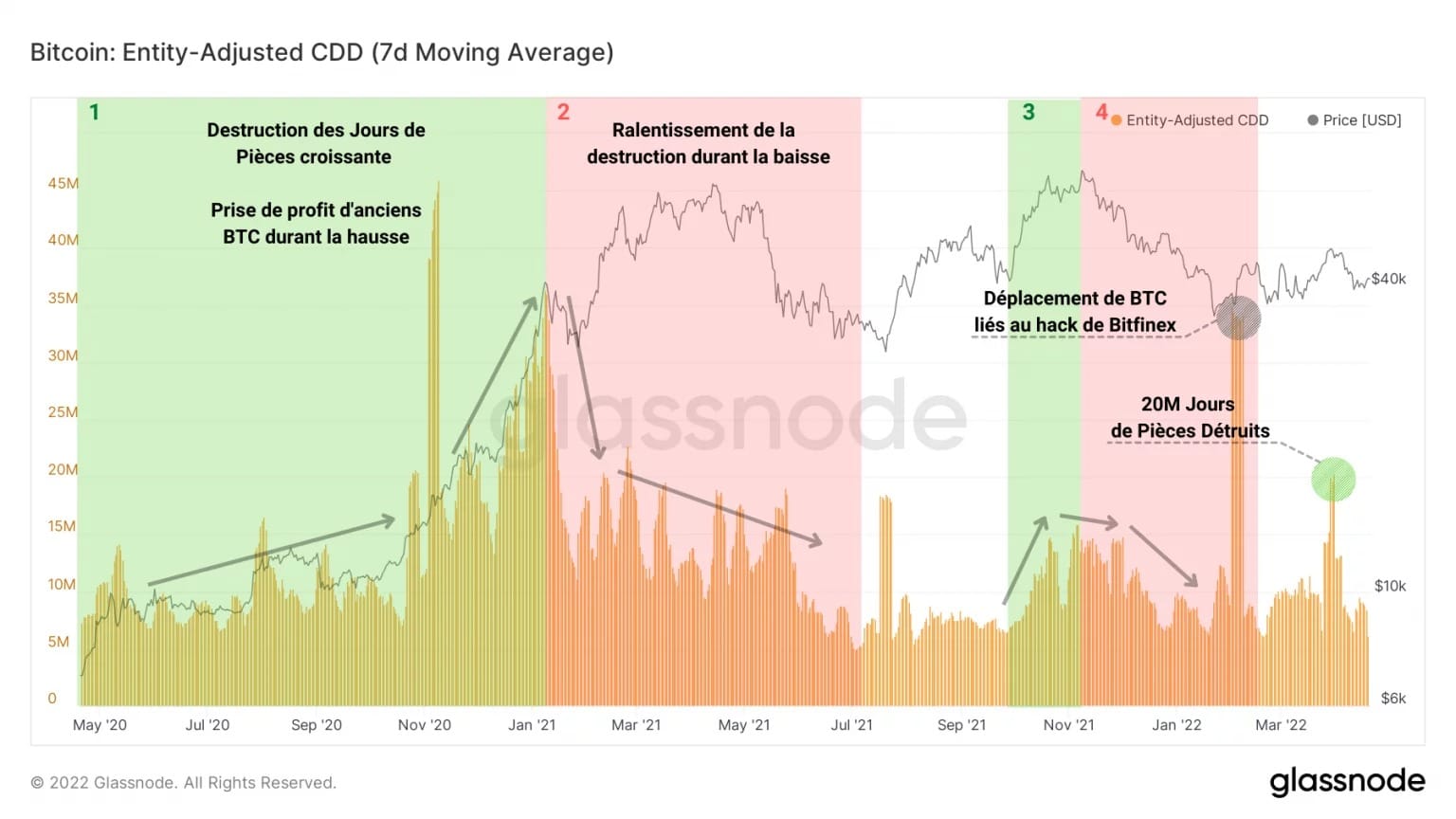

Let’s begin this analysis by looking at the Coin Days (CD) count destroyed in recent weeks.

Particularly effective in identifying the spending behaviour of seasoned investors and HODLers, the chart below distinguishes two distinct spending phases:

- periods of high JP destruction (green) indicate that old BTC are spent for profit and serve as catalysts in bull markets;

- periods of low JP destruction (red) indicate rejuvenation of spending and savings behaviour by long term investors.

Figure 2: Destroyed Coin Days

We can see that in recent months, the downward trend in JP destruction has moderated. Furthermore, during the recent rise that brought BTC back to the $50,000 mark, a peak of 20 million JP destruction appeared, indicating moderately aged spending.

