Bitcoin is going through a critical period: transaction fees are falling and blocks are not all full. While network security depends on these economic incentives, the question becomes urgent: is a model based solely on fees viable in the long term?

Could the Bitcoin blockchain shut down once all BTC has been mined?

For about a year now, the Bitcoin and Ethereum blockchains have seen a significant drop in transaction fees collected. This situation can be explained in part by a new phase of adoption led by institutions, which use third-party custodians to store and exchange their assets, thereby reducing on-chain activity. On Bitcoin, the rise of second-layer solutions such as the Lightning Network and Liquid is accentuating this dynamic. These tools allow users to manage their assets more easily, more confidentially, and above all, at a lower cost.

This decline in activity reignites an old debate: the future of Bitcoin in a world where mining rewards remain low. What will happen when fees become the only source of income for miners?

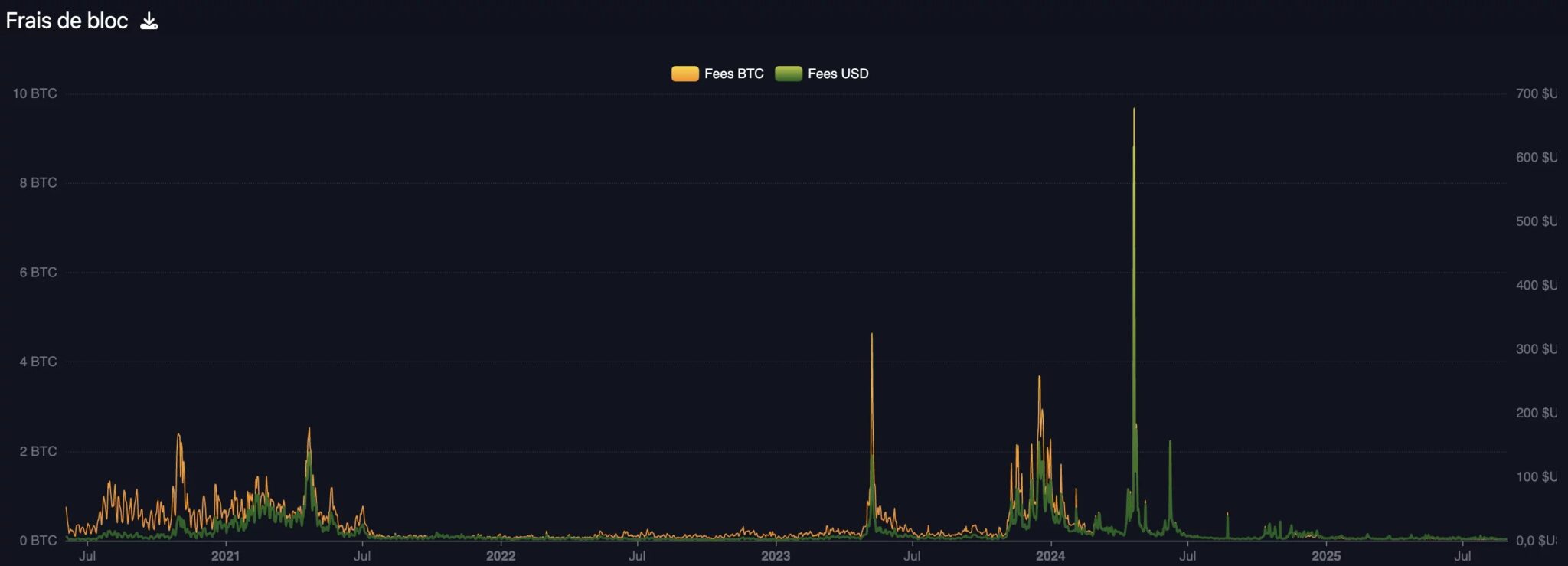

As the chart below shows, transaction fees collected per Bitcoin block are now at their lowest level, around $2,000, a threshold similar to that observed during the 2022 bear market.

It is therefore difficult to imagine that Bitcoin and its miners can survive in the long term with such low fees. Once the block reward, which is halved every four years, becomes negligible, miners will have to rely on higher fees to remain profitable.

This criticism, while relevant, overlooks a key point in Satoshi Nakamoto’s design: mining is designed to adapt to the economic state of the network.

