Bitcoin’s 4-year cycle and the cyclical bear market could be the trap at the end of 2025. Read analyst Vincent Ganne’s explanation.

$126,000 may not be the cyclical peak

For over a decade, the dominant analytical framework for the Bitcoin market has been based on the four-year cycle theory, centered around the halving. This mechanism, which cuts BTC issuance in half, has historically driven the major phases of price increases, euphoria, and subsequent corrections in the asset.

However, since the bottom in late 2022, several major anomalies have called into question the robustness of this model. The question is no longer just where we are in the cycle, but whether this cycle still makes sense in an environment where Bitcoin is now evolving as a global, mature, and macro-sensitive asset.

First anomaly: the supposed cyclical peak in October 2025 ($126,000 on October 6) does not align with traditional business cycle benchmarks. The Copper/Gold ratio, an excellent proxy for risk appetite and the strength of the global economic cycle, shows none of the characteristics of a macroeconomic peak.

Historically, major peaks in the Bitcoin price (2013, 2017, 2021) have coincided with an overheated industrial cycle, as reflected by a high Copper/Gold ratio nearing its peak.

However, in 2024–2025, this ratio remained depressed, with no comparable upward momentum, and even showed recurring signs of weakness. If Bitcoin has indeed formed a cyclical peak, then it is occurring in complete contradiction to the global cycle—something that has never happened before.

Does the 4-year cycle driven by the halving still make sense?

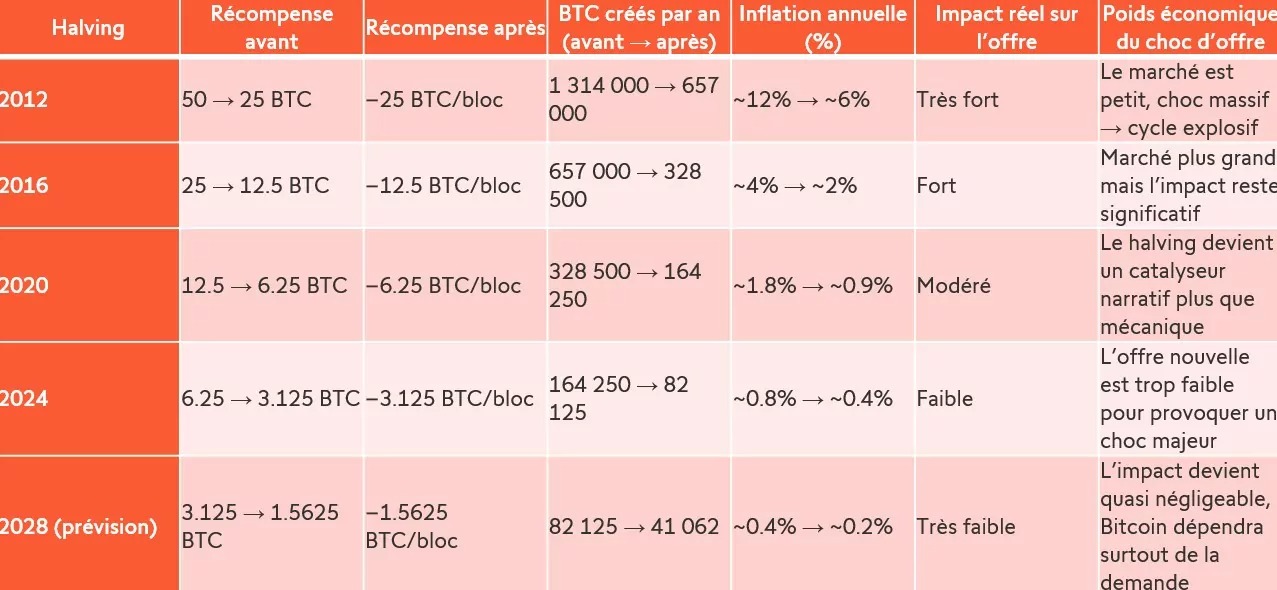

Second anomaly: the halving loses a little more of its mechanical impact each time. The data is clear: in 2012, the halving cut Bitcoin’s monetary inflation in half, reducing annual issuance from 1.3 million to 657,000 BTC. In 2016, then 2020 and 2024, this effect gradually diminished: 12% → 6%, then 4% → 2%, then 1.8% → 0.9%, and finally just 0.8% → 0.4%.

With this halving of an increasingly smaller peak (by 2028, the impact will be almost negligible), the relevance of the 4-year cycle centered around the halving is thus called into question. The halving is no longer a supply shock capable of mechanically fueling an explosive cycle (and thus a bear market?); it has become a narrative catalyst (perhaps now merely psychological), whose actual impact increasingly depends on the macroeconomic context, global liquidity, and institutional demand.

In this context, a question arises: does the traditional 12-month cyclical bear market still make sense? If the four-year cycle is less and less dictated by supply, and increasingly by macroeconomics and institutional flows, then the very structure of Bitcoin’s cycles could be evolving toward a model closer to that of traditional assets: phases of expansion and contraction linked to global liquidity, real interest rates, and the global economic cycle.

Perhaps we are no longer in a simple “Bitcoin cycle,” but in a macro cycle with Bitcoin as part of it. And if that is the case, then the timing of the cyclical bear market no longer has any mechanical or predictable basis, and it could be the major trap at the end of 2025.