The attractiveness of a sector can be measured in various ways, one of which is by the amount of funds invested by venture capital firms.

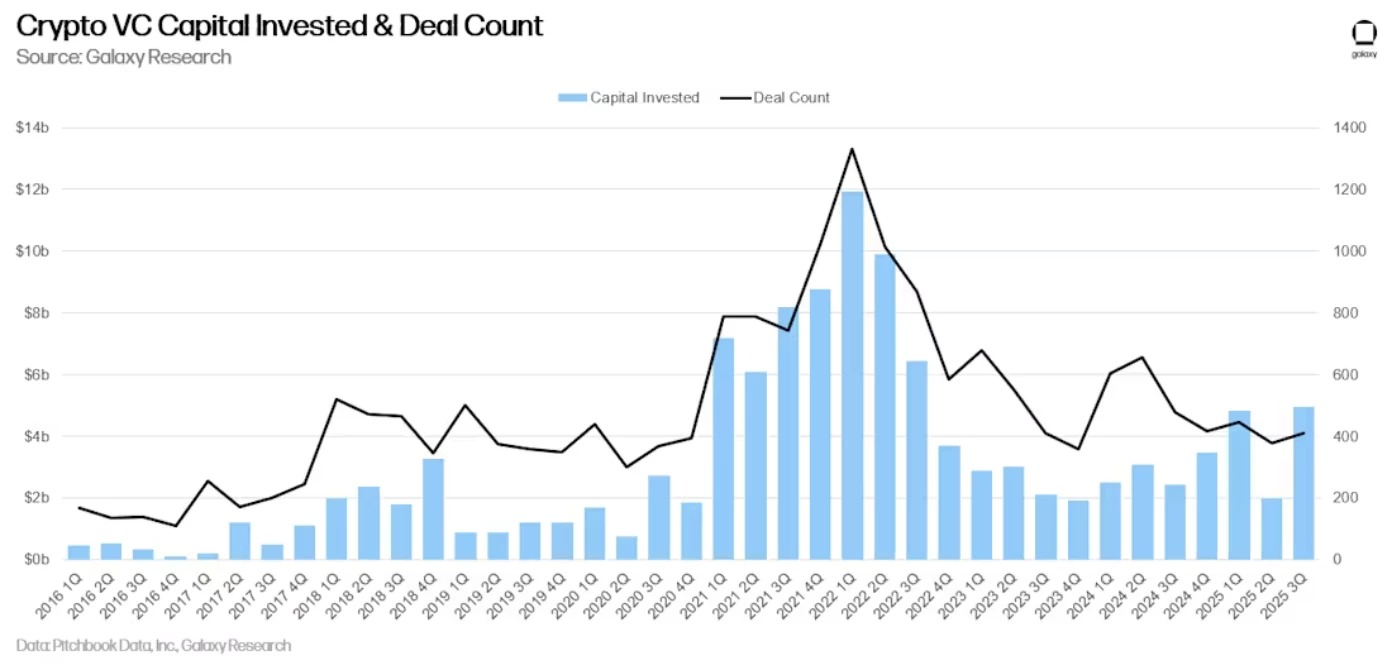

And with $4.6 billion, the third quarter of this year set a record unmatched since the unprecedented successes of 2021/2022.

Venture capital firms make a strong comeback in the third quarter

The development of the cryptocurrency sector involves significant investments by venture capital (VC) firms, which are at the forefront of supporting the most innovative areas. However, it must be acknowledged that the enthusiasm of 2021/2022 has given way to a more measured exposure to this ecosystem.

This reality was recently examined in a report published by the analysis department of crypto company Galaxy Digital, which described VC activity as “active and healthy overall” during the last quarter.

Indeed, the funds raised since the beginning of 2025 have already exceeded the totals for the previous two years, with more than $10 billion on the books, even if “the number of deals does not seem set to exceed previous years.”

And for good reason: the $4.6 billion recorded in the third quarter is already the best result since the third quarter of 2022, just before the dramatic collapse of the FTX cryptocurrency exchange platform.

In the third quarter, venture capital firms invested $4.65 billion (+290% month-on-month) in crypto and blockchain-focused startups and private companies across 415 deals (+9% month-on-month).

Investments now decoupled from Bitcoin performance

During the third quarter, seven deals alone captured half of the funds deployed by venture capital firms in crypto and blockchain-focused companies, with: Revolut ($1 billion), Kraken ($500 million), Erebor ($250 million), Trésor ($146 million), Fnality ($135 million), Mesh Connect ($130 million), and ZeroHash ($104 million).