The graph below shows that, despite historically low fees, the total reward (fees + subsidy) remains high, excluding peaks of euphoria such as those observed during the 2021 bull run or during periods of high activity related to Ordinals and Runes.

What will happen if fees remain low for a long time?

It is difficult, if not impossible, to predict how miners will react to a continued decline in rewards if on-chain activity does not pick up again.

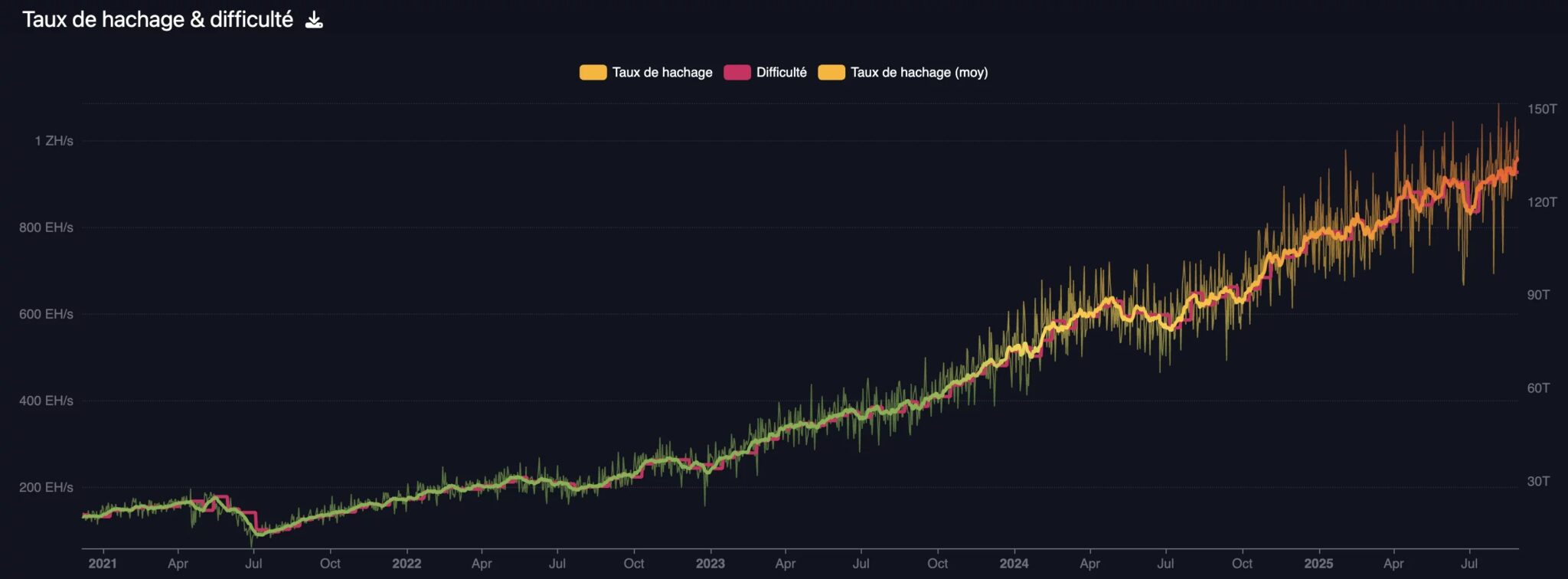

However, the mining market has never been so buoyant. The hashrate, i.e., the computing power securing the network, has just broken a historic record, proving that the activity remains highly profitable despite the decline in fees.

With an average of 962 EH/s, never before has so much power been dedicated to the security of the Bitcoin blockchain, despite the low fees collected.

This rate is 10 times higher than after the “China Ban” of 2021, when more than 50% of miners (then located in China) had to cease their activities overnight.

Thus, a sustained drop in fees could well cause the hashrate to fall by bankrupting the least competitive miners, but that would not necessarily spell the end of Bitcoin. The network is designed to automatically adjust to these variations in hashrate.

Finally, even if industrial mining were to become unprofitable, it is still conceivable that the activity could return to individual users. They could choose to secure the network out of conviction, not for profit, with the aim of preserving a monetary system they consider essential.