In just a few months, the US has rolled out the red carpet for stablecoins. The GENIUS Act, widely supported, aims to regulate them and should come into force very soon. But are these really just good intentions? Or could it be that, ultimately, this is all a ploy to save the debt and favor the biggest banks?

Stablecoins are booming. But why?

Since the beginning of 2021, stablecoins have experienced significant growth and have gradually become a staple of the crypto market. These unique cryptocurrencies are backed by an asset, very often a currency such as the dollar or the euro.

Almost always the dollar, in fact: at the time of writing, stablecoins have a market capitalization of $264 billion. Of this amount, $256.5 billion are stablecoins backed by the dollar, with giants Tether and Circle leading the way.

The former, the historic leader in the sector, has a market capitalization of $158 billion with its USDT. Circle, the eternal runner-up, has a market capitalization of $62 billion with the USDC.

Recently, stablecoins have been praised in the United States, both by banks and businesses. The reason for this is the regulatory relaxation that has been emerging since Donald Trump became president, notably through the GENIUS Act recently passed by the Senate. Even Scott Bessent, the US Secretary of the Treasury, seems to be enthusiastic about the idea of stablecoins coming into their own:

Recent reporting projects that stablecoins could grow into a $3.7 trillion market by the end of the decade. That scenario becomes more likely with passage of the GENIUS Act.

A thriving stablecoin ecosystem will drive demand from the private sector for US Treasuries, which back…

— Treasury Secretary Scott Bessent (@SecScottBessent) June 17, 2025

Recent reports predict that stablecoins could reach a market value of $3.7 trillion by the end of the decade. This scenario is becoming more likely with the adoption of the GENIUS Act. But above all, Scott Bessent emphasizes one thing: “A thriving stablecoin ecosystem will stimulate private sector demand for the US Treasury bills that back them. This new demand could reduce borrowing costs for states and help control national debt.” “

This is the beginning of an answer to the question posed by Arthur Hayes, co-founder of BitMEX, in his latest blog post:

Why is Scott Bessent so bullish on stablecoins? Why did the Genius Act receive bipartisan support?

Do US politicians really care about financial freedom, or is there something else behind it? Perhaps they care about it in the abstract, but noble ideals do not motivate action.US debt in the background

To back up his argument, Arthur Hayes provided a few reminders. Faced with uncontrolled spending, the US finds itself in the following situation:

- Public spending is skyrocketing (particularly on security, with US involvement in Ukraine and the Middle East);

- Taxes are not keeping pace;

- The only recourse is debt.

This is not unique to the United States, as the following chart shows. However, their 30-year bond yields are among the highest, reflecting a loss of confidence among borrowers in the government’s ability to repay its debt.

