Bitcoin (BTC) ends January on an optimistic note. While it is too early to seriously declare that a reversal is underway, many indicators suggest that the market is preparing for one by adopting a structure opposite to that of late 2021. On-chain analysis of the situation

Bitcoin is gaining strength

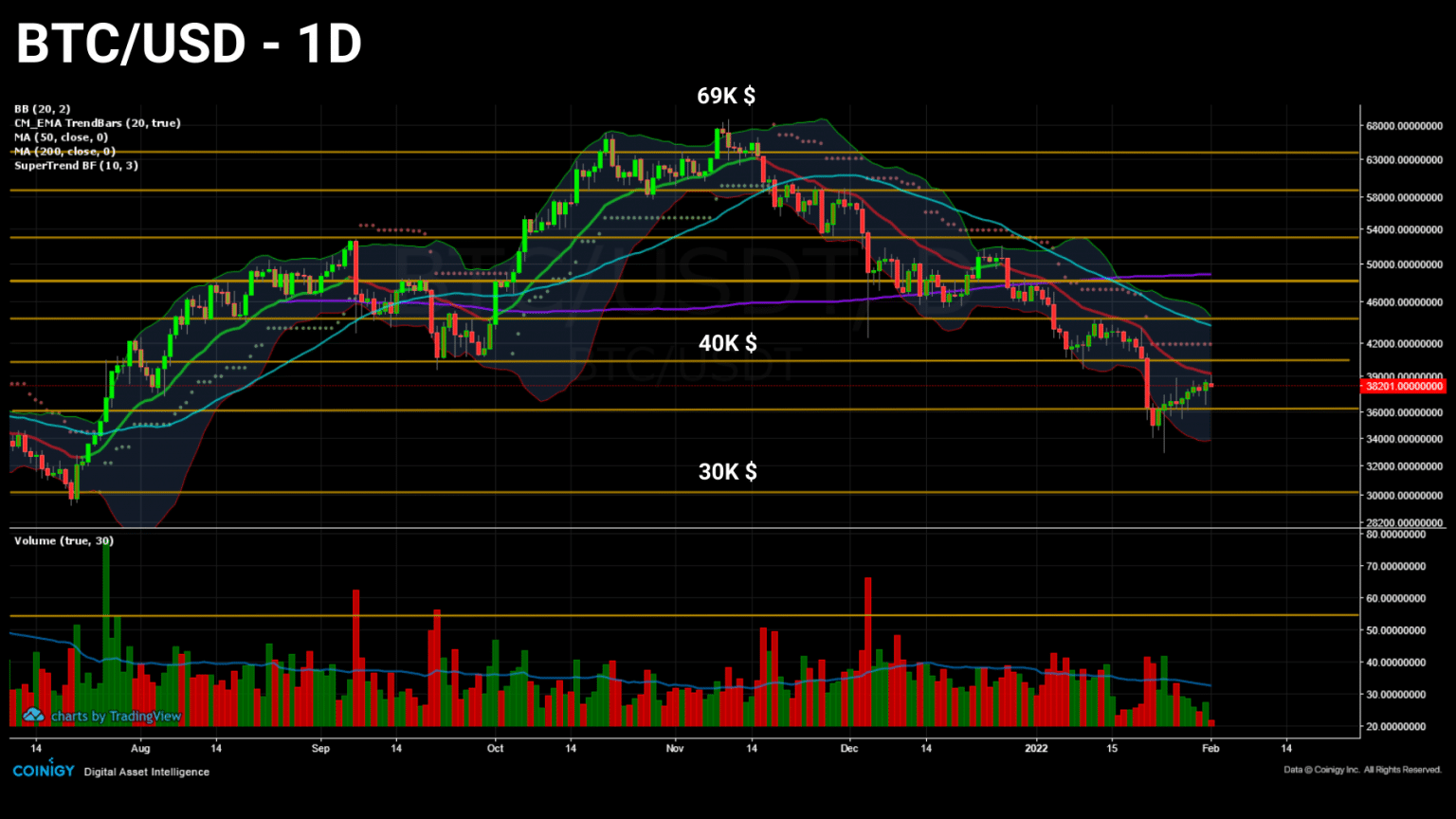

The Bitcoin (BTC) price closes January with a week of gradual gains and prints a monthly candle above $35,000.

On its way to test the $40,000 resistance, the Bitcoin price is still below the EMA 21, the first technical indicator to be breached before a bull market recovery can be considered.

Daily Bitcoin Price Chart

Nevertheless, signs of a trend reversal are gradually forming and point to a February that will be crucial for the long-term direction of the crypto-currency market.

Again this week, we will be watching a broad spectrum of indicators in an effort to identify the beginnings of a future move based on:

- the sustained buying behaviour of various cohorts;

- growth in transfer volume on the channel;

- the emergence of bearish speculative positions;

- the bullish divergence of the realised gradient.