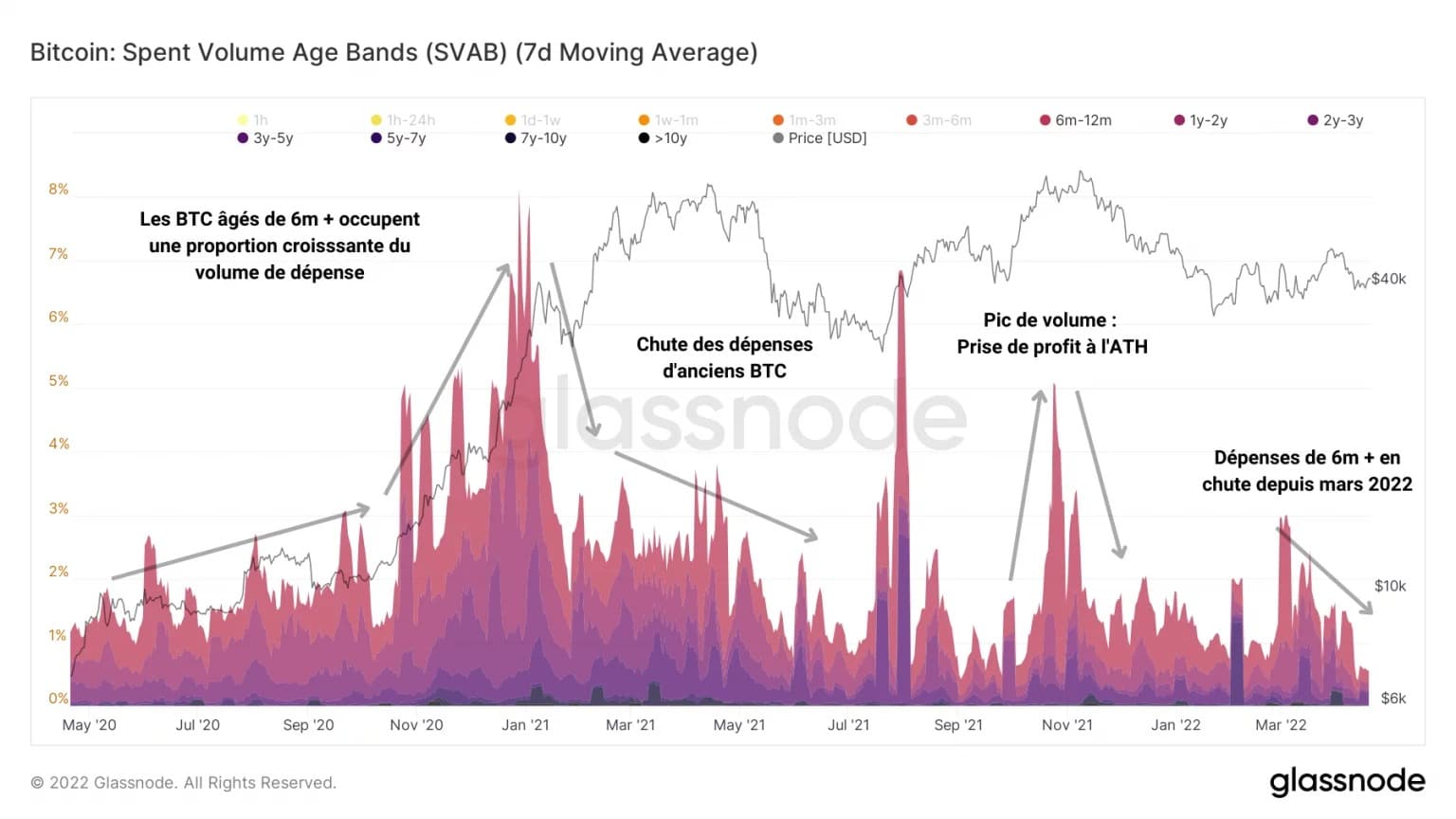

The same behavioural pattern can be seen on the Spent Volume Age Bands (SVAB) chart, where it can be observed, however, that spending of bitcoins older than 6 months has been steadily declining since March 2022.

Figure 3: Age bands of spent volume (SVAB)

It seems, therefore, that the above-mentioned peak in destruction is an isolated spending phenomenon and does not yet constitute a global trend involving a large number of investors.

By referring to the average age of UTXO spent, known as ASOL, we can further support this thesis. ASOL is a life indicator that works as follows:

- high values and increases indicate that the average age of spending is high, indicating that long-term investors are spending their assets;

- low values indicate that the majority of UTXO spent are young and immature.

Figure 4: Average age of UTXO spent (ASOL)

We thus find a similar rise in ASOL at the end of 2020 and the beginning of 2021, followed by a steady decline in peaks indicating an absence of an identifiable upward spending pattern.

Corroborating the above, liveliness, defined as the ratio of the sum of JP destroyed to the sum of all JP ever created, continues to fall, indicating that hoarding remains the dominant behaviour within the market.

Figure 5: Liveliness

One third of the market in a state of loss

Let’s turn to the metrics relating to the profitability of the market and its cohorts. These are essential tools for gauging the extent of selling or buying pressure, but also the reactions of investors to market stimuli.

