Arthur Hayes, former CEO and founder of cryptocurrency exchange BitMEX, is abandoning memecoins in favor of the secure, high returns offered by decentralized finance. But memecoins are already dead anyway: make way for creator coins.

Arthur Hayes abandons memecoins

Since being pardoned by Donald Trump, the former CEO of BitMEX has become increasingly present in the American crypto ecosystem.

Based in Hong Kong, where he manages his money and his family office Maelstrom (with $6.46 billion in assets under management), Arthur Hayes showers the ecosystem with his knowledge of memecoins, monetary theory, and financial markets.

The 42,000 subscribers to his newsletter can take full advantage of his insights, which are often focused on his own investments—a happy coincidence.

Is Arthur Hayes always in the right place at the right time? Or is he promoting his investments in order to use his subscribers as exit liquidity? A little bit of both.

According to Arthur Hayes, the investments that deserve investors’ attention today are no longer memecoins, such as PEPE and MOTHER, which he has long promoted while calling them “dogshit.”

His sights are now set on safer projects, such as those in decentralized finance. Safer, but potentially more profitable, as he sees the potential to earn 3,400%, 5,100%, and 13,000% respectively in EtherFi, Ethena, and Hyperliquid.

Please note that these predictions are solely those of Arthur Hayes. He holds significant positions in these three projects, both personally and through his investment fund.

Beyond promoting his own projects and companies that share his vision, such as Ethena, Arthur Hayes is known for anticipating different market cycles.

On the other hand, won’t stablecoins (Ethena) and decentralized finance (Hyperliquid) become pillars of the global economy, generating trillions of dollars and replacing the most powerful financial institutions on the planet? It’s a possibility.

Every stock, every bond, every fund—every asset—can be tokenized. If they are, it will revolutionize investing.

Larry Fink, CEO of Blackrock

Memecoins are over, we need to move towards decentralized finance: that’s the gist of Arthur Hayes’ message, delivered during an interview with YouTuber Kyle Chasse. But should we trust him? Are memecoins really dead and buried?

Memecoins? They’re not what they used to be

In previous cycles, memecoins captured everyone’s attention. Journalists and YouTubers told crazy stories of immense fortunes built overnight with an investment of just a few hundred dollars. It was a speculator’s paradise. Memecoins created this controversial image of cryptocurrency: an absurd investment with no real value that could make you very rich, very quickly. This was true for the first memecoins, Dogecoin and Shiba Inu. It was slightly less true for the slew that followed on Ethereum and Solana, and even less so for the hundreds of thousands of coins created via pump.fun.

On Pump.fun, there are approximately 100,000 active addresses for $1.2 billion in memecoin capitalization, or $10,000 per address on average.

In 2021, the market cap of memecoins was $80 billion for 900,000 active addresses, or nearly $90,000 per address on average. Source: Coinmarketcap. This particular site, pump.fun, marks the final phase of memecoins as we have known them.

A kind of metastasis, a moment when things go completely haywire in the most chaotic way possible. Everyone has their own memecoin, and the money invested is diluted to the point where no one makes any money, except for two or three clever people who pull the strings of marketing or the market.Memecoins weren’t totally meaningless

However, this isn’t the end. Rather, it’s the beginning of a new cycle in which traditional finance is also involved.

Take Tesla, for example. Tesla’s share price does not seem to be linked to the number of cars sold. For Elon Musk’s admirers, this is normal: Tesla is a robotics company. Or an AI company, or an autopilot company, or a battery charging company, etc.

The idea is that Tesla is not judged on its results as a company. Rather, it is a way of investing in Elon Musk’s genius. No matter what, he will eventually find something that works. The public is therefore fond of this stock. Tesla is a bit like a memecoin. Elon Musk has treated it as such, with statements and declarations that have angered the Securities and Exchange Commission (SEC). And, naturally, Elon Musk was drawn to Dogecoin and memecoins: it’s his world.

When Donald Trump launched his “memecoin,” it also became a way to invest directly in the President of the United States. It’s assumed: these memecoins will never have a purpose other than to offer the public a way to speculate on a personality.

No more need for a supposed roadmap or white paper. These cryptocurrencies don’t want a shaky decentralized finance protocol, or a staking system that no one will use and its exorbitant fees. Pure speculation, no utility.