A very attractive buying area

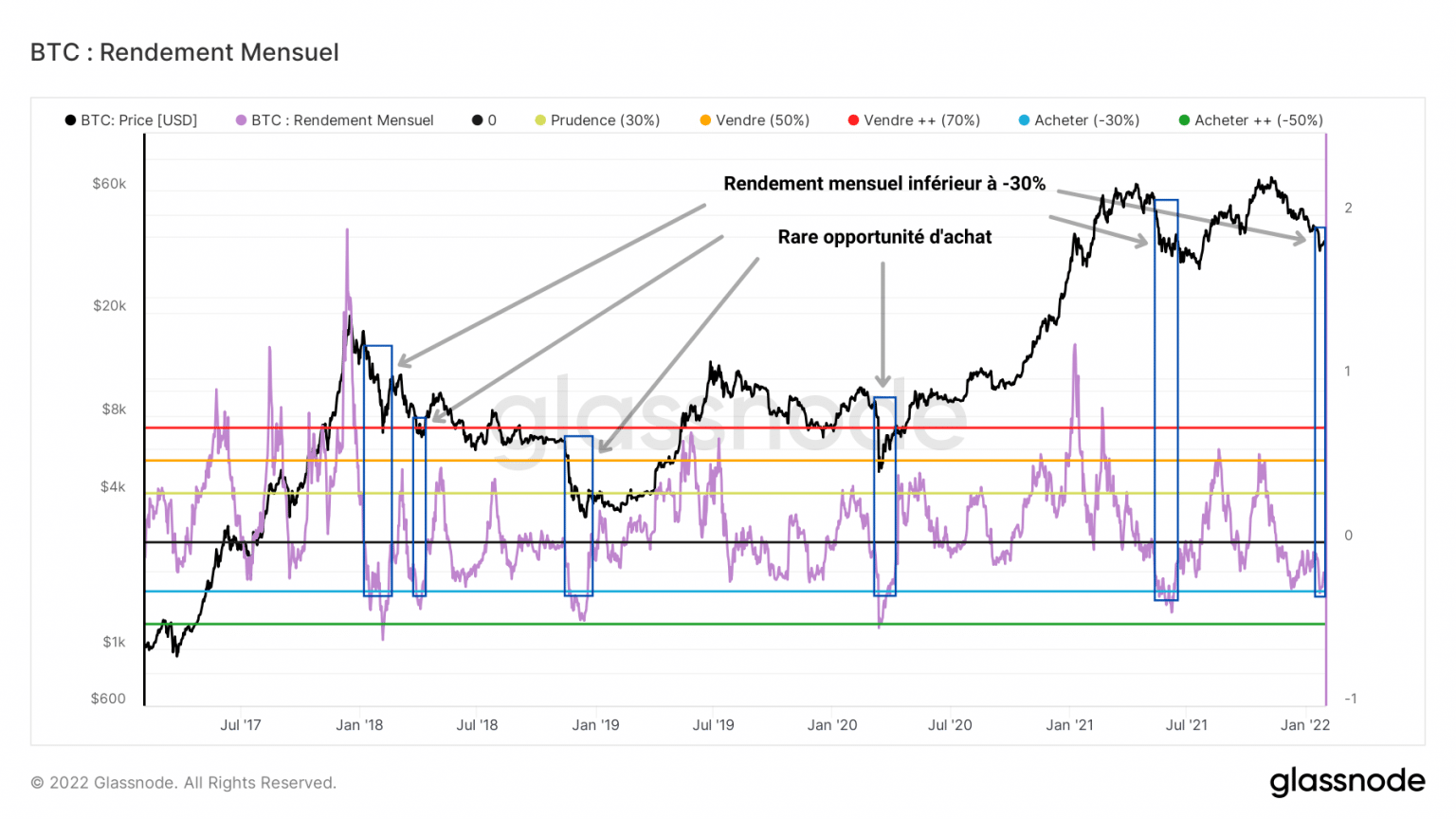

To set the scene, let’s start by noting that, from a monthly perspective, BTC is within a significant buying zone. At just -50% of its ATH, the asset is trading at a value sufficient to generate visible interest.

Since the peak of the 2017 parabolic phase, a monthly return below -30% is a rare event, occurring only six times in the space of four years.

