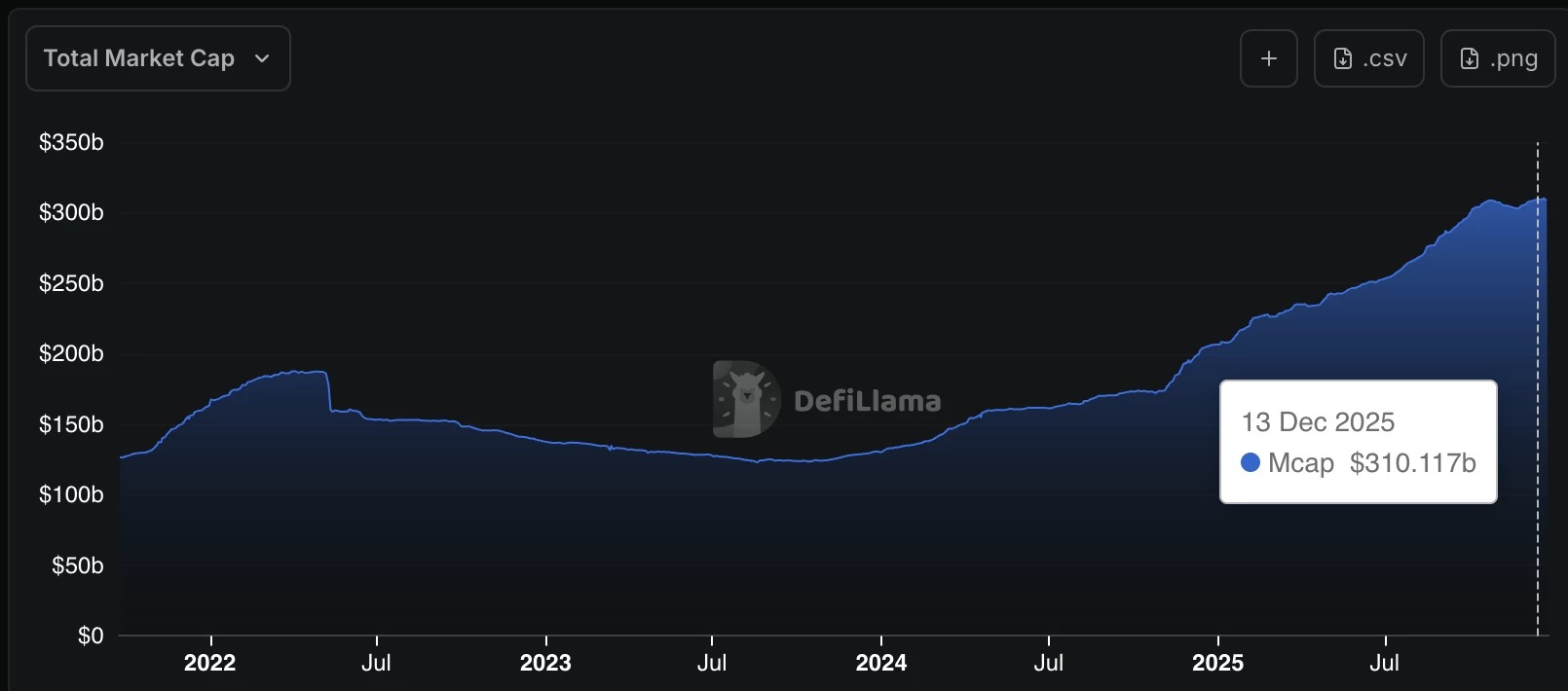

Stablecoins have reached a new high with a market cap of $310 billion. While the crypto market is struggling to find a clear trend at the end of 2025, these stable assets are confirming their central role in the ecosystem, despite sharp declines in Bitcoin and Ether.

Stablecoins exceed $310 billion in market capitalization

While the cryptocurrency market is struggling to find a clear trend at the end of 2025, the market capitalization of stablecoins continues to increase. Bitcoin, after reaching an ATH of $126,000 in October, is now hovering around $89,000, a 30% drop. Ether, for its part, made only a brief foray above its former peak before losing 40%.

The current performance of cryptocurrencies is causing frustration among investors, while equity markets, buoyed by the artificial intelligence sector, continue to rise, with the S&P 500 reaching new all-time highs and approaching 7,000 points.

But stablecoins are not experiencing a bear market.

While they fell from $187 billion in May 2022 to $124 billion in 2023 during the last bear market, their capitalization rebounded to $205 billion in January 2025. And today, it exceeds $310 billion.

While investors hoped to see the crypto market attract new capital and support the valuation of altcoins, the latter are actually struggling to capture the value actually created by the ecosystem: the tokenization of the dollar. The increase in the capitalization of stablecoins thus appears to be a direct expression of the growing use of the dollar within blockchain protocols.

The growth of stablecoins is accompanied by a new regulatory framework in the United States. The GENIUS Act, passed this summer, imposes transparency requirements on stablecoin issuers regarding reserves, regular audits, and a specific license issued by the Treasury.

Far from slowing down the market, this new regulation seems, on the contrary, to reassure institutional investors, who are attracted by this new tool that allows them to design new financial instruments. More and more institutions are expressing a desire to issue their own stablecoin, driven by strong growth in demand, but also by the profits currently being made by the main issuers.

Stablecoins are a point of systemic fragility

While stablecoins are now the driving force behind activity on smart contract blockchains such as Ethereum and Solana, their dominance raises a fundamental paradox.

Although they represent a tiny fraction of the total crypto market capitalization, they now account for most of the actual use: transfers, trading on DEXs, collateral for decentralized loans, etc. Stablecoins have become the invisible and indispensable infrastructure of liquidity.

This raises an inherent problem with stablecoins, notably USDC, USDT, and centralized stablecoins representing 98% of the market, which are issued by centralized private entities (Circle, Tether) subject to US GENIUS Act regulations, making their influence dependent on the decisions of the US regulator.

This raises an inherent problem with stablecoins: USDC, USDT and, more broadly, all centralized stablecoins, which represent about 98% of the market, are issued by private entities such as Circle or Tether. These entities are subject to US regulation, notably via the GENIUS Act, which makes their influence directly dependent on the decisions of the US regulator. This reality creates an unprecedented strategic imbalance: in the event of a blockchain fork, stablecoin issuers must choose, or be forced, to support one branch but not the other. Their choice can thus seal the fate of a network. Ironically, the more stablecoins are used, the more vulnerable the ecosystem becomes to centralized decisions.