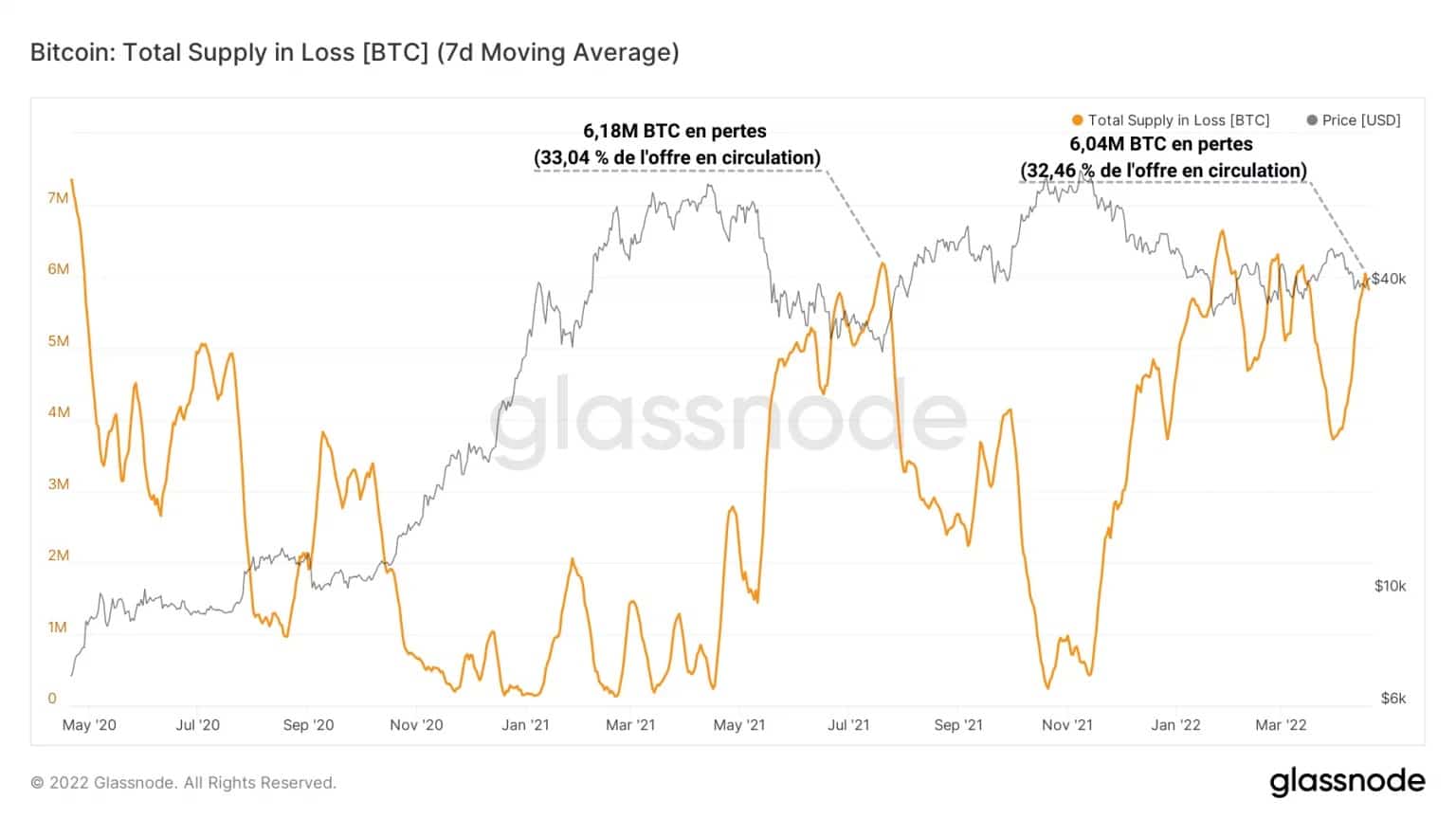

Let’s start by highlighting a salient fact: the supply of BTC in circulation estimated to be in a loss-making state (and therefore more likely to be spent) is now almost similar to that recorded during the final decline of the May-June 2021 capitulation.

Figure 6: Lossy supply

With nearly 6 million BTC in a state of latent loss (one third of the BTC in circulation), the market is currently under strong potential selling pressure, although its structure is significantly different.

