: Which Models Are Weathering the Storm?")

Declining trading volumes and adjustments to short-term interest rates have put publicly traded crypto-related companies to the test. The Q4 2025 earnings reports reveal the impact of the market cycle on Coinbase, Bullish, Gemini, and Robinhood. Circle, with USDC, is following a distinct trajectory. What should investors take away from this?

As the Q4 2025 earnings season draws to a close, it’s time to take stock. Of the more than 80% of S&P 500 companies that have reported to date, approximately 75% have exceeded revenue expectations and nearly 80% have outperformed earnings per share (EPS) forecasts.

Today, I’m offering an overview of the results from companies closely tied to the cryptocurrency ecosystem, starting with exchange platforms.

Coinbase, Bullish, and Gemini Bear the Brunt of the Crypto Crash

All three players have naturally felt the impact of the cryptocurrency price correction, as well as, to a lesser extent, the adjustment in short-term interest rates. When trading volumes slow down and prices correct, platform fees automatically decline.

Coinbase

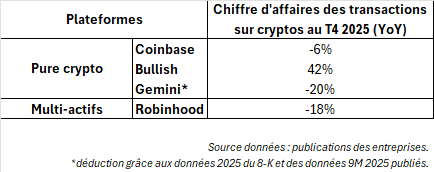

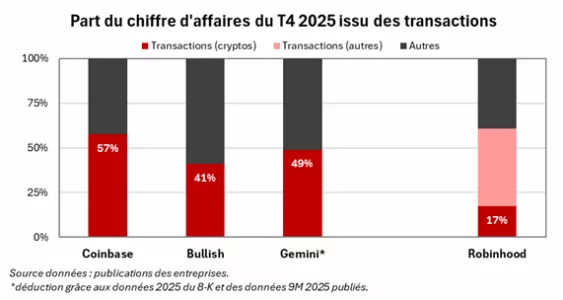

At Coinbase, the industry leader, revenue fell by 5% ($1.78 billion), driven by a 6% decline in trading revenue compared to the previous quarter.

The company is increasingly highlighting the growth of ancillary businesses such as institutional custody, stablecoins, and services, but the fourth quarter shows that these lines are not entirely decoupled from the market cycle. Subscription and service revenues also fell by 3%, impacted by the easing of short-term yields.

Bullish

Bullish, for its part, is attempting to shift its image from a spot platform reliant on retail speculation to a market infrastructure geared toward institutional flows. In Q4, the company reported $64.3 billion in “digital asset sales” (gross volume of crypto assets traded), a high figure but one that provides little insight into actual profitability.

The true indicator is “adjusted revenue” at $92.5 million, up from $76.5 million in Q3, which rose sharply despite the crypto market downturn thanks to the successful launch of its crypto options.

Management is now focusing on derivatives, with over $9 billion in options volume for the quarter and open interest reaching $4 billion as of January 31. The business model is becoming more sophisticated, but remains dependent on overall market dynamics.

Gemini

Gemini presents a very different profile, and is likely more speculative in the short term. Its (interim) Q4 results reflect a company in the midst of a transition. Activity is growing, with a 17% increase in monthly active users (approximately 600,000) and expected revenue of between $165 million and $175 million for the fiscal year, driven more by service revenue (particularly the credit card) than by transaction fees.

Nevertheless, operating expenses far exceed revenue, reaching $520 million to $530 million, resulting in a net loss of nearly $600 million and an Adjusted EBITDA that remains negative at around -$260 million. Compounding this is the simultaneous departure of the Chief Operating Officer (COO), Chief Financial Officer (CFO), and General Counsel, with responsibilities being refocused around Cameron Winklevoss.

Gemini thus becomes a restructuring story rather than a proxy for cryptocurrency prices. If credible cost cuts or a clear repositioning emerge, the stock’s turnaround could be significant, but the execution risk remains high.

Robinhood is faring better thanks to its more diversified model

Multi-asset broker and fintech firm Robinhood has also been hit by the crypto downturn, but is holding up better than “pure crypto” platforms thanks to its more advanced diversification. Its revenue remained nearly flat compared to the previous quarter at $1.28 billion (+27% year-over-year), while cryptocurrency commissions fell by 18% ($221 million).

Transactions in other markets (+20% QoQ) more than offset the decline in crypto commissions and the drop in revenue from client cash balances (-10%).

During the conference call, management emphasized the growth in client assets more than crypto volumes, reflecting a gradual shift toward a model focused on balance sheet monetization, similar to Interactive Brokers.

Circle Rides the Wave of Exploding USDC Circulation

Circle stands out completely from the other companies mentioned, as it represents a proxy for the democratization of stablecoins. Whereas Coinbase or Robinhood primarily generate revenue when investors trade, Circle derives most of its revenue from interest earned on the reserves backing the USDC (its dollar-pegged stablecoin).

In practical terms, the more USDC in circulation there is and the higher the short-term interest rates are, the more Circle’s revenue grows. In the fourth quarter, this mechanism played out fully, as the group reported a 4% increase in revenue (to $770 million), of which $733 million came from interest on its reserves.

This increase is driven by the growth in USDC outstanding, which reached approximately $75 billion in circulation (+72% year-over-year), more than offsetting the decline in the interest rate (-69 basis points) following the Fed’s rate cuts.

Once the growth in USDC outstanding approaches 0%, changes in short-term interest rates will become the main driver of Circle’s profits if the company does not diversify further.