Bitcoin monthly return chart

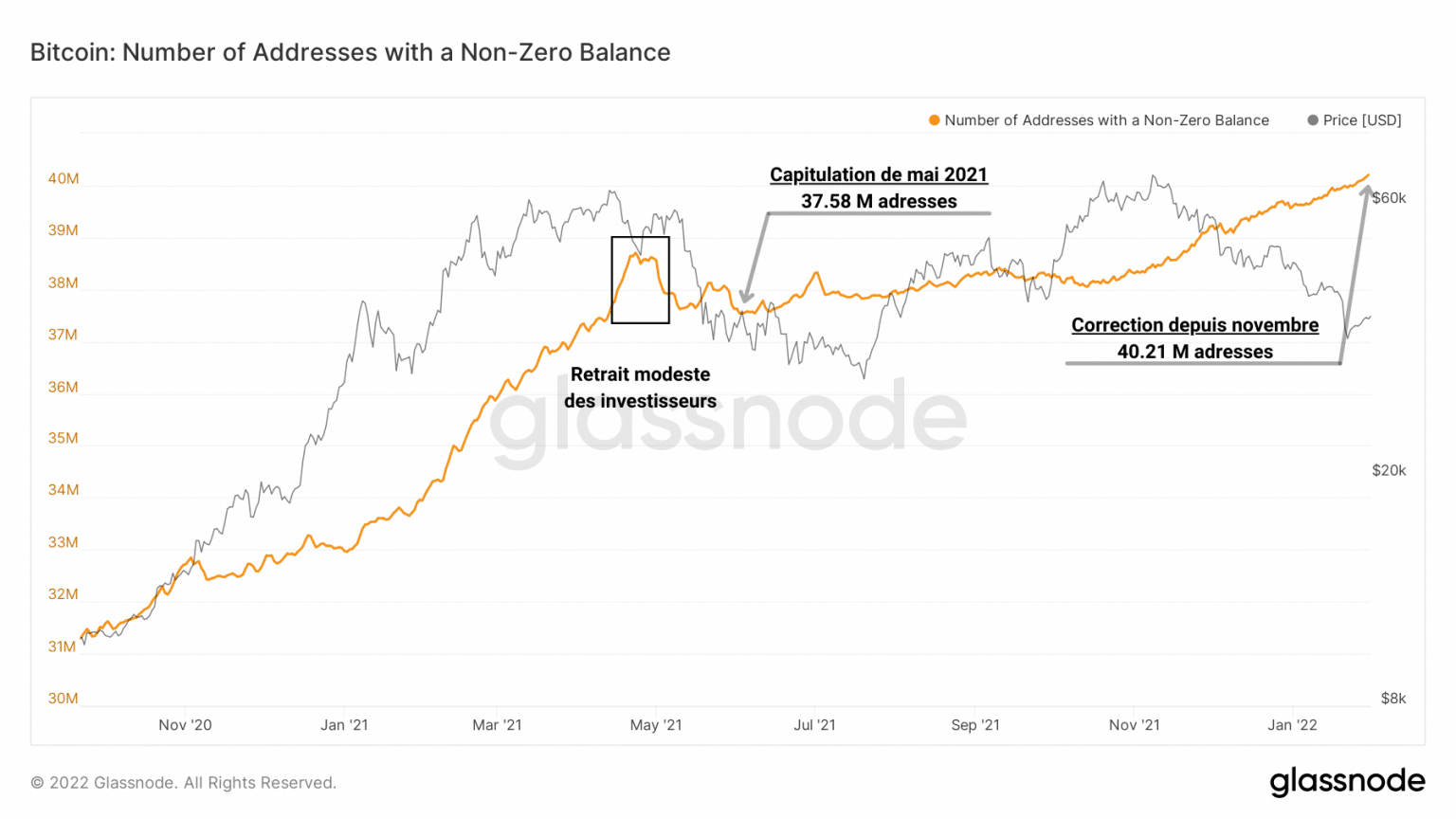

It is in this regard that many participants have taken advantage of the ongoing 77-day correction to accumulate ever more bitcoins at low prices.

Judging by the continuous increase in the number of BTC addresses with a non-zero balance since May 2021, this decline has not prevented investors from piling up satoshis, notably via dollar cost averaging strategies.

Chart of bitcoin’s non-zero balance address account

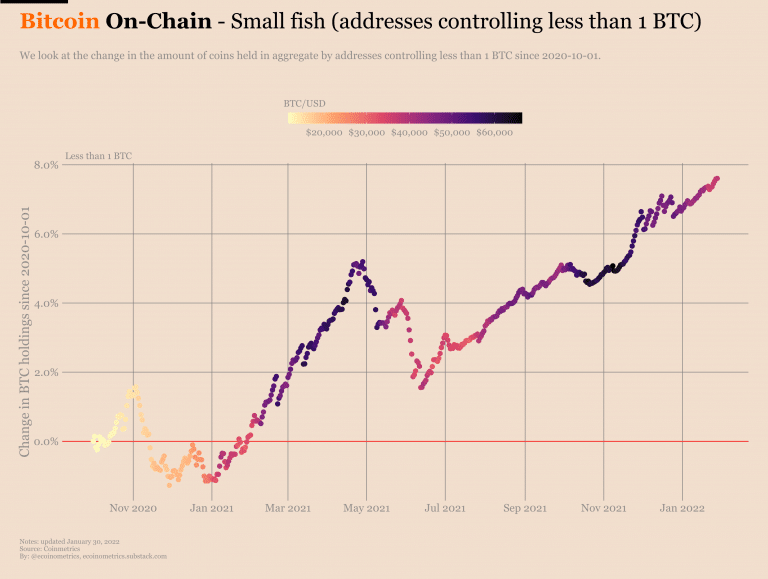

Indeed, Ecoinometrics data reports that significant buying – and even saving – behaviour is taking place behind the scenes.

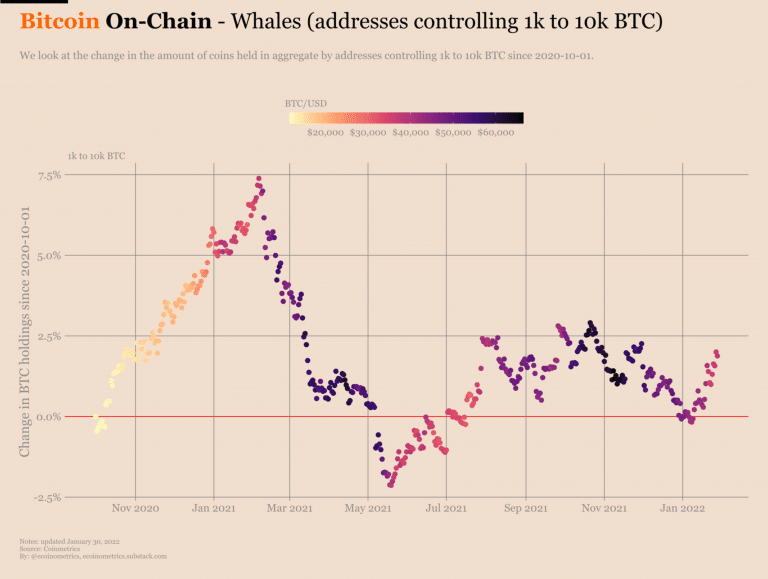

Not only are addresses controlling less than 1 BTC steadily increasing, but so are the “whales”, those addresses controlling between 1,000 BTC and 10,000 BTC.

Graph of % change in holdings of addresses holding less than 1 bitcoin

While the fish have been reaccumulating since July 2021, the cetaceans have started a new wave of buying since the beginning of 2022. The average cost basis of their recent positions is close to $37,000.

Chart of % change in holdings of addresses holding between 1,000 and 10,000 bitcoins

It’s impossible to say whether we’ve hit the bottom of the correction, although the behaviour of participants is the opposite of what it was two months ago.

Current price levels are attracting many entities as February begins with strong spot demand.