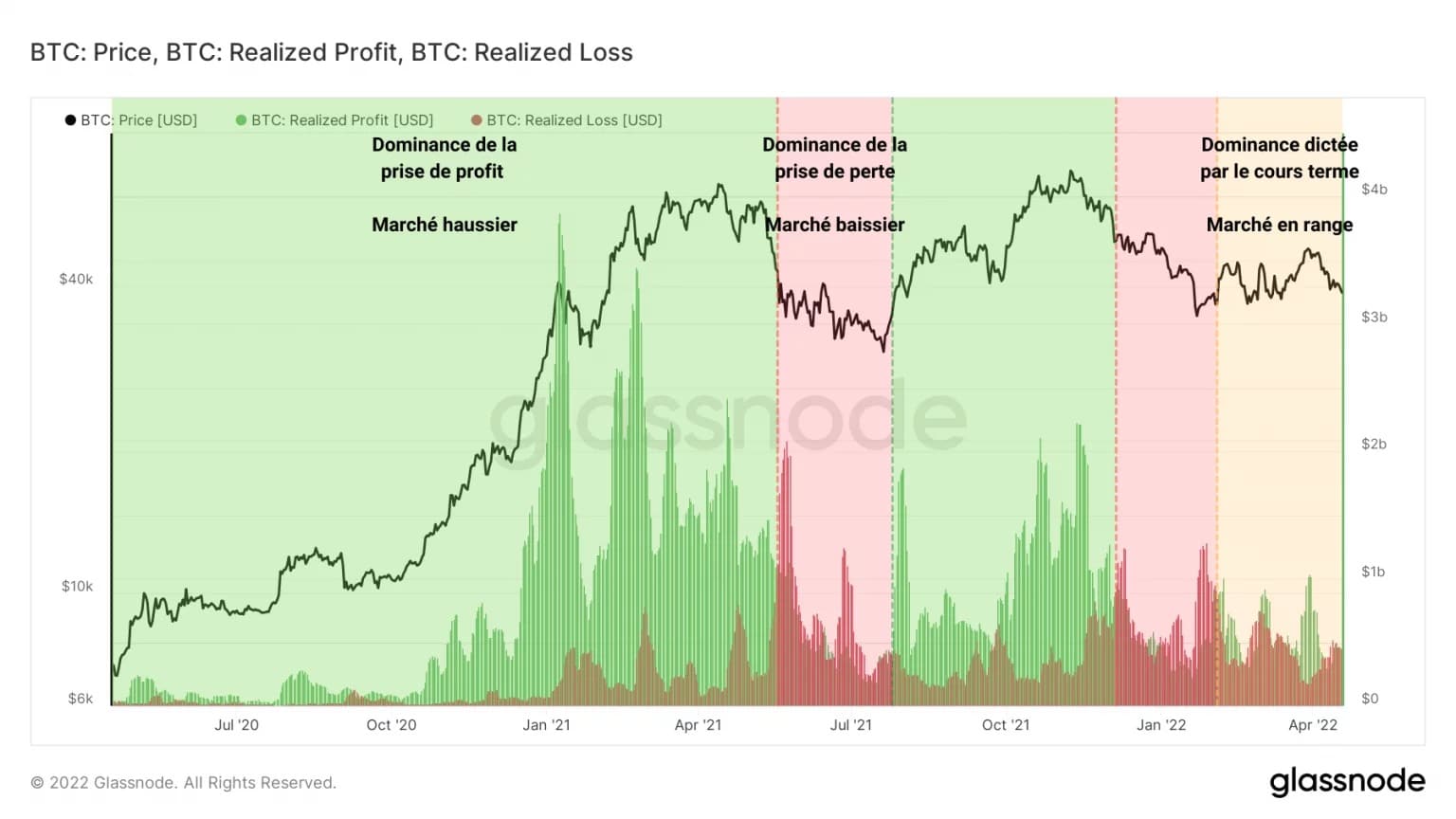

Indeed, tracking realized gains and losses clearly indicates that the current period (yellow) is not dominated by selling, as was the case in May-June 2022 (red).

Figure 7: Realised Losses and Profits

Back in the range state, short-term price action thus exacerbates profit and loss taking, providing a catalyst for both buying and selling pressure.

