")

As Stream Finance revealed a loss of $93 million, its XUSD collapsed, revealing contagion among other decentralized finance protocols.

With the expertise of Pascal Tallarida, founder of Jarvis Network and trainer for Alyra, we look back at the various players affected, the ins and outs of this case, and the dangers it may pose for DeFi.

Is the Stream Finance case and its XUSD putting DeFi at risk?

In recent days, yield hunters’ nerves have been put to the test in decentralized finance (DeFi), first with Monday’s $130 million hack on Balancer (BAL), and now with the scandal surrounding Stream Finance and its XUSD.

As a reminder, the protocol teams revealed a loss of $93 million, attributed to “an external fund manager.” However, this hole in the coffers directly affects XUSD reserves, which could be described as a stablecoin in a loose sense, but which in reality is more of a yield token that offered up to 18% compound interest before the crisis.

While before the events, the protocol claimed $530 million in assets under management, with $163 million in total value locked (TVL) from users, that same TVL is now $94 million, according to data from DefiLlama.

Taken in isolation, these losses, while significant, remain largely manageable for the DeFi ecosystem. The problem here is that in the Stream Finance case, a contagion effect is being demonstrated across several protocols.

Lending loops amplify risk

At the same time, Pascal Tallarida, founder of Jarvis Network and trainer for Alyra, discusses the case of lending loops, or looping, which involves borrowing an asset to deposit it as collateral and then borrowing again. This maximizes returns, but also increases risk:

There are lots of investors who have started looping. They bought XUSD, deposited it in money markets, borrowed USDC or other stablecoins, and bought XUSD again. The team behind XUSD did this themselves. In other words, it borrowed dollars from various protocols [Morpho, Euler, editor’s note].

It was largely through this strategy that Stream Finance claimed more than $500 million in assets under management, a double count without which the true TVL was lower.

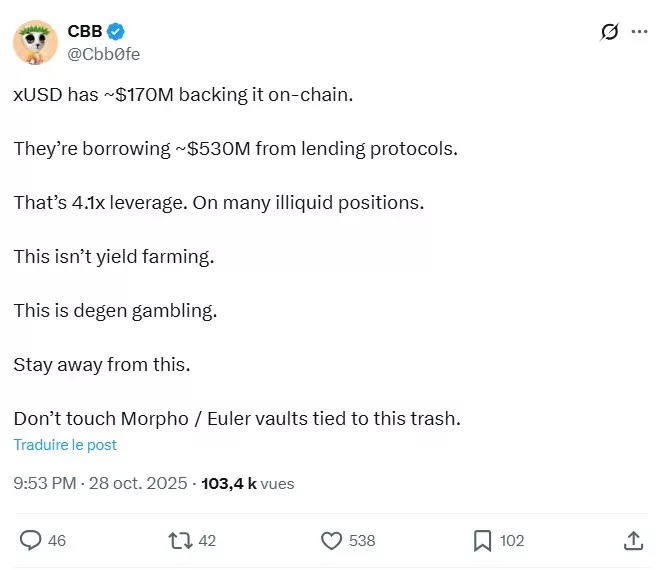

This practice raised questions from the community, in response to which the protocol teams promised to provide proof of reserves in recent days. Among the warning signs, we can cite this tweet from October 28:

On DefiLlama, TVL began to fall on October 27, indicating either insider trading or a loss of investor confidence. Since the events we now know about, many positions are now blocked, as Pascal Tallarida explains:

The problem is that since XUSD was used as collateral pretty much everywhere, the priority of those who lent USDC or other assets while accepting XUSD as collateral was to withdraw their funds. However, the only funds you can withdraw are those that have not yet been borrowed, so all pools with XUSD as collateral have risen to 100% utilization and interest rates have increased. […] Positions are at risk of being liquidated, but people today do not want to liquidate XUSD, because there is no point in liquidating to recover an asset whose true backing is not yet known.

To understand what follows, we must first review several important concepts in these remarks. Regarding liquidation, it should be remembered that when a position is no longer sufficiently collateralized, liquidators close the position using the capital deposited as collateral, and the original owner is also penalized. The operation is then profitable for the liquidators, who keep the bonus from the penalty after the remaining capital has been used to cover the losses.

For funds locked in pools, this is true in the case of protocols such as Morpho or Euler, which use vaults in which a specific asset can generally be borrowed against another given asset. This is less the case with applications such as Aave, where several authorized collaterals can be used to borrow several authorized assets.

Did the curators amplify the crisis?

After this necessary explanation, we now come to the heart of the Stream Finance problem, namely contagion to other DeFi applications, which is reminiscent of the UST case, albeit on a much smaller scale.

To understand this, we need to highlight the role of curators, namely third-party agents who define strategies for assets borrowed via vaults, particularly in terms of risk management and allocation. Here, it appears that a number of protocols could be affected by the XUSD crash:

Added to this is the fact that many projects were found to have indirect exposure to XUSD. These projects are now impacted, such as the Trevee project, which chose to work with MEV Capital, and MEV Capital decided to lend the funds entrusted to it against XUSD as collateral. Admittedly, that’s not all they did, but with the decline in TVL and withdrawals from the protocol, the share of funds lent against XUSD has grown to 92%.