The chain is increasingly in demand

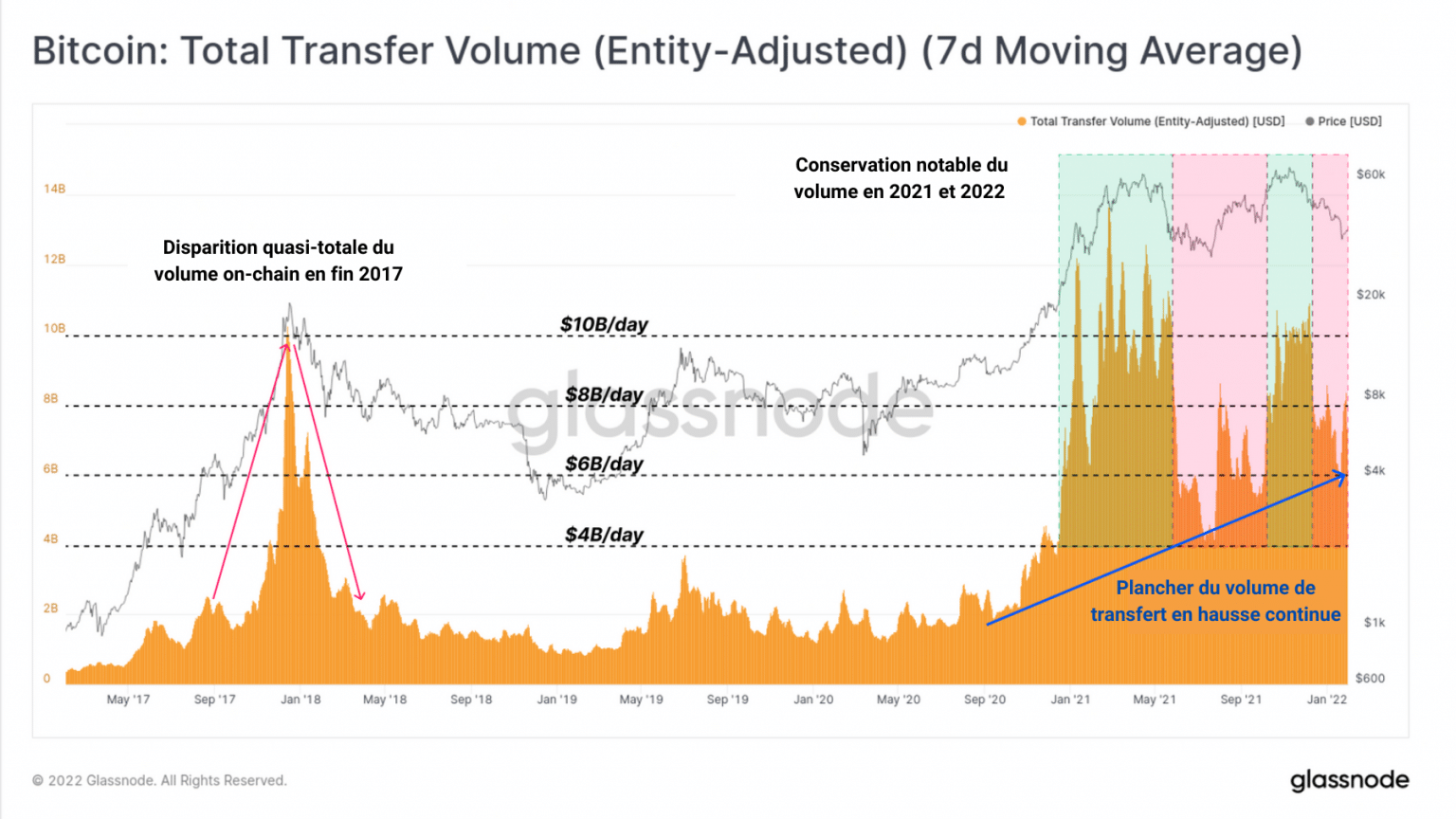

Now let’s go back in time and see how the BTC price has reacted to transfer volume over the past five years.

Typical of a parabolic top like the market has seen since 2011, the 2017 peak marks an all-time transfer peak and then disappears precipitously, a sign of a rapid disengagement of market participants.

They then bequeath the channel to its regular users, generating an average volume of around $2 billion moved daily.

A new ATH in transfer volume does not occur until four years later, in January 2021, when the market welcomes new entrants.

Indeed, emerging nations, corporations, funds and derivatives markets are joining the game alongside more and more individuals and are making unprecedented demands on the blockchain.

Bitcoin transfer volume chart

It is in this context that the volume floor gradually increases while the use of the chain varies according to the trend while maintaining its consistency.

