Thanks to their IPO documents, we can see that Gemini and Bullish used a controversial accounting rule. Were their financial results overstated?

Gemini and Bullish use a controversial accounting rule in their accounting

While the Bullish cryptocurrency exchange finalized its Initial Public Offering (IPO) last week, Gemini is expected to follow suit soon, becoming the third exchange platform to go public in the United States.

However, it appears that the accounting of both companies has been somewhat embellished thanks to a new accounting rule, seemingly to please investors, as pointed out by our colleagues at Protos:

Bullish’s IPO started at $95 and reached $118 before collapsing to $64 a week later. Without the new FASB ASU 2023-08 rule allowing cryptocurrencies to be valued in income statements, their last two financial years would have been negative. Accounting lobbyists got exactly what they wanted.

In concrete terms, this famous accounting rule has already been adopted by Strategy for several quarters, and we highlighted its potential abuses a few weeks ago, while Michael Saylor’s company claimed a supposed profit of $10 billion.

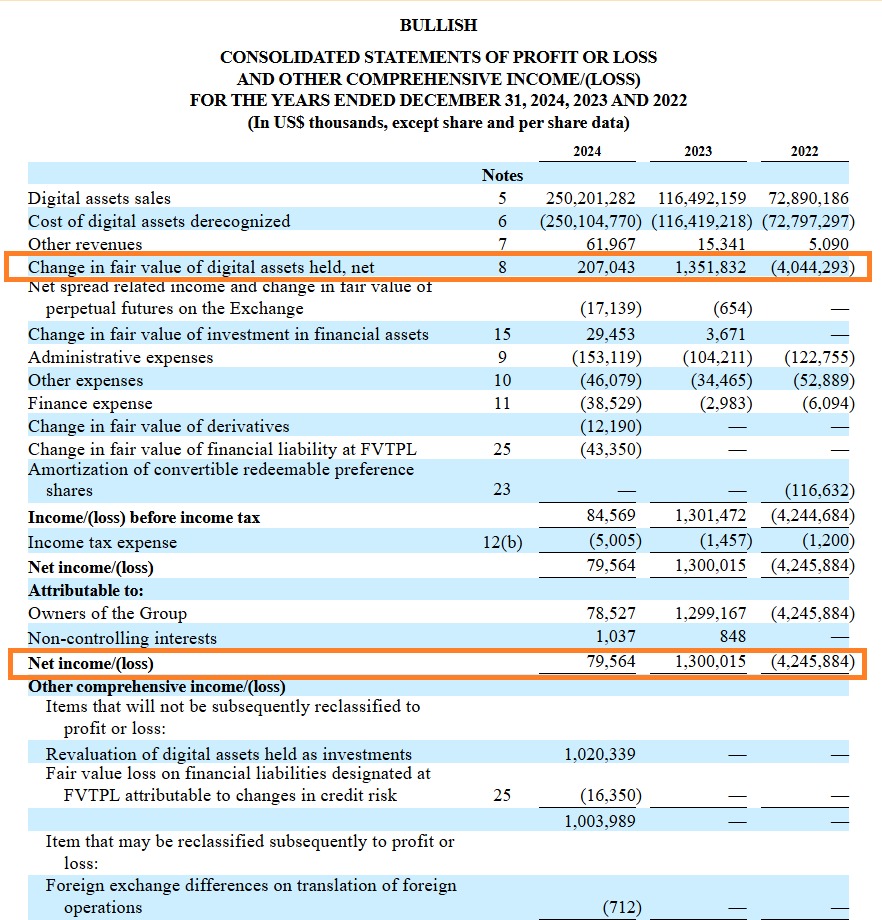

Regarding Bullish, where the exchange posted net revenues of $70.56 million in 2024, it should be noted that the company also classified $207 million in unrealized gains on its cryptocurrencies as part of those revenues. Without this, Bullish’s net revenue would have resulted in a loss of $127.48 million:

As for Gemini, the situation is a little more worrying. And for good reason: we are looking at $282.47 million in losses over the first six months of the year. However, unrealized gains in cryptocurrencies are included in this balance sheet. Without them, Gemini would have recorded a loss of $320.33 million in the first half of 2025.

It should be noted that, although debatable, this accounting rule is perfectly legal in the United States. However, its use should make us wary of the figures that companies sometimes put forward, and it is therefore advisable to look at the fine print of balance sheets rather than just turnover and profit.