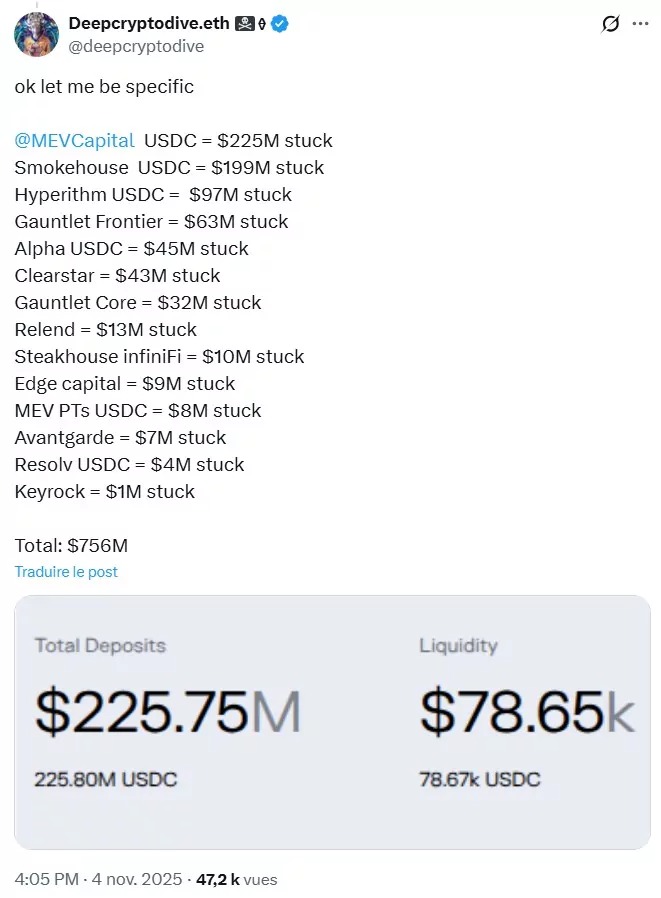

According to Deepcryptodive.eth, which oversees risk for on-chain asset manager KPK, a total of $756 million is also reportedly locked in various vaults on Morpho Labs, given exposure to XUSD:

It should be noted, however, that Morpho has relayed the statements of several of its partners, who maintain that they have no exposure to XUSD. This is the case, for example, with Steakhouse Financial, Gauntlet, and Felix Vanilla.

For his part, Paul Frambot, co-founder and CEO of Morpho Labs, took to X to defend his view of the situation:

A vault is comparable to an on-chain fund, and just like traditional funds, some will perform well and others will not, but that is something we must accept and mitigate if we want to build a truly open and decentralized system. The fact that only one vault out of approximately 320 on the Morpho app was exposed, even partially, to xUSD does not prove that the model is ineffective; quite the contrary. Thanks to Morpho’s isolated market and vault model, the more than 319 other vaults and their depositors, each with a different risk profile, were not exposed.

A still imperfect system

While the current situation raises questions about how returns are generated in DeFi, it is important not to wrongly blame Morpho or any other protocol that may have been unwittingly involved in this crisis.

However, the coming weeks could be instructive in terms of the extent of this situation, which should serve as a lesson not to transpose the mistakes of traditional finance to DeFi. Indeed, Pascal Tallarida points out that DeFi “has become really complex”:

On money markets such as Morpho, curators allocate your funds across different markets. They are the ones who decide on collateral, so they can accept new collateral overnight without asking your opinion. More and more protocols are entrusting their funds to curators to manage their liquidity. This is undoubtedly a very good model for the future of DeFi, but it is a model that can be improved, particularly in terms of transparency regarding the actual risks taken by curators. That is why there is regulation in traditional finance. These are still human beings who make mistakes; mistakes that are sometimes honest, sometimes motivated by greed.

However, while our interviewee “believes that curators have amplified this crisis on XUSD” and “hopes that there will be an aftermath,” he does not lump everyone together. Like Paul Frambot, he points out that “the majority of [DeFi] vaults are not exposed to XUSD.”

Although many curators have not touched this product, a few bad apples can cause everyone to be lumped together.A turning point in DeFi?

In conclusion, Pascal Tallarida emphasizes the human factor, which is becoming increasingly important in DeFi:

What this year has taught me is that we have more and more humans in DeFi. Originally, DeFi was supposed to be something deterministic where you just had to trust the code. Sure, there were human errors, but they were limited. Now, with curation, I think we’ve returned to a model where humans are very important because they make decisions.

If the markets turn around for the long term, other problems besides that of Stream Finance could come to light, as was the case in 2022.

Add to that the Balancer hack we mentioned at the beginning of this article, and investor confidence could erode, triggering capital withdrawals. On Ethereum, this is not yet the case, if we report the TVL in ETH equivalent, but it remains a statistic to watch.

It’s also worth remembering that problems sometimes take time to come to light, as evidenced by the Moonwell hack, in which the attacker stole $1 million worth of ETH twice in less than a month. On Tuesday, on-chain data also revealed that he had attacked Venus Protocol for $664,000 and Takara Lend for approximately $450,000, as well as other protocols for smaller amounts.

The ecosystem will undoubtedly recover from this setback, but these stories will fuel the pro-regulation rhetoric of certain detractors when prices turn around for good.