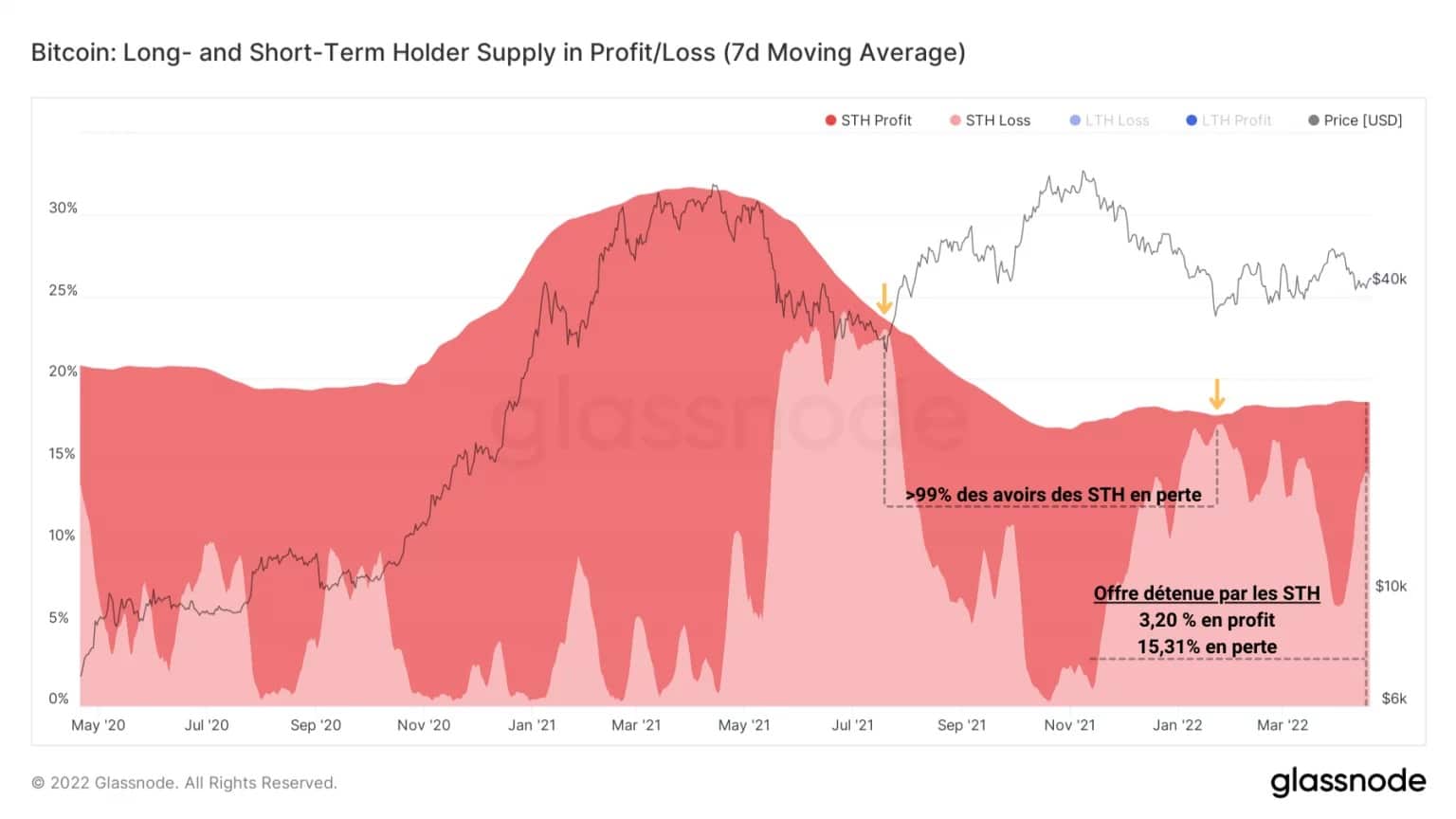

On the side of short-term investors (STH), volatility-sensitive participants, the unrealized loss state still largely dominates, but has not reached the level of pain (☻99% of cohort holdings in losses) experienced during final declines, a sign that a price drop cannot be ruled out.