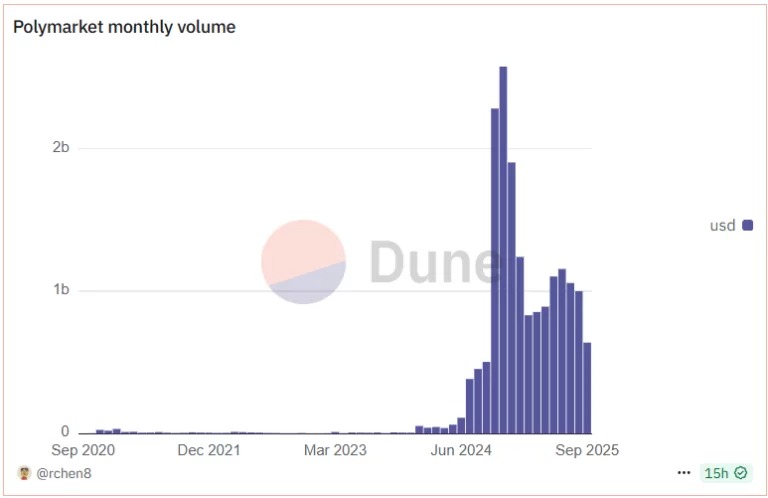

This evolution of finance, which Satoshi Nakamoto did not foresee, is consistent with the evolution of the world. Polymarket’s predictive betting is moving in the same direction: speculating or betting on anything and everything, from children dying in bombings to the weather.

Another wave of cryptocurrencies has emerged, at the intersection of this widespread speculation and the internet: creator coins, or live-stream coins, cryptocurrencies associated with online content creators.

The era of creator coins

The Internet has revolutionized the world. Newspapers, movies, and television, the euro and the dollar—these are all prehistory. Contrary to what is often said, cryptocurrency is not “Internet money.” It is money in the Internet era.

With creator coins, the world continues to evolve.

Memecoins were the precursors. But they were just jokes. Soon after the first memecoins arrived, all the good jokes had been made. All the memes had been used, all the possible and imaginable references, all the stars, all the rappers we had forgotten.

Everything had been done, all possible value had been extracted. And there are only so many things you can say with a memecoin, which consists simply of a name, an image, and possibly an X account.

Yet the internet is the cradle of creation, sharing, and content. That’s precisely what memecoins were missing: content, substance, stories. Tesla works because Elon Musk entertains us every day. The same goes for Donald Trump.

What if TikTok had a child with cryptocurrencies?

What would happen if TikTok had a child with cryptocurrencies? Just watch the live streams on pump.fun to find out.

These coins had been removed, however. As soon as they appeared in 2024, abuses exploded, foreshadowing a dark future in which the most atrocious acts, filmed live, would be rewarded with a handful of dollars. This vision was captured and shared in the first episode of season 7 of Black Mirror. We can easily understand the anticipation surrounding the British series. On Instagram, YouTube, and TikTok, the most foolish behaviors generate the most traffic, interactions, and money. Taking risks in dangerous neighborhoods to have a gun pointed at your face, assaulting people, giving toothpaste sandwiches to homeless people to eat—there is no shortage of ideas.

But live streams on pump.fun have made a big comeback. Money has no smell! It’s not dangerous content, it’s the attention economy. Attention can be monetized, it’s a market, and there’s nothing wrong with that. It’s not seen as a risk, but as an opportunity.

With the return of live streams on pump.fun, we will probably quickly see a return to unbelievable acts, such as the user who set himself on fire live to earn money, suicides, acts of unprecedented violence, or gratuitous assaults. However, there is still some good to be found.

A social network that gives power back to users

If the moderation of the “decentralized” pump.fun platform manages to maintain a semblance of calm, pump.fun could become the ultimate social network. A place where members retain more than half of the value created, keep their data, and are not bombarded with advertising.

This app would be functional and meet a need, offering a real use case for decentralization while leaving the value with the content creators. A model like Twitch, but better.

On average, social networks keep 50% of the value produced by content creators.

Public data

Pump.fun is not the first project to seek to redistribute value via a decentralized version of a platform. For example, the Brave browser offers to share the revenue generated by advertising. But the company has not found the right balance in its business model, the Brave token (BAT) has lost 90% of its value, and the product has never been able to compete with Google.

This is the main problem with decentralized redistribution: the business model. How can you pay yourself and cover the platform’s costs while still rewarding the content creator? How can different, sometimes contradictory, pricing dynamics coexist on a single cryptocurrency?

The answer: by using different cryptocurrencies. In the case of pump.fun, each creator is assigned their own cryptocurrency, a creator coin, associated with their account. The platform raises money through the Initial Coin Offering of its token, the PUMP. It has been a resounding success, raising $600 million in 12 minutes. For their part, content creators do not see their own cryptocurrency impacted by price movements related to the company or other creators. Everyone has their own little kingdom and currency. With PUMP as a source of funding for the company, wealth for the team, and a creator coin specific to each content creator, everyone can live their own little adventure without encroaching on their neighbor’s. Revenue sharing is no longer even an issue: the creator coin belongs to the creator. They are the only ones who own it (along with their followers): the platform becomes what it should always have been: a space for connecting people, without that intrusive middleman who takes his cut, imposes his rules, steals data—in short, without Mark Zuckerberg.