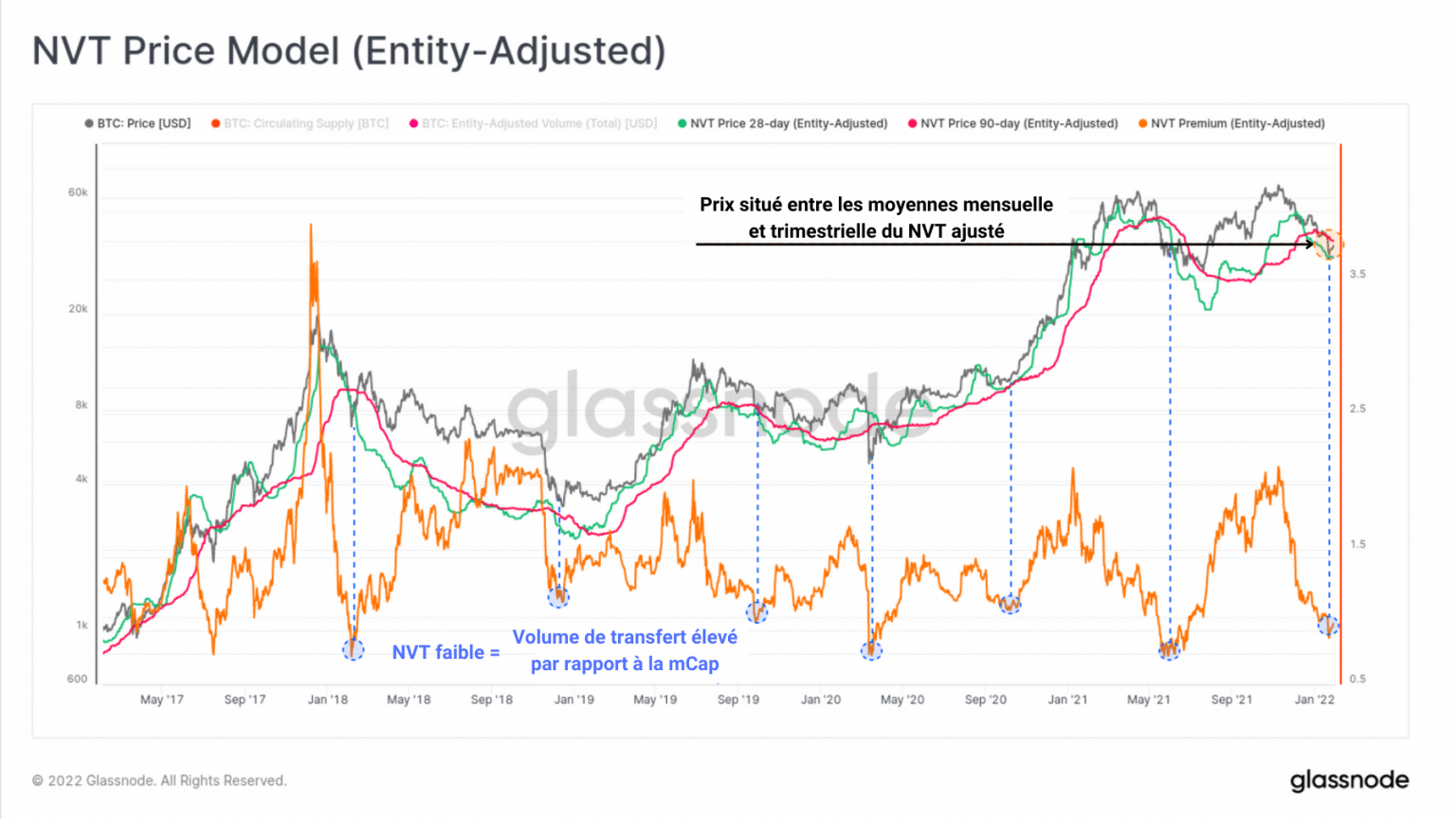

On this occasion, a correction to the interpretation of the NVT signal proposed in a previous article is in order.

The annotation “low network utilisation” would consider a low NVTS as a sign of a chain poor in transfer, a clumsiness that should be rectified immediately.

Remember: the NVT signal is an indicator obtained by dividing the bitcoin network net worth (mCap) by the 90-day average transfer volume. This variant of the NVT ratio therefore follows the same rules.

Graph of bitcoin NVT signal

If the mCap decreases relative to the transfer volume, the deepest dips in the oscillator are reached when the transfer volume increases over the same period.

This indicates significant network usage at a time when the market is correcting, a continuous engagement of participants that does not occur at every correction.

Such a low NVTS has only occurred four times since the end of 2021. Rare are the days when the bitcoin network has been so undervalued for its use in the past.

Bearish bias on derivatives

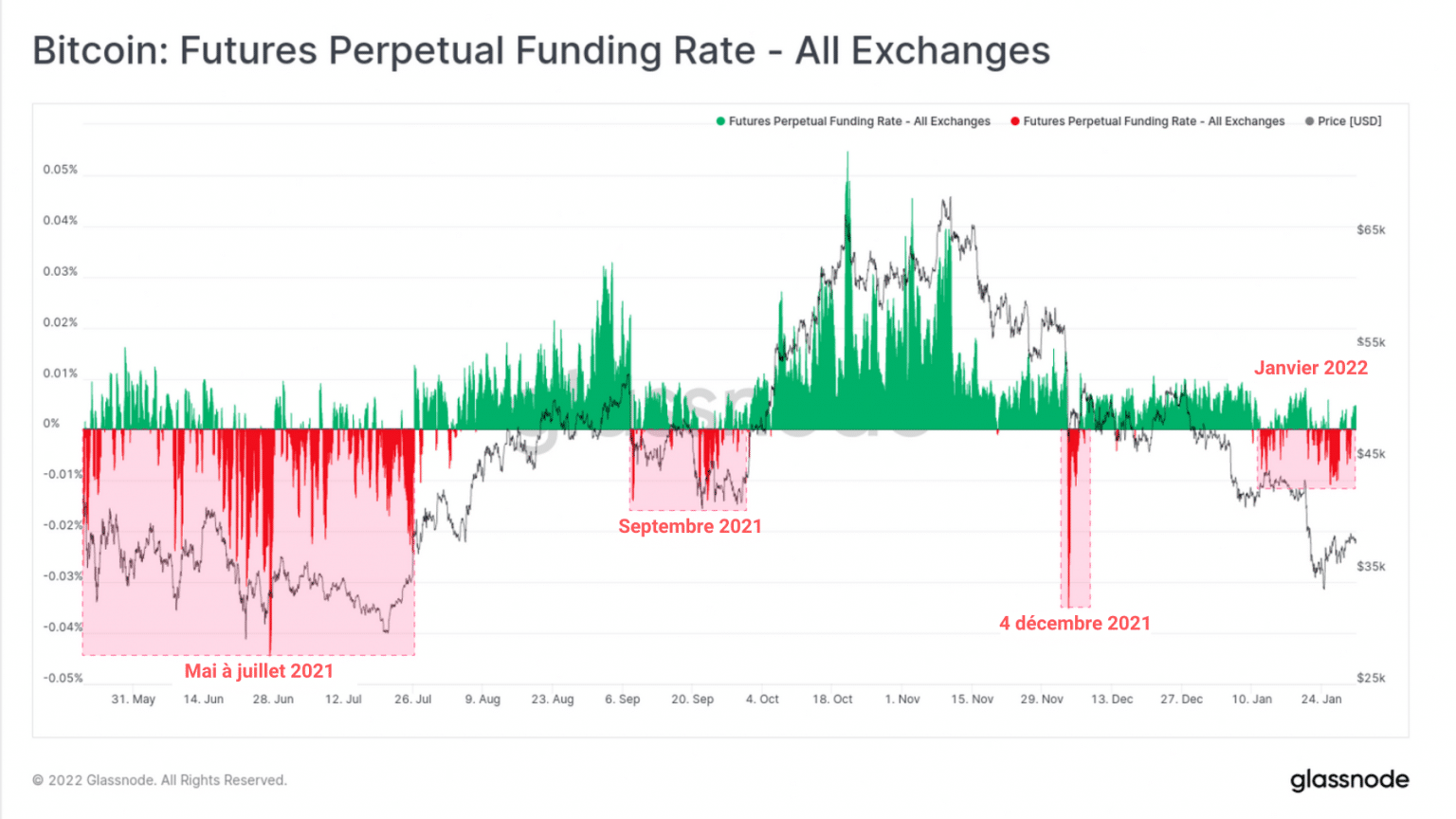

Despite strong spot demand, shorts are appearing in the derivatives markets while open interest remains high.