Figure 8: Supply held in Loss or Profit by STH

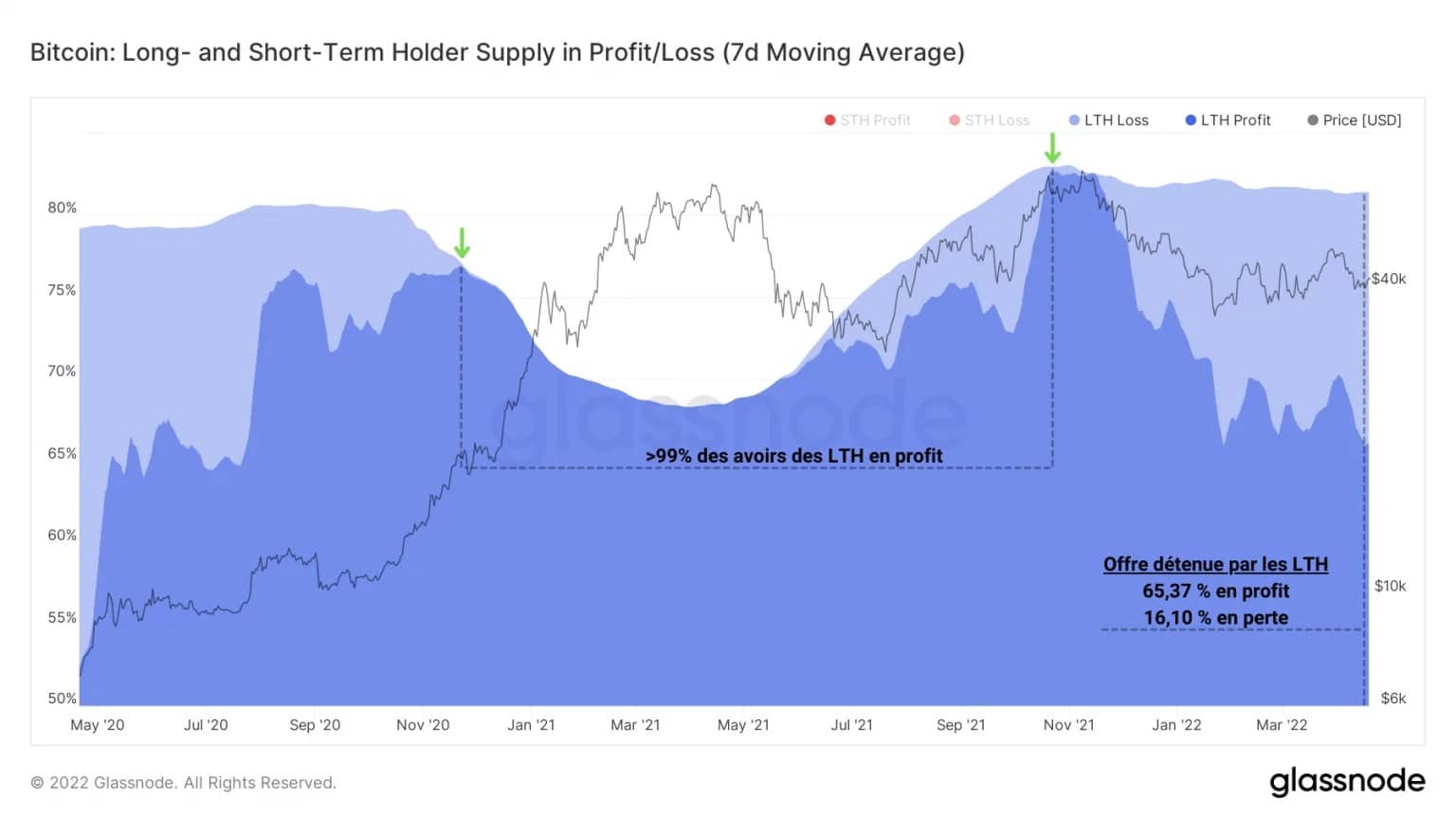

Long-term investors (LTHs), while predominantly profitable, share a similar portion of the supply in loss status (15% to 16%) with STHs. They are, however, less likely to spend their BTC on a decline, preferring HODL and accumulation behaviour.

Figure 9: Supply held in Loss or Profit by LTH

The state of the market’s profitability remains unalarming, with less than half of the supply at a loss and LTHs unlikely to sell. If a price drop were to occur, the short-term behaviour of STHs would provide direction for the next few days.

Miners await next bull market

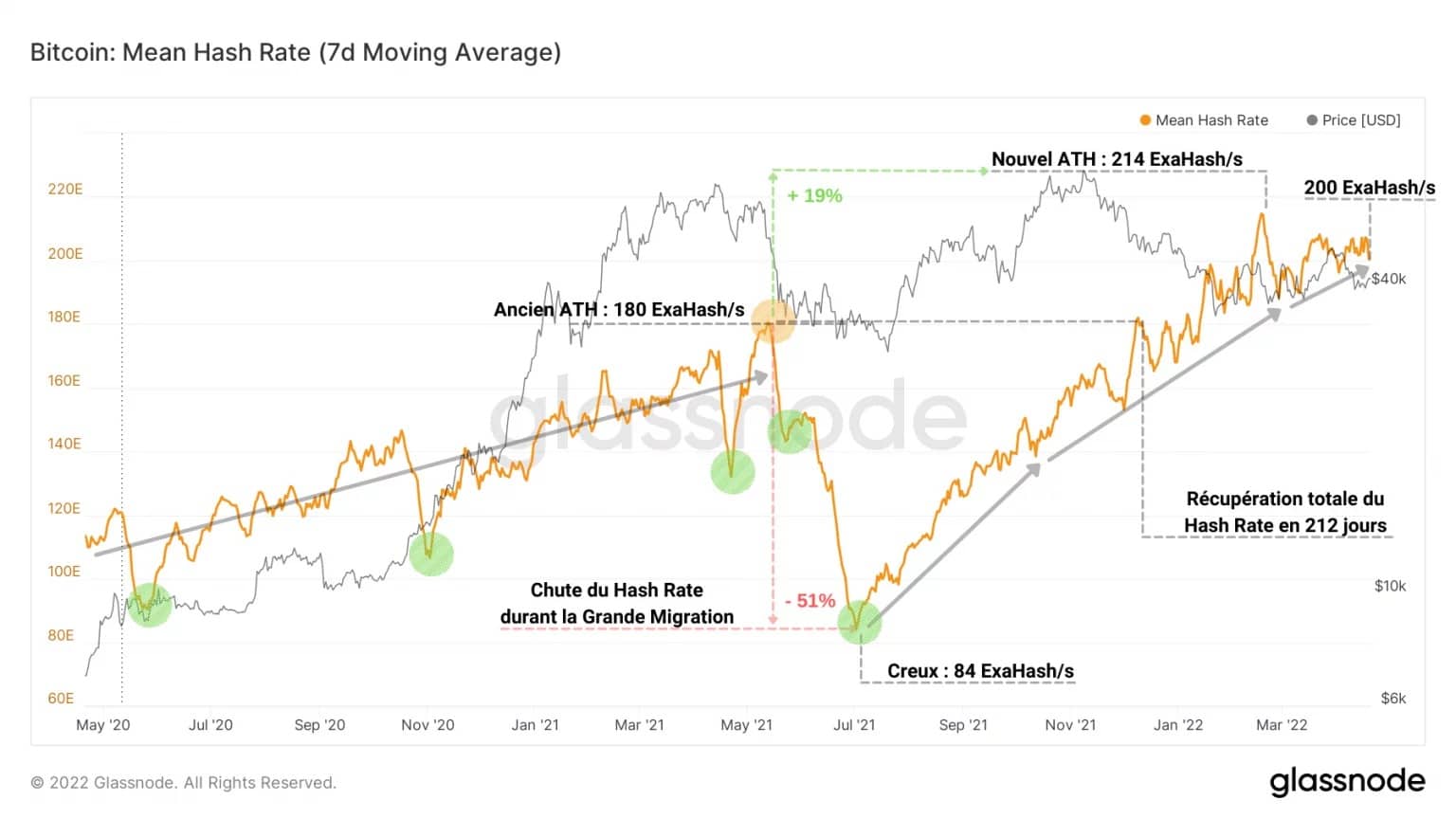

As far as the Bitcoin network is concerned, the weather is good. The computational capacity needed to forge a block has reached 200 Exahash, ensuring high network security by miners now recovered from the Great Migration related to China’s mining bans.

