Despite significant structural support, gold, silver, and cryptocurrencies now appear to be at risk of a major short-term correction.

Gold, silver, and Bitcoin benefit from significant long-term structural support

The long-term appeal of these three “non-sovereign” assets is undeniable, supported by three major macroeconomic forces.

The “de-dollarization” of sovereign balance sheets is accelerating

Widening government deficits, combined with the bipolarization of the world, are fueling fears of chronic “debasement” of fiat currencies. Above all, the threat of the “weaponization” of the dollar—following repeated economic sanctions and the freezing of Russian assets linked to the war in Ukraine—has catalyzed a diversification trend.

Central banks have purchased more than 1,500 metric tons of gold since 2023, bringing the total value of their gold reserves (approximately $4.5 trillion) above that of their holdings of U.S. Treasury bonds (approximately $3.5 trillion)—a first in nearly three decades, according to data compiled by the ECB and the World Gold Council.

The Erosion of the Fed’s Credibility

Persistent U.S. inflation above the 2% target, combined with political pressure to lower rates, is undermining the central bank’s credibility in its mission of “price stability.” This implicit tolerance for inflation reinforces the credibility premium of real and alternative assets.

The recent decline in real yields

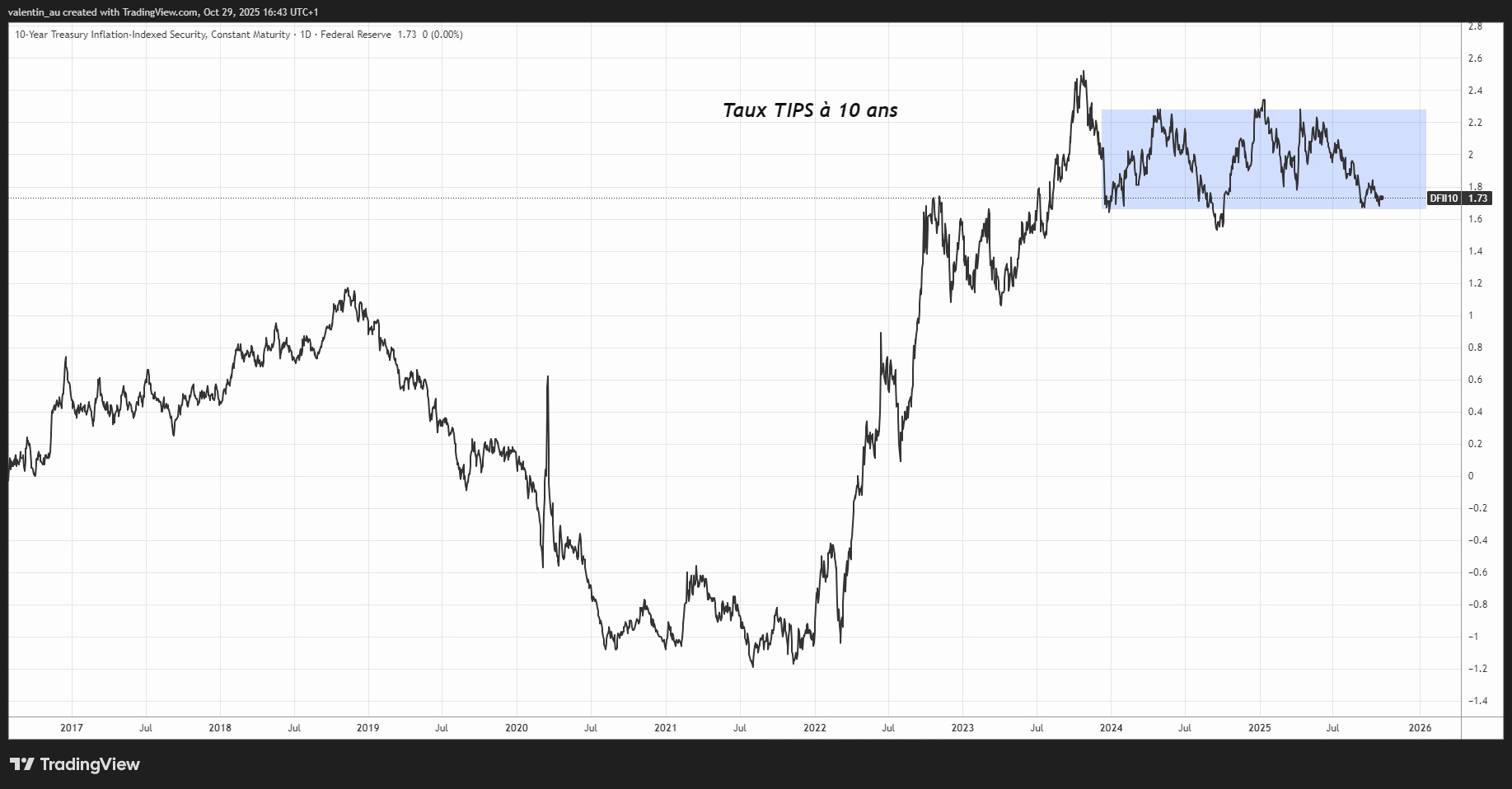

When bond yields, after adjusting for inflation, decline, the opportunity cost of holding a non-coupon-bearing asset decreases, making them more attractive to investors. In other words, when safe investments yield less in real terms, investors turn more to tangible assets such as gold or Bitcoin, which then serve as stores of value. These real rates remain within a manageable range for these three assets. The yield on 10-year TIPS has, in fact, continued to decline recently, standing at 1.69% at the end of October. A further decline in these real rates would support precious metals and Bitcoin, while a rebound would amplify the correction seen in recent weeks.

Chart of the 10-year yield on U.S. inflation-indexed Treasuries

Structural support, but the risk of a short-term correction prevails

While the long-term fundamentals are positive for all three assets, momentum is beginning to wane in precious metal prices after months of nearly uninterrupted gains, while a major technical signal is putting an end to Bitcoin’s bullish momentum.

Positioning in the two precious metals suggests a trend that has now turned euphoric. Inflows into gold ETFs have reached historically high levels over the past three months, close to three standard deviations above their three-year average. At the same time, the positioning in futures and options contracts by commercial hedgers (producers and refiners) is two standard deviations below the three-year average. Historically, this pattern often coincides with tactical peaks and consolidation phases, as seen last April. The price of gold, which recently hit $4,400 per ounce, is therefore particularly vulnerable to a wave of short-term profit-taking.

Silver is in a similar situation, but its potential for a correction could be offset by its growing industrial use, particularly in solar panels and electric vehicles (accounting for approximately 50% of global demand).

Chart showing the gold price, the percentage of long positions held by ‘commercial hedgers’ in futures and options (in pink), and flows into major gold ETFs (in blue)

From a technical perspective, the Bitcoin price has just broken below a key support level at $108,000, where it had been consolidating since July. This move thus forms a “double top” pattern, theoretically paving the way for a bearish reversal.

This bearish signal is all the more significant as it coincides with the well-known “Bitcoin 4-year cycle,” which suggests a theoretical peak in October followed by a sharp correction over the next twelve months—similar to what occurred in 2018 and 2022.

Bitcoin price chart

In conclusion, the imbalance now appears to favor sellers across all three assets for distinct reasons: the excessively optimistic positioning in precious metals and the break below a major support level for Bitcoin. Nevertheless, the acceleration of de-dollarization, the loss of credibility in the Fed’s independence, and the decline in real interest rates provide a structurally bullish environment. These fundamental factors could reduce the duration and magnitude of the correction, transforming tactical risk into an opportunity for long-term investors to build their positions.