Morpho is a decentralised peer-to-peer lending protocol based on protocols like Aave and Compound. The interest rates for both providers and borrowers are more advantageous thanks to optimised liquidity allocation mechanisms. Focus on a new innovative lending protocol

What is Morpho

Morpho is a protocol for borrowing and lending cryptocurrencies. It is based on the peer-to-peer (P2P) exchange model developed on underlying and existing lending protocols such as Aave or Compound. This protocol, operating on the Ethereum blockchain, has been developed since 2021 by Morpho Labs, a French company.

In concrete terms, Morpho functions as a portal to decentralised lending, and the decentralised application (DApp) connects borrowers and liquidity providers.

It is therefore possible to make a loan or provide funds and receive interest in return. The question is: what is the point of using Morpho’s app instead of using Aave or Compound’s apps directly?

Borrowing cryptocurrencies is a common financial transaction in the decentralised finance (DeFi) sector, the successes of Aave or Compound prove this with total locked-in values (TVL) accumulating $8 billion and $4 billion respectively in June 2022 (both rise to the top 10 highest TVLs in DeFi). Moreover, the growth of this segment continues to be very promising.

However, the Morpho team has observed, by analysing historical supply data against borrowing rates of the main DeFi protocols, that borrowing rates are very high compared to supply rates, which are very low.