Figure 10: Hash Rate

The Minage Pulse, which calculates the difference between the 14-day average block interval and the 10-minute target time, is oscillating near its neutral zone.

The values of this oscillator can be interpreted as the number of seconds of acceleration (negative) or deceleration (positive) of mined blocks relative to the target block time of 600s.

Figure 11: Mining Pulse

We can easily identify periods of slowdown (green), directly related to the hashrate drop. This usually occurs when the hashrate slows down more than the difficulty adjustments, and indicates that miners are disconnecting, explaining the peak experienced in July 2021.

It thus appears that the Bitcoin network, both in terms of security and pace, is performing healthily, despite on-chain activity far from the levels seen during bull markets.

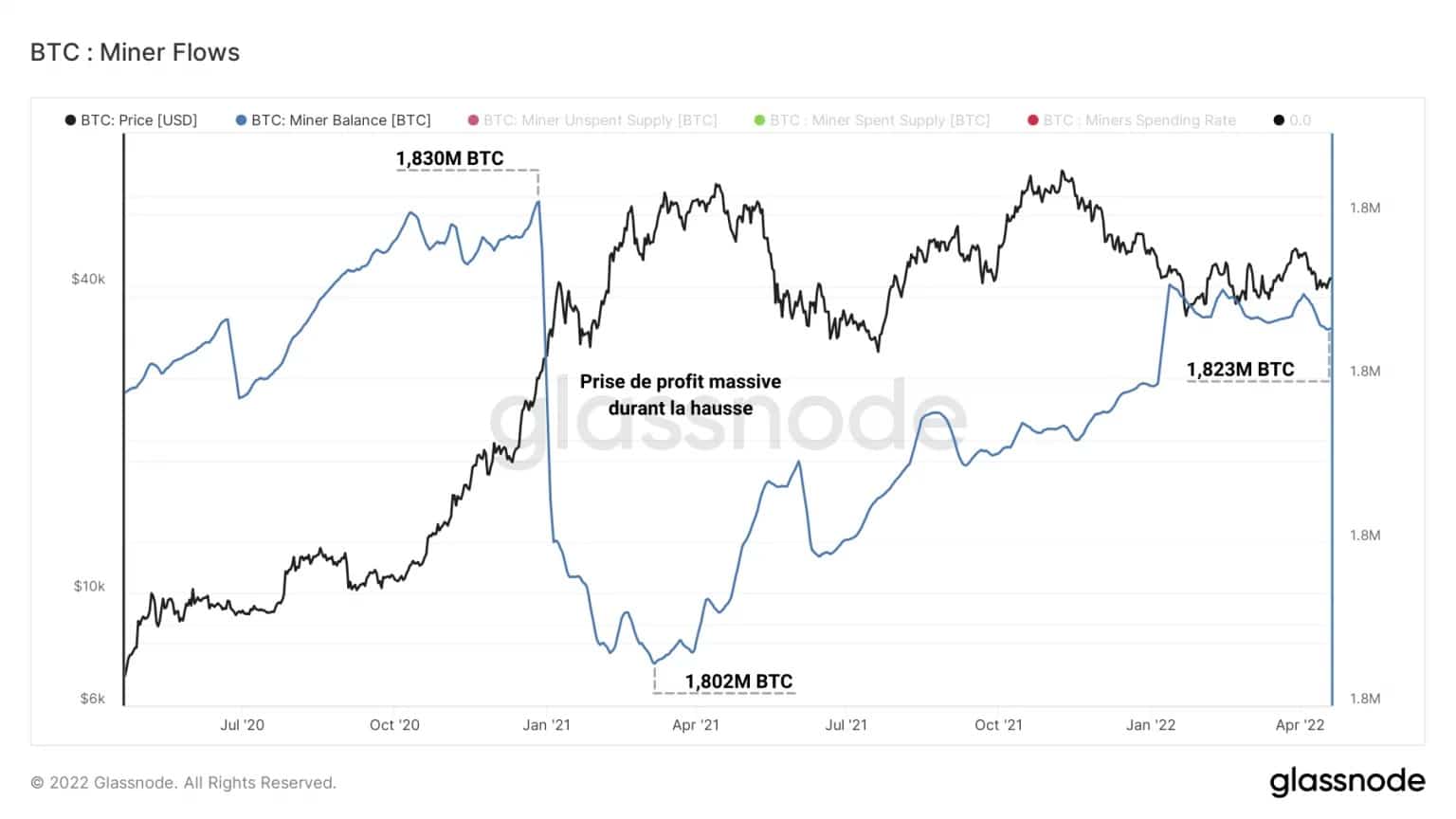

Figure 12: Miners’ Reserves

The Miners cohort has been very conservative since the November 2021 ATH. After a coordinated profit taking of almost 30,000 BTC between January and April 2021, these entities, known to be both compulsive sellers for OPEX spending and high conviction HODLers, are being cautious at best.