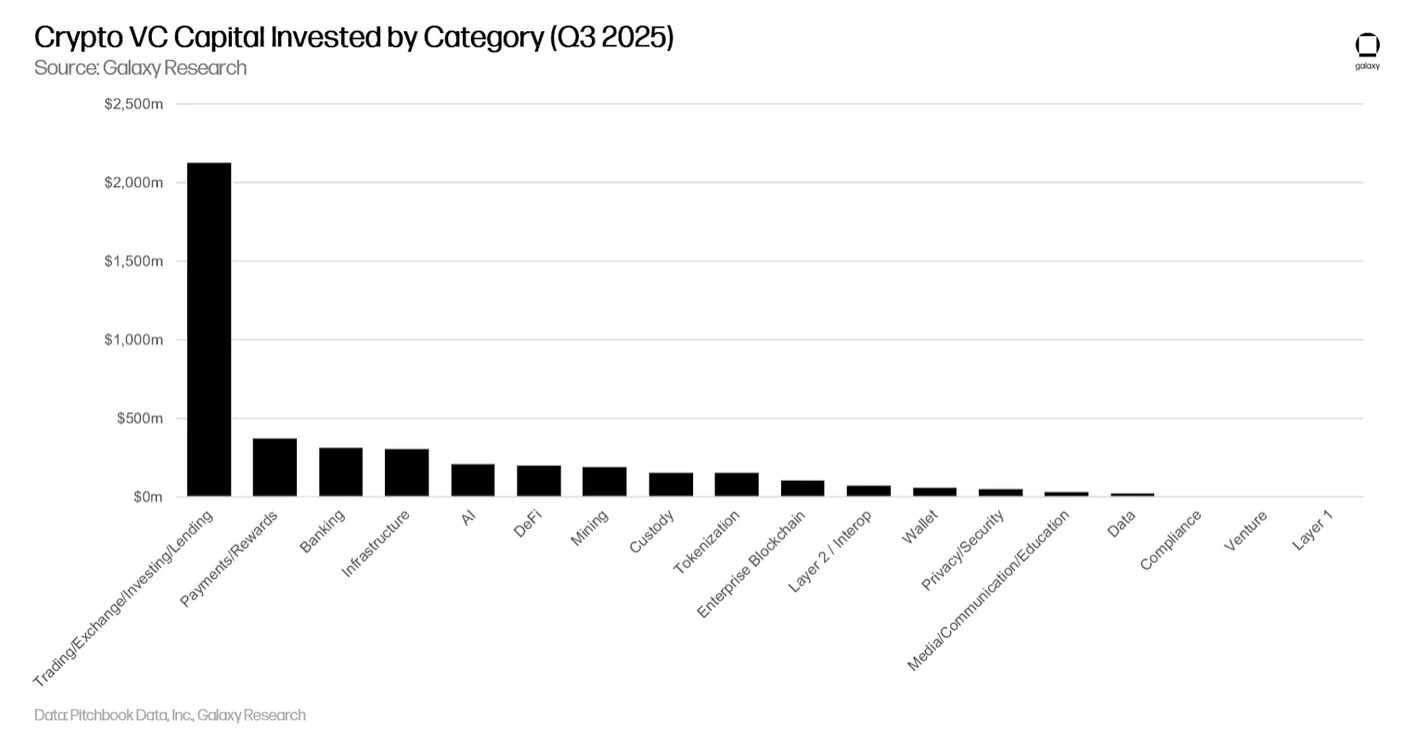

The distribution of invested capital involves companies already established (57%), while 43% involved younger structures. Which sectors are favored? In first place is the Trading/Exchange/Investing/Lending category, while Payments/Rewards and Banking are seeing significant increases.

As for pre-seed deals—as in the case of the Monad project, whose ICO has just taken place—their number has remained stable from month to month “and remains solid compared to previous cycles.” This data is considered “a way to assess the robustness of entrepreneurial activity,” while transactions involving established companies “reflect the growing maturity of the market as a whole.”

Unlike previous bull cycles, the capital invested in crypto startups is no longer directly correlated with the price of Bitcoin. Indeed, BTC “has risen significantly since January 2023, while venture capital activity has struggled to keep pace,” particularly in the face of increased competition from ETFs and Digital Asset Treasuries (DATs).

Very (too?) favorable investment contracts

Nevertheless, the strong presence of venture capital firms in the cryptocurrency sector remains controversial at times, particularly when it comes to the distribution of tokens associated with certain projects, or the favorable conditions they enjoy.

Just look at the case of the Berachain project, which is embroiled in controversy following the revelation of its agreement with the investment company Nova Digital. At issue is a right to reimbursement on its $25 million investment, allowing it to recover all of its funds if the price of the BERA token were to fall.

At the same time, venture capital firm Mercury Fund has just taken the Plasma project to court following an error—apparently corrected a little too late—in the drafting of the warrant procedure associated with the distribution of the XPL token. A shortfall of 278.5 million units, which makes a small difference.