As shown below, the funding rate for perpetual contracts turned negative repeatedly from 11 January onwards, although the magnitudes remain small.

Some speculators are clearly opening bearish positions and others may follow in an effort to sell BTC in the short zone discussed in CryptOdin’s technical analysis to stall a rebound.

Perpetual contract funding rate chart on bitcoin

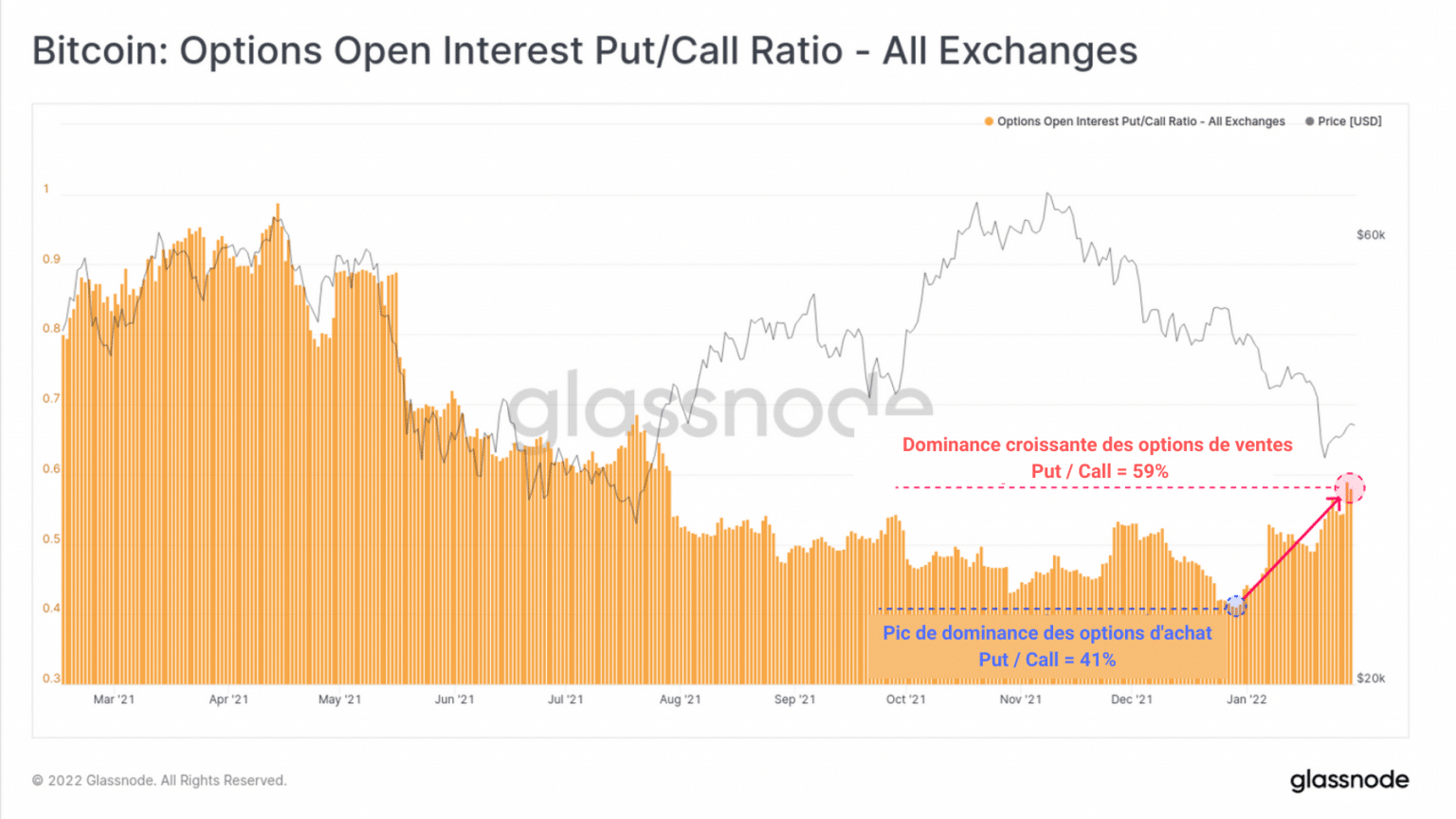

Similar behaviour is emerging in the options markets, with the put/call ratio reaching 59%, the highest in several months.

This indicates that speculators have shifted their preference from calls to buying insurance against declines, even as the market trades at notably low price levels.

Graph of the dominance of the put/call option ratio on bitcoin

With this observable bias movement in the derivatives markets, the dominance of short liquidations could exceed monthly highs in high volatility.

Faced with a bearish bias and high leverage, a reasonable argument could be made for a potential short squeeze if new capital flows into BTC.

Upper momentum divergence

If this eventuality occurs, it could be the trigger for a trend reversal worthy of the July 2021 rally.

