The dramatic and painful collapse of the Terra ecosystem has led to a de-anchoring of UST and selling pressure of over 80,000 BTC on the market. A look back at the events of the past week and the hyperinflation of the LUNA token through the lens of on-chain analysis.

The Terra ecosystem six feet under

The collapse in a matter of days of the Terra ecosystem, home to the 3rd most capitalized stablecoin (UST) and the LUNA token, has been the subject of much discussion in recent weeks.

Now recognised as one of the most spectacular implosions in cryptocurrency history, the de-anchoring of the UST has caused a hyperinflation of the LUNA token that would make the Weimar Republic pale in comparison.

Cryptoast today takes a look at the recent events surrounding the hyperinflation of the LUNA token and the de-anchoring of its stablecoin UST through on-chain analysis.

An annualized inflation rate of 99,263,840%

Over the past few years, the stablecoin market has grown dramatically, consolidating nearly $135 billion in value between the USDT, USDC, BUSD, DAI and UST as of May 8.

The fundamental use of stablecoins in the cryptocurrency ecosystem makes them a major pillar whose dynamics are influenced by, among other things, the evolution of the Bitcoin (BTC) market and its short-term volatility.

Stablecoins, which come in several types, can generally be listed as follows:

- Collateralised (USDT, USDC, BUSD);

- Over-collateralised (DAI);

- Algorithmic (UST).

In the case of UST and LUNA, their design allowed users to convert 1 UST into 1 dollar of LUNA (and vice versa), regardless of the price of the two assets. Through this arbitrage mechanism, a demand for UST caused a contraction in the supply of LUNA, leading to an appreciation in its price if there was sufficient demand.

Despite this strategy, the current uncertainty and volatility in prices caused participants in the Terra ecosystem to panic. On 8 May, when the BTC market resumed its fall, a large number of investors burned USTs to recover LUNA, in order to liquidate their position as soon as possible.

