Despite a sharp drop on January 30, gold and silver prices have crossed symbolic thresholds, with a meteoric rise in just a few months and record volumes. Beyond the monetary narrative, the current dynamic resembles a market driven by flows, against a backdrop of absorption of global excess savings. A powerful but unstable engine. Is this rise in precious metal prices coming to an end?

Gold is gaining momentum, silver even more so

Gold and silver have been rising sharply for several months. The rise that began in recent years has accelerated significantly, to the point where an ounce of gold exceeds the $5,000 threshold and an ounce of silver exceeds $100.

After rising more than 60% in 2025, the price of gold has already gained more than 15% since the beginning of the year as of January 30.

Silver, which soared by more than 140% in 2025, has risen by around 40% since January 1. This acceleration can also be seen in the speed of price increases. It took gold nearly 1,700 days to rise from $2,000 to $3,000.

It took only 207 days to reach $4,000, then just 111 days to cross the $5,000 threshold. This compression of the time needed to gain each $1,000 illustrates a change of regime that goes beyond the simple debate about the intrinsic value of the metal.

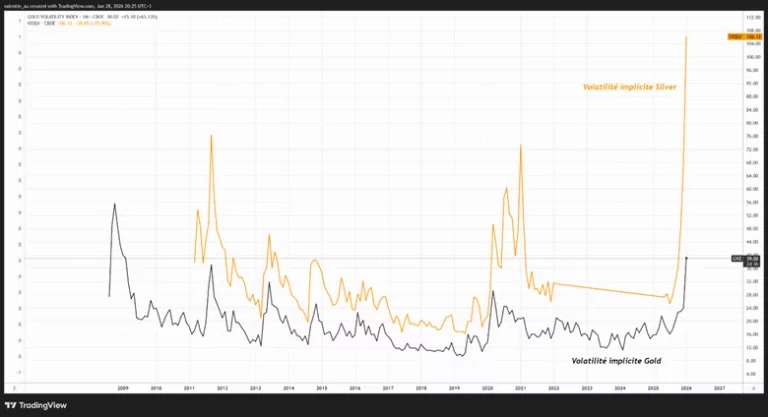

On a linear chart, the rise in these metals appears naturally parabolic. The most useful information is found on the logarithmic chart, where the slope has also risen sharply in recent months, particularly for silver.

Historically, this type of configuration, characterized by both a sharp acceleration and an unusually large deviation from the long-term average (5 years on the chart), is typical of periods of intense speculation, even when the underlying fundamentals are very real, as was the case with cocoa in 2023 or gold and silver in the early 2010s.

A market driven by speculative flows thanks to an appealing narrative

It is tempting to explain the surge by pointing to a loss of confidence in US assets, questions about the status of the dollar, or the perceived erosion of the Federal Reserve’s (Fed) independence. These factors exist and form a coherent narrative, but they alone do not explain the extreme convexity observed in recent months. Market data confirms a reading that is more “flow” than “fundamental.” The year 2025 was marked by record inflows into gold exchange-traded funds (ETFs). More recently, the CME Group announced an all-time high of 3,338,528 contracts traded on its metals complex on January 26.

The mechanism is simple: the more momentum a market shows and the more it crosses symbolic thresholds, the more it attracts flows, which further reinforces the momentum. The loop is self-perpetuating and can last longer than expected, until the narrative supporting it begins to weaken, often even before the fundamentals change.

Gold and silver as a “reservoir” for excess savings

In addition to the speculative dimension, there is a more structural factor that is often underestimated: the absorption of global excess savings.

For many years, beggar-thy-neighbor policies have kept the dollar artificially strong by attracting capital flows, preventing exchange rates from fully playing their role in adjusting trade imbalances. In this context, a persistently strong dollar has become the norm, despite persistent U.S. trade deficits.

If these deficits are no longer automatically offset by inflows into dollar assets, then exchange rate adjustment once again becomes the dominant mechanism, which automatically weighs on the dollar.

In a world still dominated by mercantilist growth models, excess savings must be recycled. However, there is no reserve alternative deep enough to absorb this excess on a lasting basis. At the same time, the US administration is showing decreasing tolerance for the absorption of these savings without compensation. As a result, some of this excess savings could be redirected towards gold and silver, which are establishing themselves as neutral reserve assets by default.

What could break the upward momentum

There is a solid fundamental base. But as prices rise, economic players are adapting.

The Financial Times recently noted that, with prices around $112 per ounce, silver now accounts for up to 26% of the total cost of a photovoltaic module. Faced with this increase, manufacturers are accelerating their thrifting and substitution strategies, particularly through copper contact technologies. Industrial demand is therefore becoming more elastic.

In a flow-driven regime, a simple change in perception could also halt the rise. Geopolitical appeasement, such as a trade agreement between Donald Trump and Xi Jinping or diplomatic progress in Ukraine, could be enough to undermine the dominant narrative. Similarly, a monetary policy shock, or simply a reassessment of the Federal Reserve’s trajectory, could trigger a coordinated wave of profit-taking. In this context, the White House’s announcement on Friday, January 30, of Kevin Warsh’s nomination as Fed chair may have undermined the narrative of an overly accommodative Fed. Warsh may have recently won over the US president with his partisan and accommodative rhetoric, but his track record links him more to the camp of those in favor of a restrictive policy, with increased vigilance on the risk of inflation.

During the 2008 crisis, as governor, he was reluctant to extend monetary easing after the collapse of Bear Stearns, and then continued to insist on inflationary risks in the fall after the collapse of Lehman Brothers, even as the economy shifted into a disinflationary environment. This contrast between a recent tone that is considered accommodative and a restrictive past could be enough to destabilize a market that is already heavily positioned, thereby weakening the marginal driver of the movement. Finally, technical factors matter. Stabilization or even net outflows from gold ETFs could weaken the conviction of recent buyers. Record levels of activity combined with high volatility also increase the risk of episodes of deleveraging, i.e., forced reduction of exposures. In this context, an increase in margin requirements decided by the CME clearing house on gold and silver futures contracts, a common practice in times of tension, could act as a catalyst for normalization.

Conclusion

The bullish thesis on gold and silver is not based solely on geopolitics or monetary mistrust. It is mainly due to a combination of self-sustaining speculation and the redeployment of excess global savings into “neutral” reserve assets. As long as flows remain oriented towards buying, the momentum may continue.

The breaking point will likely come from a single factor: a shift in ETF flows, a reversal in the dollar and real interest rates, tighter margins on derivatives, or a political and monetary shock that undermines the narrative. If these signals appear, normalization could be rapid, as the rise has been.