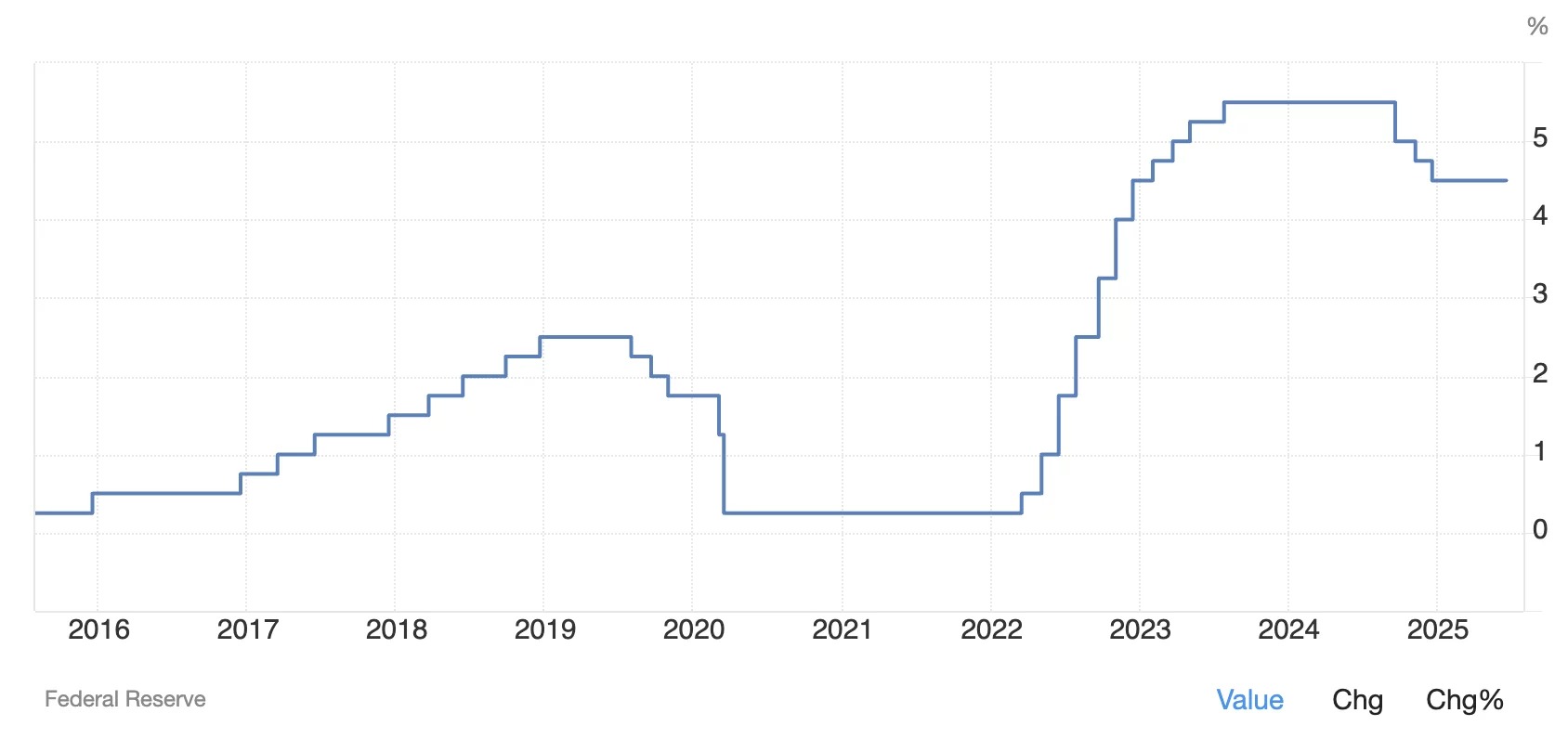

What’s more, since 2022, quantitative easing has come to an end: the Fed can no longer buy Treasury bonds on a massive scale as it did after 2008 while keeping interest rates very low.

Finally, according to Arthur Hayes, the liquidity well of the Reverse Repo Program (RRP), which aims to allow financial institutions to temporarily deposit their money with the Fed in exchange for Treasury bills or MBS (Mortgage-Backed Securities), with a small return, is soon to dry up.

This mechanism, which took over during a period of undisguised quantitative easing, helped to preserve the stability of the US monetary system.

With this “secret weapon” no longer available, what solution is there to save the markets?

Stablecoins: trillions for Treasury bills

This is where stablecoins come in. “The ‘too big to fail’ banks have significant reserves (deposits, Fed reserves). They could inject up to $6.8 trillion into T-bills if they are allowed to issue stablecoins,” says Arthur Hayes.

While banks were encouraged to accumulate large amounts of long-term Treasury bills from 2020 to 2022, the sudden rise in interest rates has led to the bankruptcy of some of them. Those still standing are therefore naturally less inclined to expose themselves to US debt.

What they are now looking for are more liquid, less risky and yield-generating assets. Short-term T-bills meet these criteria. Above all, stablecoins offer a perfectly suited channel for holding these assets while meeting operational profitability requirements.

JPMorgan, the largest bank in the United States, has clearly understood this: it has just officially launched JPMD, a deposit token that will be offered on the Base layer 2 and, for the time being, reserved for institutional investors.

As Arthur Hayes points out, the relaxation of the Supplemental Leverage Ratio (SLR), which is due to come into effect within six months, will reduce the amount of capital that banks have to tie up against their T-bill holdings. This measure is expected to free up up to $5.5 trillion in liquidity on bank balance sheets.

This liquidity will enable large banks to buy short-term Treasury bills on a massive scale while issuing more and more stablecoins, which should eventually cannibalize traditional deposits.

This is a win-win situation: banks buy back US debt while reducing their massive compliance costs, for example by automating on-chain transaction analysis with AI. This is how a stablecoin issued by a bank becomes an indirect buyer of public debt.

A well-oiled machine designed to maintain the banks’ hegemony

What’s more, some of the measures in the GENIUS Act are not insignificant. They guarantee the oligopoly of the largest US banks, which work hand in hand with the government, notably by prohibiting Big Tech from issuing their own stablecoins, which will be obliged to work with… a bank.

Finally, as Arthur Hayes points out, FinTechs such as Circle and small banks do not benefit from a government guarantee on their commitments, unlike large banks. “If my mother were to ever use a stablecoin, it would be one issued by a TBTF bank. Boomers like her will never use a FinTech or small bank for this purpose because they don’t trust them due to the lack of government guarantees,” he says.p>

In short, stablecoins would allow banks to:

p>

- Not lose deposits that could go to competitors (FinTech, etc.);

- Reduce compliance costs;

- Not pay interest;

- Earn returns via short-term T-bills;

- Boost their share price.

“The Trojan horse of stablecoins is already inside the fortress, and when it opens, it will not be armed with libertarian dreams—it will be loaded with cash to buy Treasury bills to keep stocks inflated, deficits financed, and baby boomers asleep,” he concludes.