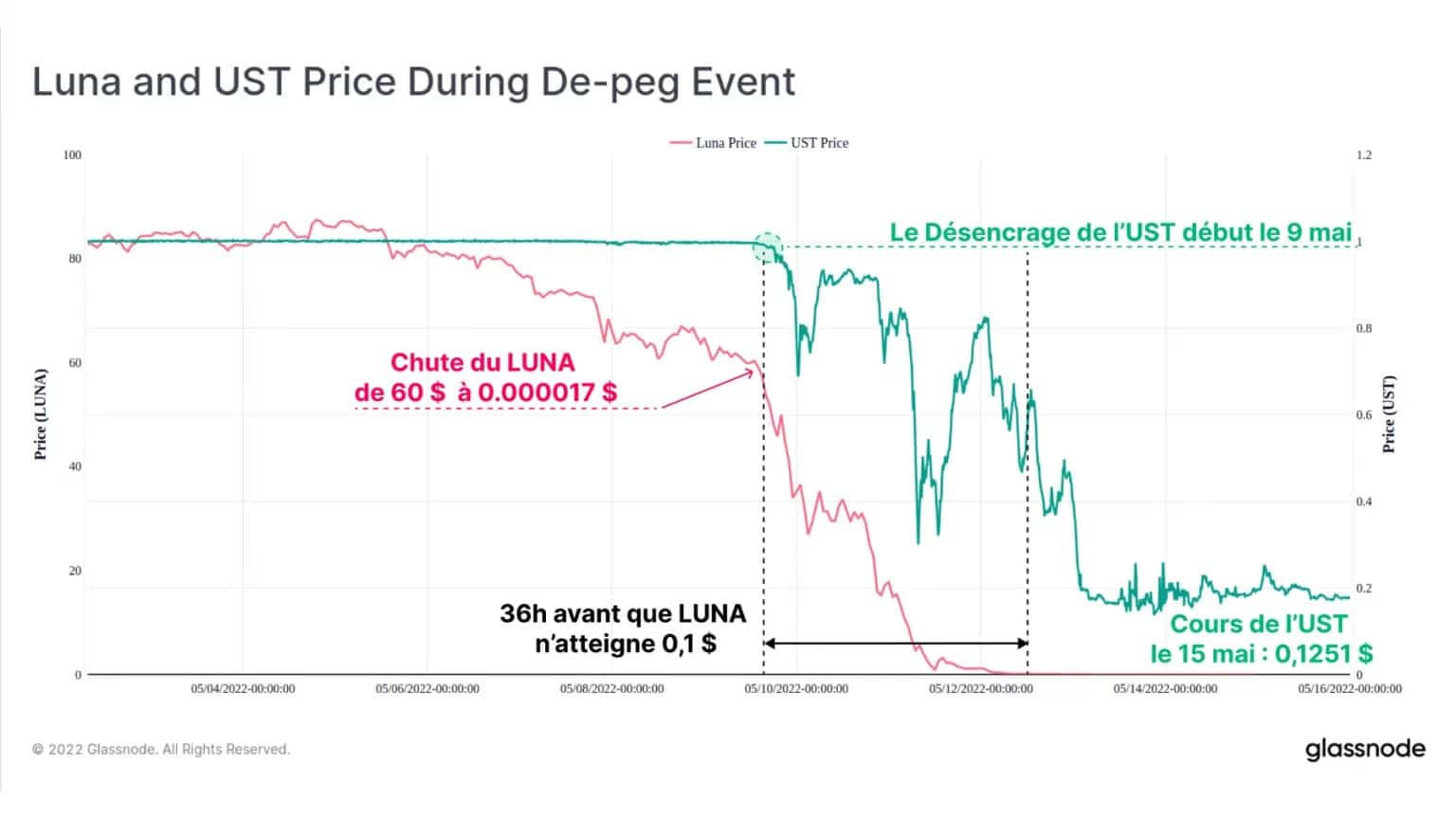

According to data from the latest Glassnode report, the UST anchor began its deviation on May 9, when LUNA was valued at around $60 (~49.5% from its ATH). Over the next 36 hours, the price of LUNA fell below $0.1 and its UST parity against the dollar fluctuated between $0.30 and $0.82.