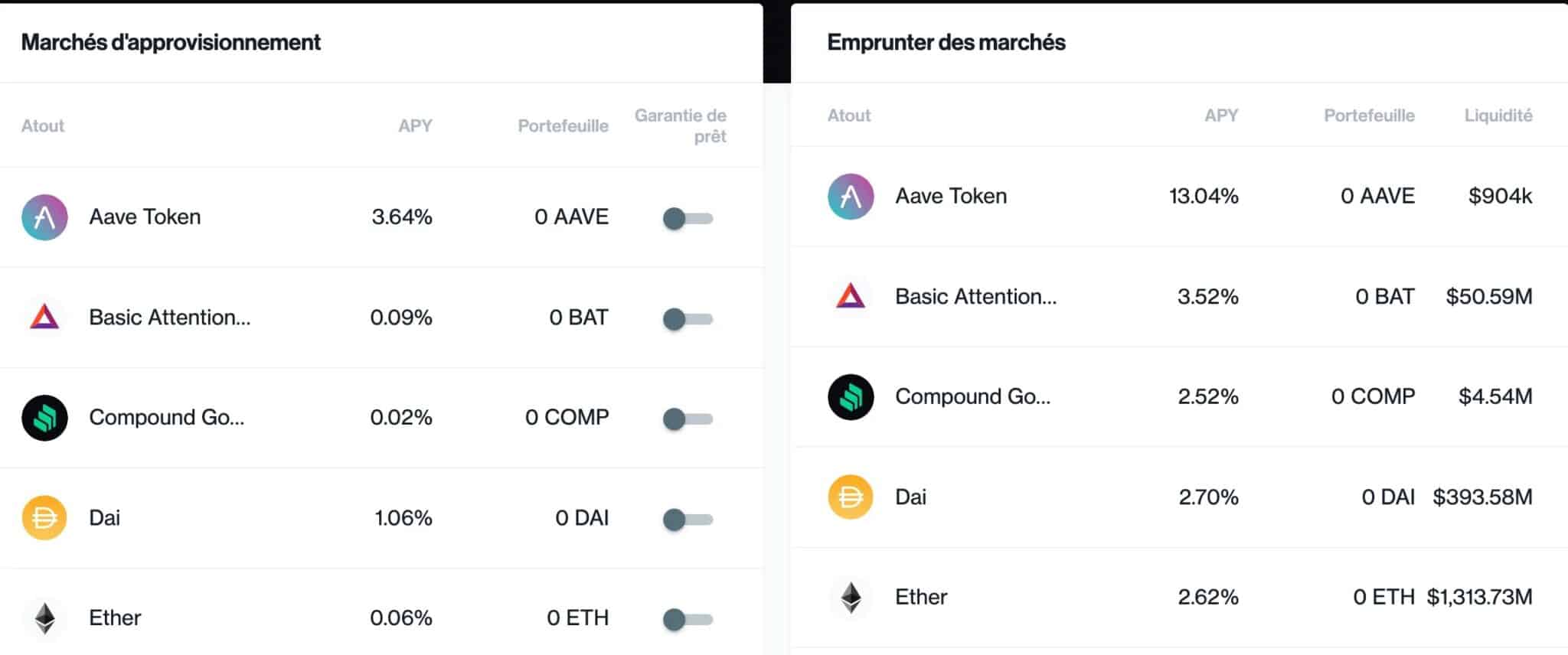

Figure 1: Overview of the lending market on Compound

Indeed, the spread between bid and offer rates for this type of protocol can be quite high. For example, if we look at the Compound dApp as illustrated above, we can see a significant spread on Ether: 0.06% APY for the bid rate versus 2.62% for the offer rate.

Why such a large spread? With DeFi, which is supposed to cut out the middleman, the liquidity provider should earn the same as the borrower pays for the loan, yet this is far from being the case on the lending protocols.

The answer lies in the model used by these protocols. Compound, for example, is based on the Peer-to-Pool model in which providers deposit their liquidity in a pool and receive tokens in exchange. A borrower, on the other hand, provides collateral to the protocol to access the liquidity in that same pool and thus borrow cryptocurrencies.

When a borrower repays his loan, he pays interest that goes into that same pool and is shared by all the providers in that pool, in proportion to the amount provided. Suppliers commit far more capital to the pool than is necessary in this model, which is why the APY of the supply is much lower than that of the loan.

This spread between the two APYs is intentional, since by using only part of the available capital in the pool, it allows suppliers and borrowers to withdraw or borrow funds at any time. This is what preserves the liquidity of the positions.

However, this model is not efficient, and this is where Morpho aims to change things, in order to match the interest rates for both parties, by creating a peer-to-peer order book recording each position.

In this way, the Morpho protocol leverages protocols such as Compound and Aave to create an efficient and liquid peer-to-peer market for bidding and borrowing positions.

Using the previous example of Ether on Compound (0.06% for the bid rate versus 2.62% for the offer rate), the Morpho protocol would achieve a rate of around 1.28% for both parties in the best case scenario.

At best, the protocol thus allows providers to have positions that match the same rate the borrower is paying, and at worst, the rates already existing on the underlying protocols (such as Aave or Compound).

Figure 2: Overview of how interest rates work on the Morpho protocol

Morpho is therefore focused on optimisation. It is about allowing borrowers and providers to benefit from a better interest rate: lower for borrowers so they pay less interest on a loan, while providers benefit from a higher rate and are therefore better rewarded. Both parties gain while maintaining the same collateral and liquidity.

This is illustrated in Figure 2, where the middle curve shows the rates provided by the Morpho protocol. The Morpho protocol thus aims to help unlock the full potential of DeFi in this way.

How Morpho works

In order to succeed in fulfilling the objective we have mentioned, the Morpho protocol works in a particular way. Indeed, liquidity on Morpho is dynamically assigned to borrowers, instead of pooling liquidity.

Since liquidity is dynamically assigned, liquidity providers compete with each other: this is the fundamental difference with more traditional lending protocols. However, the user experience remains the same as with other lending protocols such as Compound, as everything is done in the backend.

In this way, the interest paid by the borrower goes directly to the provider whose liquidity has been assigned to that borrower. In this way it is possible to have a corresponding rate between borrower and provider, or at least closer.

Morpho, as mentioned, is a protocol that builds on existing lending protocols such as Aave and Compound. Thus, if there is not enough liquidity on Morpho, the protocol will use liquidity from the pools of these other protocols.