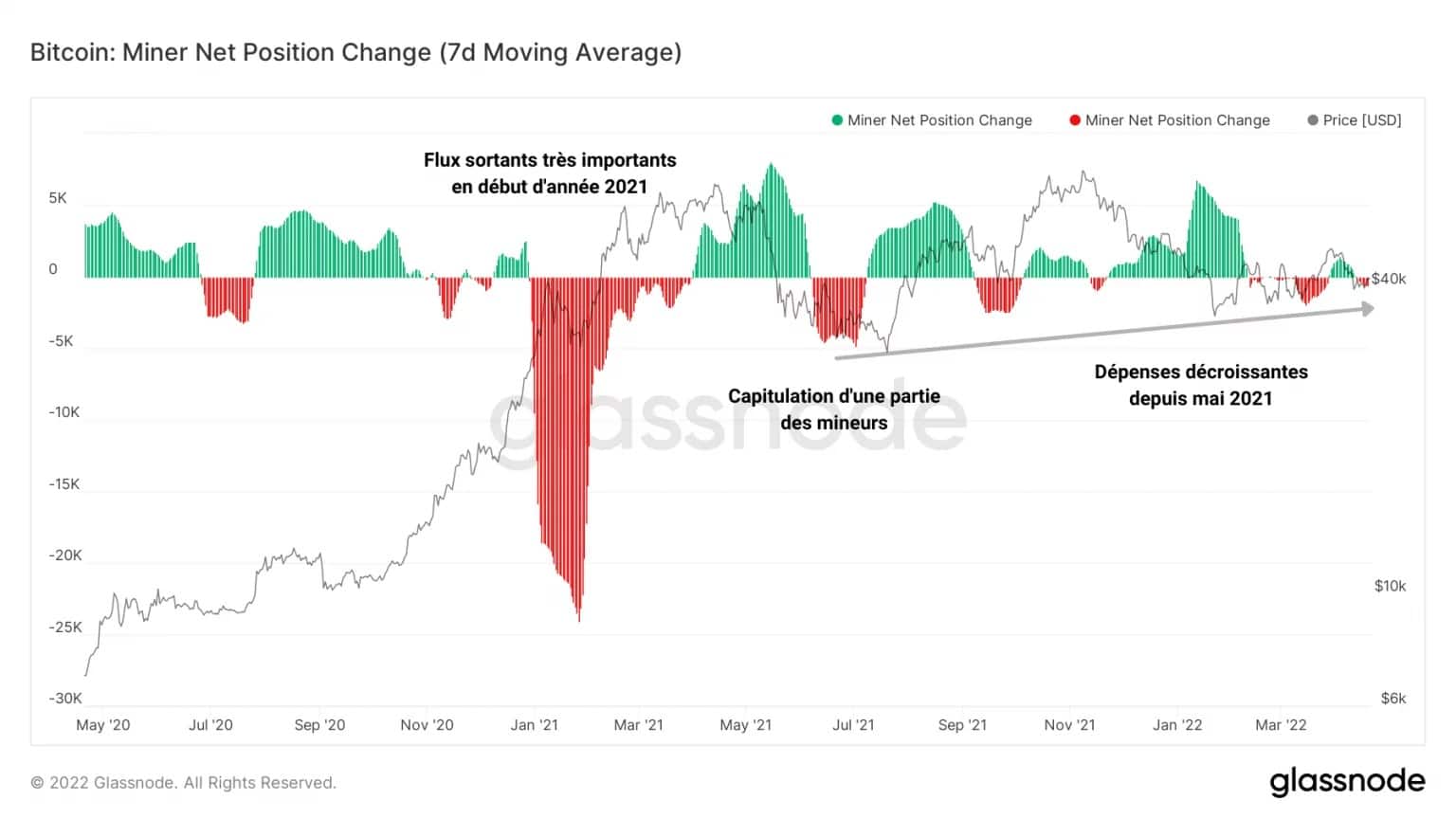

Indeed, the Miners’ Net Position Change, calculated as the monthly average of net flows associated with the portfolios of this cohort, shows strong outflows in early 2021 linked to high token destruction, a sign of profit taking.

Figure 13: Change in Net Position of Miners

A minor portion of these participants then succumb to selling pressure in July 2021, forced to liquidate a portion of their savings in order to cover their travel and settlement costs following the Chinese exodus.

This is followed in September 2021 by a steady decline in miners’ spending, reflecting savings behaviour, in anticipation of a new bull market structure in which the cohort will once again realise the profits of BTC from block reward.

Summary of this on-chain analysis

Finally, the market is approaching an indecisive structure, with no particular willingness to spend on the part of LTHs or miners.

The age of spent BTC indicates that accumulation and saving behaviour still dominates, a sign of a cautious investor bias.

With still a third of the supply in a loss-making state, evenly split between STH and LTH, the potential selling pressure is not alarming although a capitulation event is not out of reach.

Finally, the security of the Bitcoin network and the pace of block releases indicate a healthy fundamental, operated by miners unwilling to sell their tokens at such price levels.