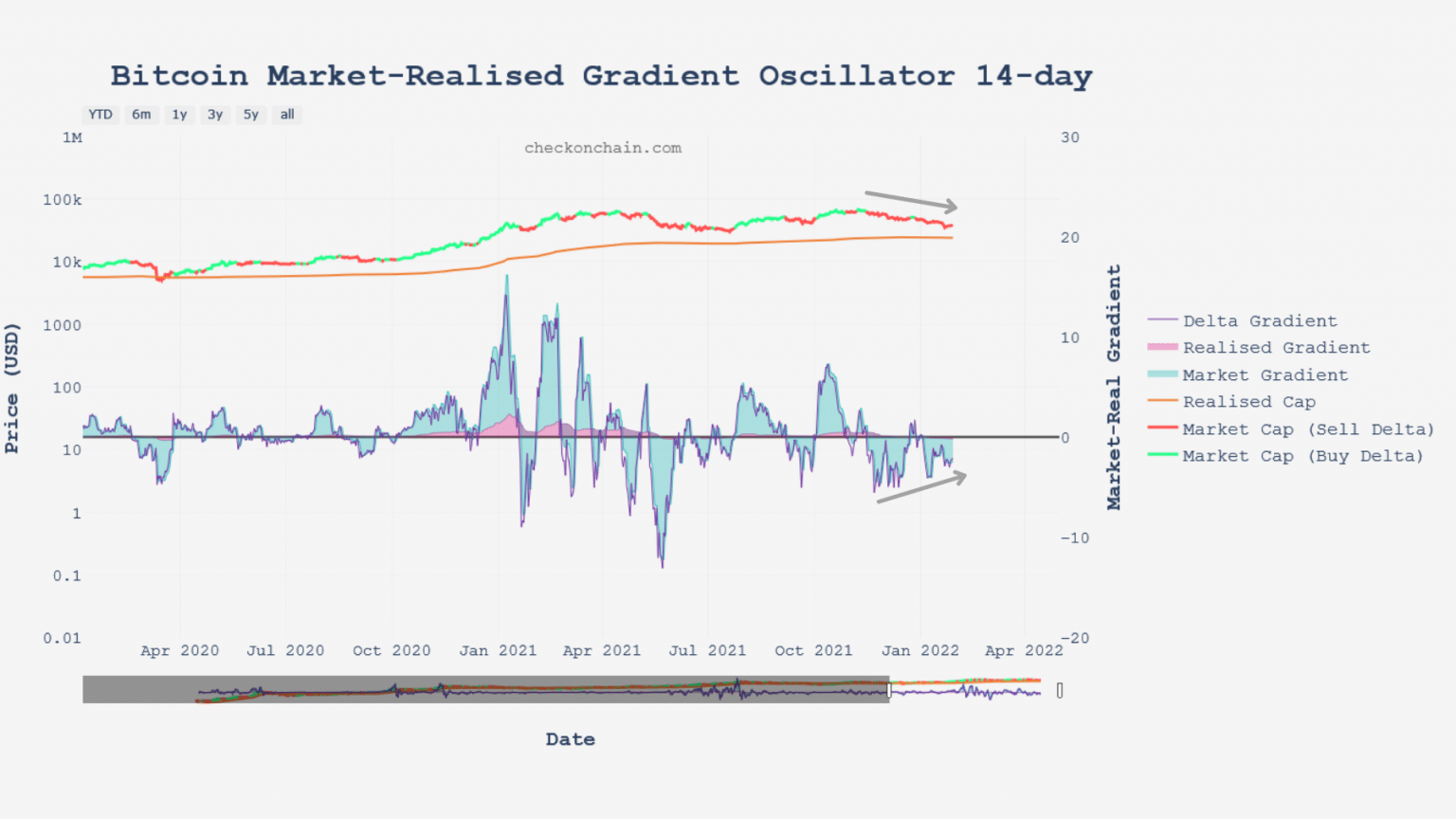

This push would allow the market’s realized gradient (MRG), an indicator that tells us about the market’s momentum, to converge to the upside on three time scales.

As seen below, the MRG-14 indicates an upward divergence between the BTC price and its short-term momentum. Forming a higher low than the previous one, this oscillator signals that the market is struggling to maintain its downward strength.