How is liquidity assigned?

The Morpho protocol maintains an on-chain priority queue, sorting users according to the amount of cryptocurrency they wish to provide or borrow. The advantage of such a sorting method is the minimisation of gas costs and resistance to Sybil attacks.

In the case of a new provider offering liquidity on the protocol, it is assigned to the largest borrower first, then the second, then the third, until the liquidity provided is fully assigned or there are no more borrowers requiring funds.

Symmetrically, when a new borrower requests funds for its loan, this request is matched with the largest provider first, then the second, until its request is satisfied or there are no more providers.

Liquidity providers and borrowers are thus directly linked in a peer-to-peer model. The Morpho protocol can freely choose the lending and borrowing rates, however these rates must be kept within the range induced by the underlying protocols to be effective.

As we have seen, ideally these two rates are identical, but this is not always the case. These rates are driven by parameters from protocol governance, but even a small difference in rates between the underlying protocols and Morpho is beneficial to borrowers and providers as the former pay less interest and the latter receive more interest.

In the future, fees will be charged by the Morpho protocol to cover the protocol’s expenses, to feed its reserve or to cover a sudden increase in demand for liquidity. However, this is not yet the case at the time of writing.

Finally, these fees will only apply to corresponding peer-to-peer volumes, for example when a borrower’s demand is met directly by one or more providers.

How are rewards distributed?

Morpho automatically transfers the rewards distributed by the underlying protocols to the providers (such as COMP tokens on Compound). In concrete terms, providers can use the Morpho protocol as if they were directly using the underlying protocol.

In addition, Morpho also distributes rewards to its users. Every 2 weeks, Morpho’s decentralised autonomous organisation (DAO) will vote on the amount of MORPHO tokens and market gauges to reward its users based on their use of the protocol during the period in question.

Decentralised governance is not yet implemented in the application at the time of writing, however. Similarly, you will have noticed that there will be a MORPHO token, but we have little information about it at the moment.

How to use the Morpho protocol

The Morpho application is very intuitive. After connecting your digital wallet to it, you will be presented with the following interface:

Figure 3: Overview of the Morpho application interface (with Compound)

Here the underlying protocol used is Compound, but it can be another one such as Aave. On the left are the interest rates that providers receive via Compound, while on the right are the interest rates that borrowers have to pay via Compound.

The interesting part is in the middle of the interface. The column entitled “P2P APY” shows the interest rates offered by the Morpho protocol, and it can be seen that these are more attractive on the assets in question than on the Compound protocol.

Taking the example of UDST, Compound offers a 2.17% rate for suppliers and a 3.71% rate for borrowers. The Morpho protocol, on the other hand, thanks to the mechanisms explained above, offers a rate of 2.78% for both parties.

Thus, the provider gains by receiving more interest than with the initial rate of 2.17% while the borrower gains by paying less interest on his loan than with the initial rate of 3.71%.

Our opinion on the Morpho protocol

Morpho offers a highly efficient peer-to-peer lending protocol with mechanisms that assign liquidity directly between providers and borrowers.

Moving away from the classic Peer-to-Pool model of DeFi lending protocols, this new P2P model proposed by Morpho allows users to benefit from better interest rates.

Thus, Morpho is an improvement of the Compound and Aave protocols, so it is in the user’s best interest to use Morpho-Compound if they already use Compound and Morpho-Aave if they already use Aave. It should be noted that Morpho-Aave is not yet available at the time of writing, but will arrive shortly.

Morpho thus manages to optimise this market and offers DeFi an additional argument to attract new potential users. The market for decentralised lending is already quite prosperous and it will be interesting to see whether Morpho can capture a share of this market with its innovations.

Finally, new features such as the integration of other lending protocols, governance or the MORPHO token are highly anticipated and will probably help the protocol to expand its adoption.

Sources – Figure 1: Compound; Figures 2 and 3: Morpho.