Figure 1: UST and LUNA rates

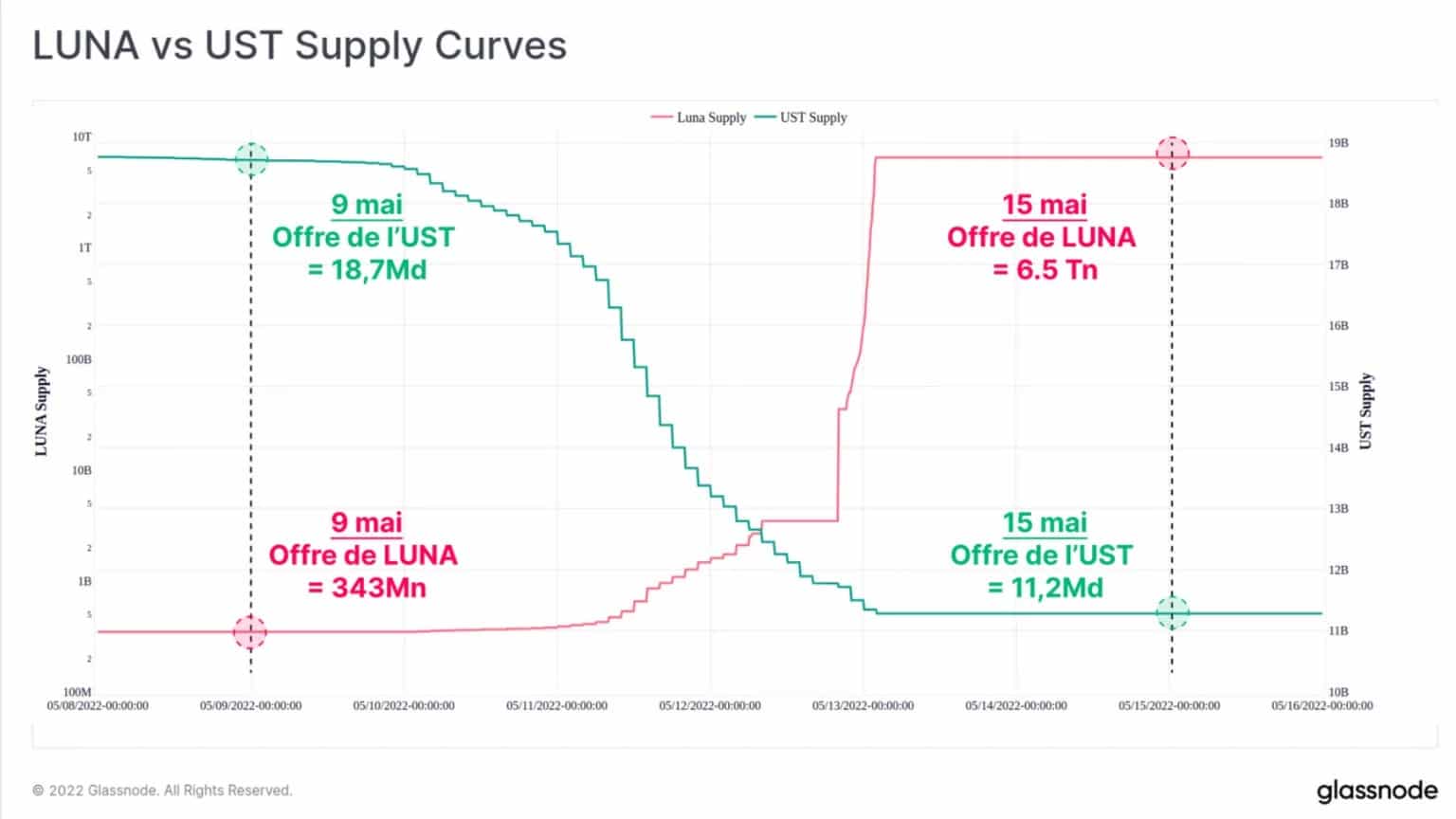

The protocol’s arbitrage mechanism then went into overdrive, with users taking fright favouring the exchange of one UST for one dollar of LUNA, increasing its supply while diluting its price.

The extent of LUNA’s supply inflation can be seen in the chart below, where UST supply (green) is in linear scale, while LUNA supply (red) is in logarithmic scale.

In one week, LUNA’s supply has grown from 343 million to over 6.53 billion, an annualized inflation rate of 99,263,840%, unheard of in the cryptocurrency ecosystem.

Figure 2: UST and LUNA supply in circulation

To date, the LUNA is worth $0.0001 (-99.9998% compared to the ATH) while the UST is stabilising around $0.06, forever excluded from a stable parity with the dollar.

As the UST parity fell, the Luna Foundation Guard (LFG) decided to deploy its recently acquired bitcoin reserves in an effort to stabilise its parity against the dollar by attempting successive capital injections.

The portfolio’s total reserves (80,394 BTC), valued at around USD 3.275 billion, were completely emptied in less than 24 hours, between 9 and 10 May.

The remaining BTC in the LFG were liquidated in three stages, as shown below. The first sale deployed a value of approximately $750 million (22,189 BTC) at 3:30pm on 9 May, when UST parity was around $0.98.

The second salvo of 30,000 BTC ($916 million) was deployed 15 hours later, and the final sale of 28,205 BTC ($873 million) left the wallet bereft at 01:30 on May 10.

Figure 3: Luna Foundation Guard’s BTC holdings; Inflows on exchanges

A series of inflows on the exchanges (in blue) can be observed between 18:30 on 9 May and 01:10 on 10 May and testify to these deposit phases. According to Glassnode’s estimates, the initial destination of these coins was as follows:

- 52,189 BTC sent to Gemini via OTC desks (which were quickly deployed elsewhere, including on Binance and Coinbase);

- 28 205 BTC sent to Binance via direct transfer.

Spillover effect on major stablecoins

A few hours later, on May 11, Tether (USDT), the largest stablecoin in terms of market capitalization, saw its anchor deviate as investors shifted the side effects of the Terra ecosystem collapse to other non-algorithmic stablecoins.

Many consider the USDT with its $83 billion market cap to be a systemic pillar for the market in its current form, being the dominant trading pair on many exchanges.

Between May 11 and mid-day on May 12, the USDT began to dissociate from its $1 benchmark, hitting a momentary low of $0.9565 before recovering within 36 hours to trade today at a slight discount of $0.998.

Figure 4: BUSD, DAI, USDC and USDT prices

Meanwhile, the other major stablecoins (USDC, BUSD and DAI) traded at a 1-2% premium for a short time as investors turned to these assets seen as less exposed to contagion risk.

Tether announced on 12 May, at the height of the stress test, that USDT exchanges remained operational and backed by the dollar price despite the deviation, which was filled by a capital injection from the Tether Foundation.

Summary of this on-chain analysis

The events of the past week will remain etched in the memories of many participants. The double collapse of UST and USDT, the destruction of some $40 billion in value for LUNA/UST, and the selling pressure of 80,000 BTC by LFG created a storm that did not fail to attract the attention of regulators.

Nevertheless, the Terra ecosystem case provides an exemplary case study in hyperinflation and offered everyone a glimpse of the value destruction induced by the limitless expansion of a money supply.

Finally, as stablecoins become increasingly integrated as a core market infrastructure, the shockwaves of potential failures, particularly for important stablecoins such as USDT, USDC or DAI, will have potentially widespread and documentable impacts across the cryptocurrency market.