MRG-14 chart of bitcoin

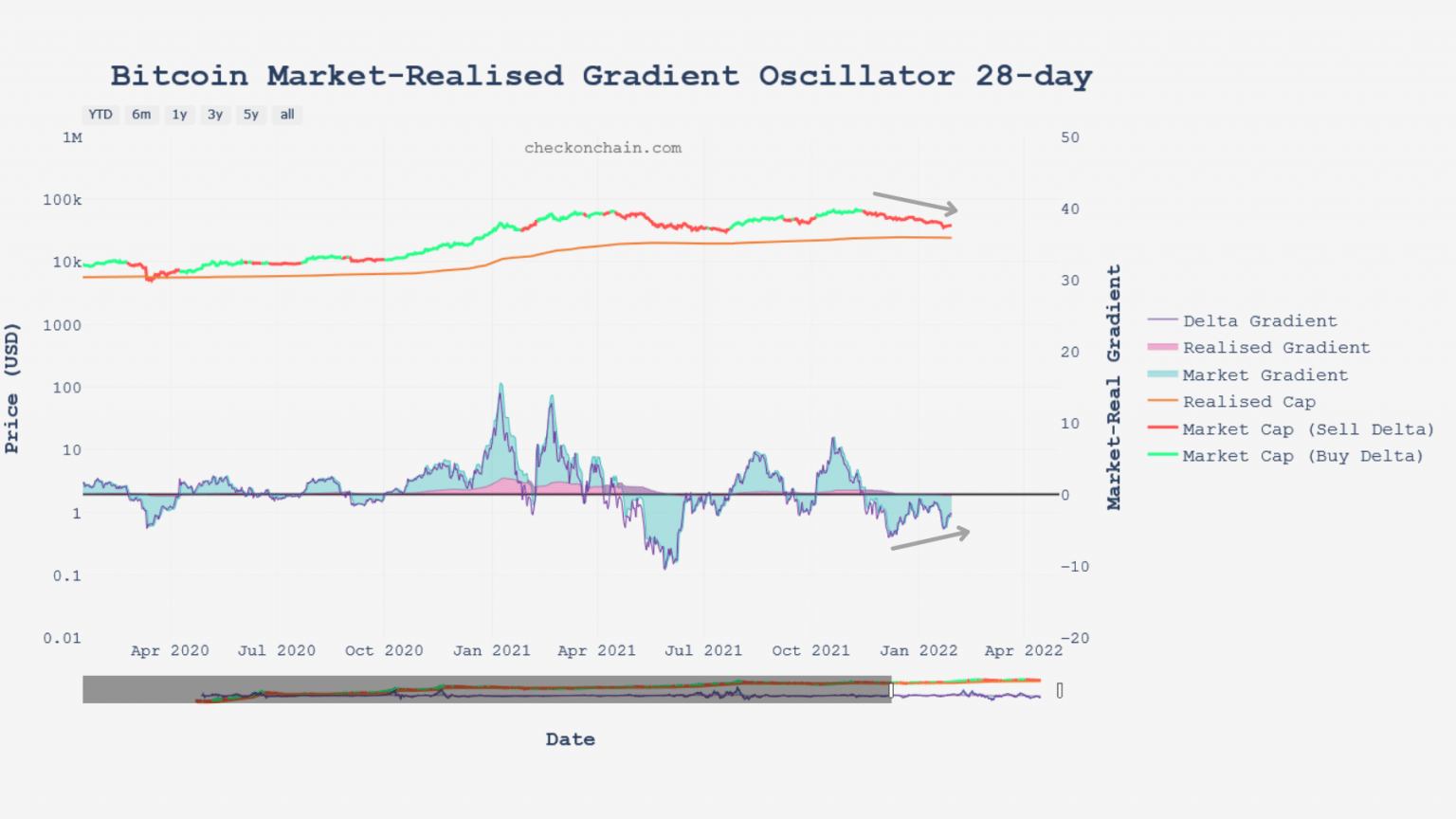

On a medium-term horizon, the observation is the same: bearish impulses are losing power and the realized gradient is approaching the neutrality zone which will have to be crossed as resistance in order to confirm a serious directional change.

MRG-28 chart of bitcoin

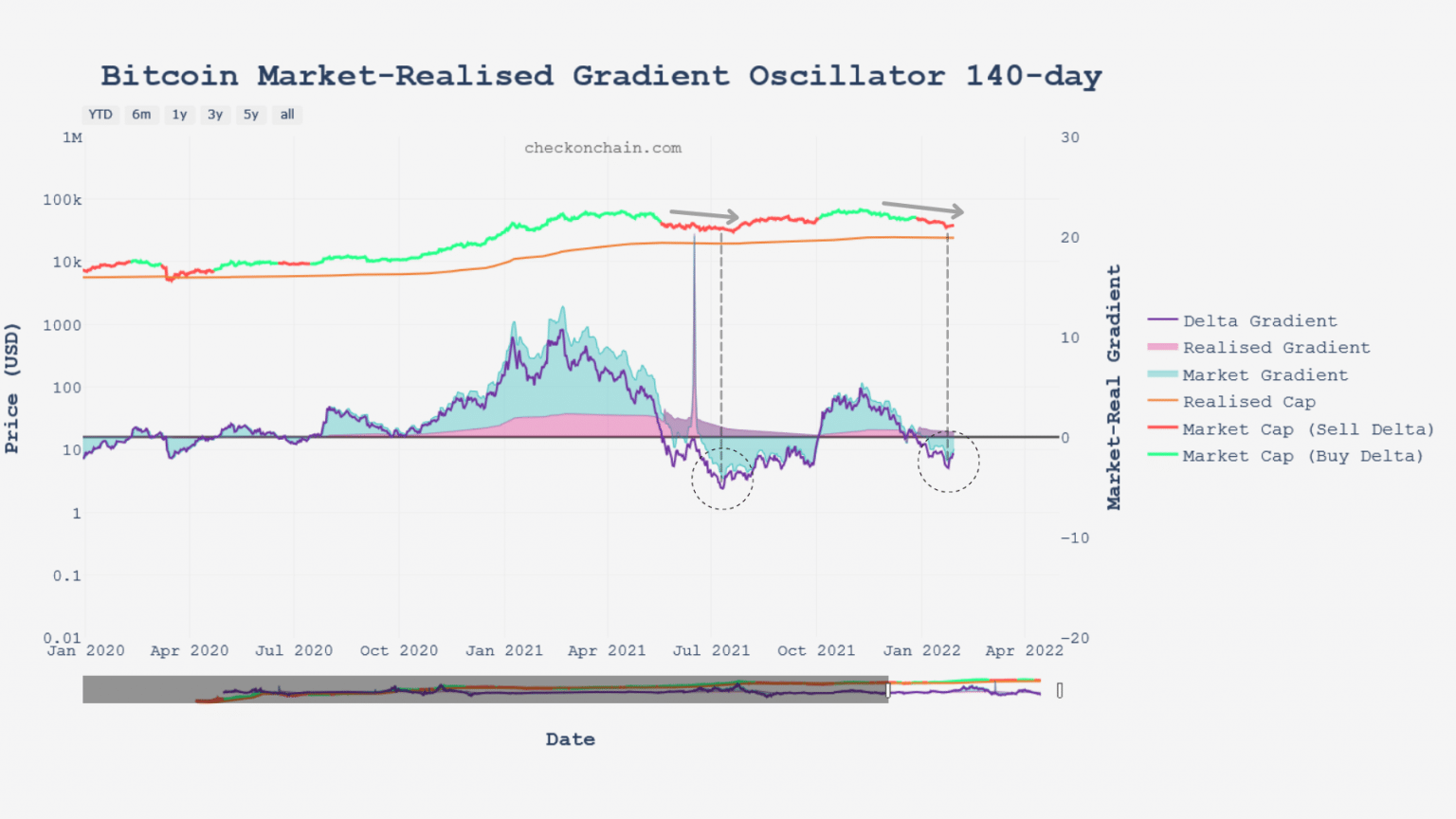

Finally, the confluence of these two oscillators would not be complete without the alignment of the MRG-140, a proxy for long term momentum.

The MRG-140 seems to be on the verge of forming a bottom that could turn into a bullish recovery signal if it were to print positive values again. From this point of view, bitcoin is showing a predisposition to reverse its trend and

MRG-140 chart of bitcoin

Summary of this on-chain analysis

Overall, the bitcoin market is ending January on an optimistic note. While it is too early to seriously declare that a reversal is in the works, many indicators suggest that the market is preparing for it by adopting a structure opposite to that of late 2021.

With hoarding in full swing and a large proportion of investors emptying exchange reserves, the use of the channel suggests that the value of the network is undervalued to a point that only manifests itself on rare occasions.

And as speculators take bearish positions in anticipation of the next decline, the risk of short squeeze and could initiate a reversal of momentum on several time scales.

Gradually, the right conditions are falling into place, but we still have to wait to see more confluence between indicators in other aspects of the chain that we will detail in the next analysis.