Stablecoins are currently at the forefront of the crypto scene, since the adoption of the GENIUS Act regulatory framework in the United States. This situation has been heralded as a real starting point for their widespread adoption, unless it is just a mirage.

Stablecoins: a “marketing mirage”?

The recent adoption of the GENIUS Act regulatory framework in the United States seems to promise the liberation of the stablecoin sector far beyond the crypto sphere alone. And for good reason, as more than 99% of its currently available supply appears to be directly backed by the US dollar.

This is a situation that many companies are preparing for, both in the crypto sector and in the payment sector. The figures announced are staggering, with an estimated capitalization of $2 trillion in a few years and a payment flow capable of capturing 17% of consumer transactions—or $50 trillion annually—by 2030.

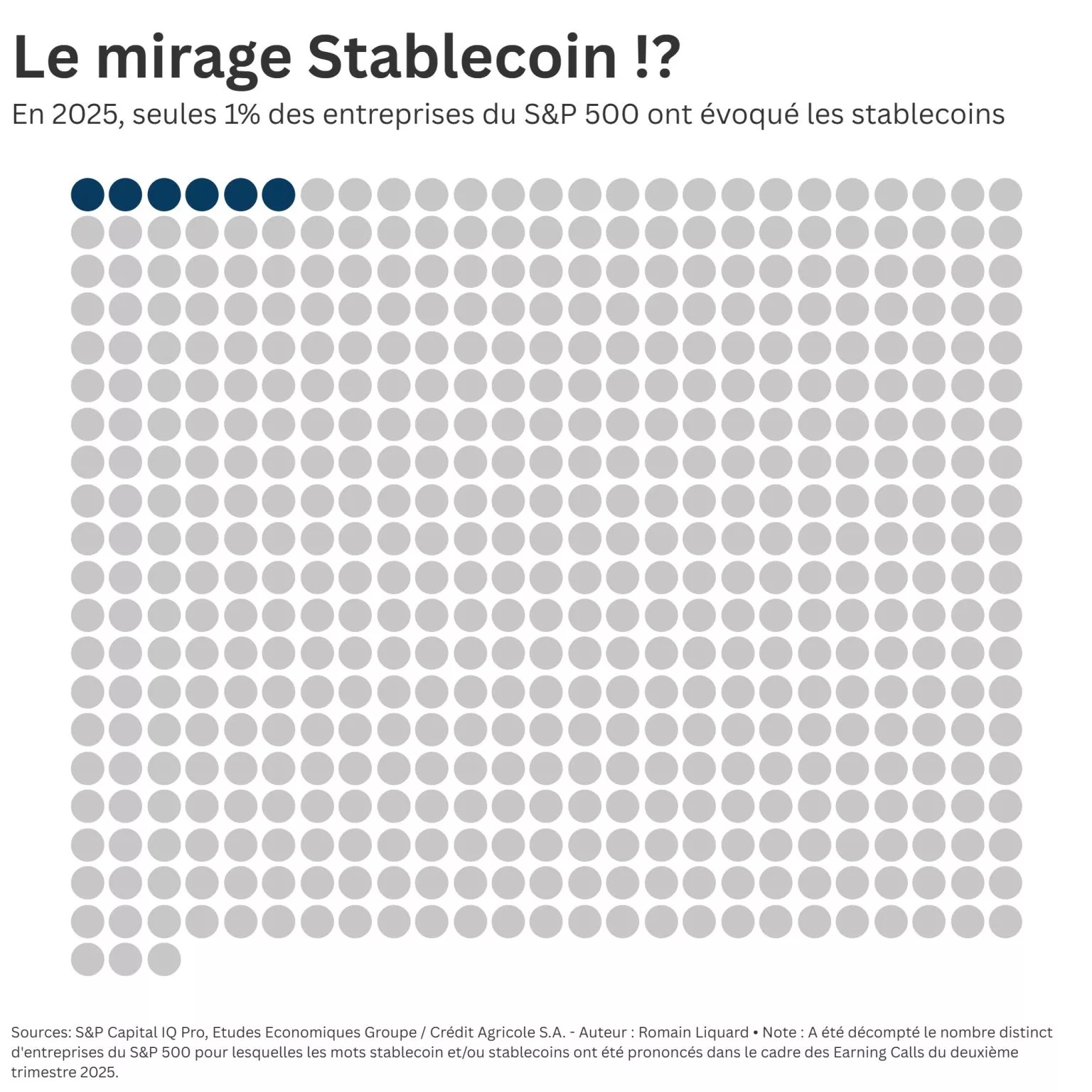

Faced with this frenzy, some analysts are trying to keep a cool head. This is the case, for example, with Romain Liquard on LinkedIn, who questions what he calls a “marketing mirage.” The origin of this questioning? The fact that “only six S&P 500 companies mentioned stablecoins in their analyst calls this year.”

If stablecoins were truly revolutionizing payments, as we are constantly told, shouldn’t we already be seeing CFOs boasting about their efficiency gains?

Romain Liquard

“Are they really circulating outside of crypto trading?”

According to data collected by Romain Liquard, only 1% of S&P 500 companies—6 out of 503—actually mentioned stablecoins in their quarterly earnings calls, which are intended to present their financial results. All of them are in the finance sector, and none are in sectors such as industry, tech, healthcare, or energy…

This observation highlights the still very intimate nature of stablecoin development, to the point of wondering whether they “really circulate outside of crypto trading,” for which they have been largely intended until now. At the same time, “are they really used for lawful international trade payments?” And “are they integrated into B2B settlements between economic agents?” “

These are all legitimate questions that remain difficult to answer, because, as Patrick Azzopardi rightly explains in his commentary on this analysis, ”stablecoins have been legal for one month in the US [and] it takes years for large banks and multinational companies to adopt plug & play technologies.”

According to Romain Liquard, the proliferation of native blockchains developed by certain stablecoin issuers—such as the leader Tether and its USDT—only serves to complicate the adoption of this payment infrastructure, which is already facing competition from certain traditional banking players.

But isn’t the game ultimately being played on a different field? With payment leaders such as Visa, Mastercard, Stripe, and more recently MoneyGram already offering dedicated stablecoin options. To the point where it is conceivable that it will soon be possible to use them for specific use cases—such as cross-border transactions—without even really being aware of it.