")

The race to accumulate Bitcoin continues unabated for Michael Saylor’s company in early 2026. By crossing the symbolic threshold of 700,000 BTC, Strategy reaffirms its belief in Bitcoin despite the falling price. As the market tests the $90,000 resistance level, this move raises questions about the valuation of the stock relative to the assets it represents.

Strategy further strengthens its status as the largest holder of Bitcoin

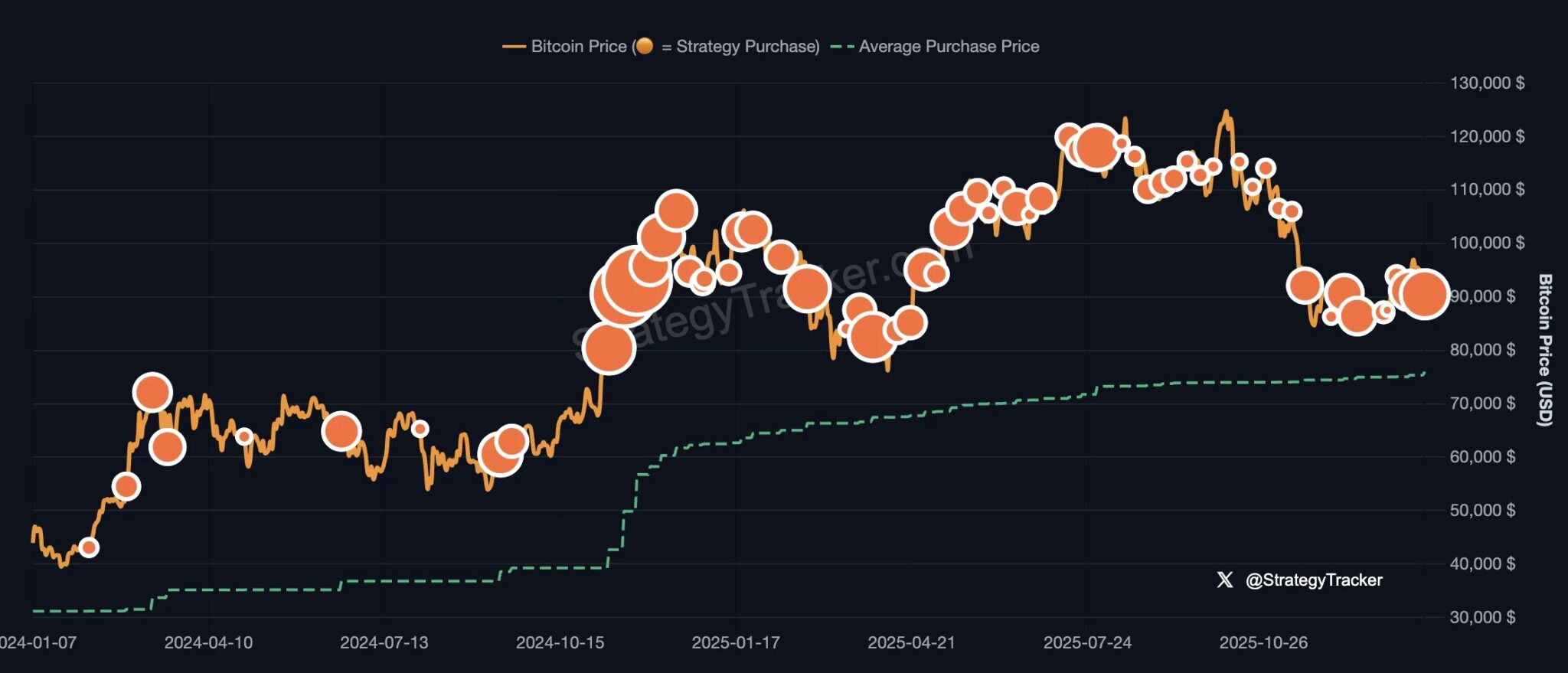

Strategy, Michael Saylor’s Treasury Company, announces the acquisition of an additional 22,305 Bitcoins for approximately $2.13 billion.

This is the largest BTC purchase made by the company since December 8, 2024, suggesting renewed confidence in the future of Bitcoin’s price.

The average execution price of this new purchase is $95,284, which is already nearly 4.5% below the current price of BTC. With this acquisition, total reserves exceed 700,000 Bitcoins to reach 709,715 BTC, acquired for a total cost of $53.92 billion, or an average price of $75,979 per BTC.

To date, this represents a total capital gain of approximately 20%, or more than $10 billion.

Based on current reserves, one Strategy share is now worth approximately 195,000 satoshis (0.00195 BTC), or approximately $176. Meanwhile, the current price of MSTR shares is hovering around $160. This discount suggests that the market is temporarily undervaluing the company relative to the value of its Bitcoin holdings. This situation can be explained in particular by the uncertainty surrounding a possible liquidation of these reserves, which could be triggered by a further decline in BTC, already down 28% since its peak in October 2025.

The risks that Strategy poses to Bitcoin and its shareholders

With more than 709,000 BTC, Strategy now controls approximately 3.5% of the total Bitcoin supply (limited to 21 million). This concentration is beginning to weigh heavily on the dynamics of the supply of Bitcoins available on the market, contributing to the rise in its price, but also posing a threat to the price in the event of a hack or forced or voluntary liquidation of reserves.

In fact, this type of company, known as a “Bitcoin Treasury Company,” acts as an indirect holding vehicle: instead of buying BTC, investors buy a share whose valuation depends largely on its Bitcoin reserves.

However, this exposure is the riskiest for several reasons. First, it constitutes an implicitly leveraged position where the volatility of BTC often has an amplified effect on the share price, which can accelerate both gains and losses.

Second, investors are not only exposed to Bitcoin, but also to business risks: management decisions, quality of execution, financing strategy, level of debt, or dilution through the issuance of shares. Added to this are regulatory and accounting risks, which may impact the company’s ability to retain, account for, or mobilize its BTC. Unlike self-custody, shareholders must trust the company’s third-party custodian, which becomes an additional point of failure: hacking, asset freezing, operational errors, or seizures.