")

The tokenization of real-world assets (RWAs) is redrawing the boundaries of traditional finance, to the point of worrying members of the Bank for International Settlements (BIS). At issue is the development of tokenized money market funds, which have the potential to amplify the risks associated with traditional finance.

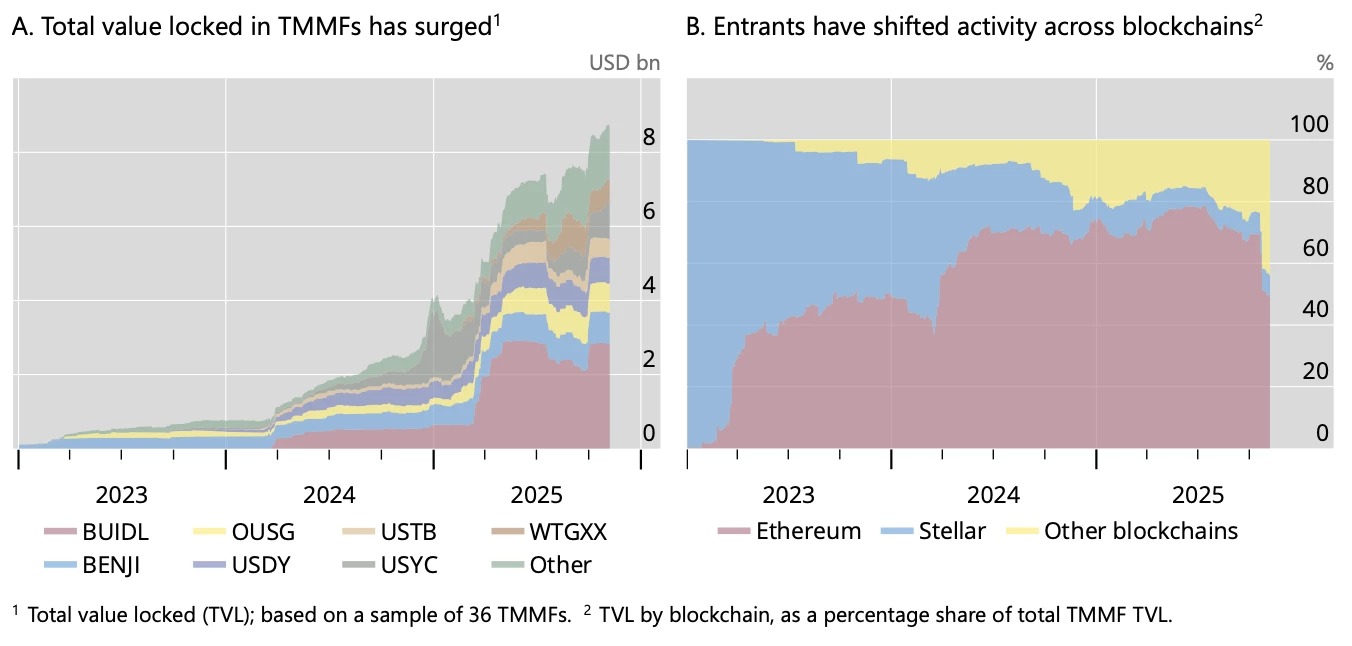

Unprecedented growth in tokenized money market funds

The Bank of Central Banks, also known as the Bank for International Settlements (BIS), often takes a negative stance on the many advances associated with the cryptocurrency sector.

This mistrust has now been applied to the significant growth of the tokenized money market fund (TMMF) market, which has grown by 265% over the past year. This is particularly due to the presence of traditional finance giants such as BlackRock and its BUIDL fund, and Franklin Templeton.

After a slow start, TMMFs have grown rapidly over the past two years. The total value locked (TVL), equivalent to assets under management, was only around $770 million at the end of 2023, but has increased more than tenfold to nearly $9 billion at the end of October 2025.

The reason for this success? An ability to maintain a certain stability while allowing on-chain interest to be distributed to their holders, unlike US stablecoin issuers who cannot offer this type of passive return. Unless the companies concerned delegate their management to third parties, as in the case of Coinbase and PayPal.

At the same time, these TMMFs issued in the form of tokens “share the key features of stablecoins, such as peer-to-peer transactions and programmability via smart contracts.” This is of interest to users of decentralized finance (DeFi) who are constantly looking for reliable and available collateral.

Risks that mirror and may amplify those of conventional funds

Currently, investments in these funds are limited to portfolios approved using tokens (ERC-1400/3643) that can block transfers to unlisted wallets. However, this restriction can be quickly circumvented with wrapped tokens or by using certain platforms.

A boom in the ability to make these tokenized money market funds the “foundation of the future financial system.” This is an opportunity for BIS analysts to sound the alarm by demanding “prudent risk management essential to maintaining confidence.”

Tokenized money market funds give rise to risks that mirror—and may even amplify—those of conventional funds of the same type and stablecoins.

This amplification could occur because “the transparency of on-chain transactions can exacerbate liquidity risk by serving as a coordination mechanism between investors.” But it could also occur because of the principle of “composability” specific to DeFi, which interlinks protocols with each other like financial Legos.

And what about leveraged borrowing strategies (looping), which involve “putting TMMFs up as collateral to borrow stablecoins in order to buy more TMMFs”? All of these situations could accentuate certain propagation effects, particularly in the context of a market shock.