Berachain, the blockchain that promised to revolutionize the crypto ecosystem with its unique Proof of Liquidity (PoL) consensus, is now facing a much harsher reality. Despite a total value locked (TVL) of over $3 billion, the bubble has burst. Why such a dramatic fall?

When innovation is not enough to guarantee the success of a blockchain

In the first quarter of 2025, Berachain was something of an oddity in the blockchain ecosystem. Driven by a community fond of offbeat memes and an ambitious technical approach, the blockchain had captured attention with its new consensus mechanism: Proof of Liquidity (PoL).

This hybrid consensus promised to solve an age-old dilemma for decentralized blockchains: how to incentivize users to provide liquidity while securing the network, without sacrificing one for the other.

Where blockchains such as Ethereum and Solana reward validators for securing the network, Berachain wanted to align economic interests by directly rewarding liquidity providers.

The idea was appealing on paper:

- The more liquidity you provide, the more you contribute to the security of the network;

- The more you help decentralized finance (DeFi) applications grow, the more BERA, the blockchain’s native token, you earn.

Around this innovation, Berachain attracted a wave of DeFi projects, riding on returns of sometimes over 100% thanks to massive token issuances. This approach quickly propelled the blockchain, even reaching a record total value locked (TVL) of $3.495 billion according to data from DeFiLlama:

However, this momentum quickly ran out of steam. The descent into hell for Berachain was brutal, as evidenced by the continued decline in its TVL. Over the last 30 days, this decline has not slowed down: Berachain has lost nearly 39% of its TVL over this period.

The difference is striking: Berachain currently has only $628.7 million in TVL, a difference of $2.862 billion from its ATH.

Furthermore, it is important to highlight the significance of this key metric within the ecosystem, which is the subject of this article. As Berachain is designed around a PoL consensus, the security of the network depends indirectly on its amount of liquidity. The price of the BERA cryptocurrency is trading at around -89% of its ATH at the time of writing.

Was the fall of the BERA cryptocurrency predictable?

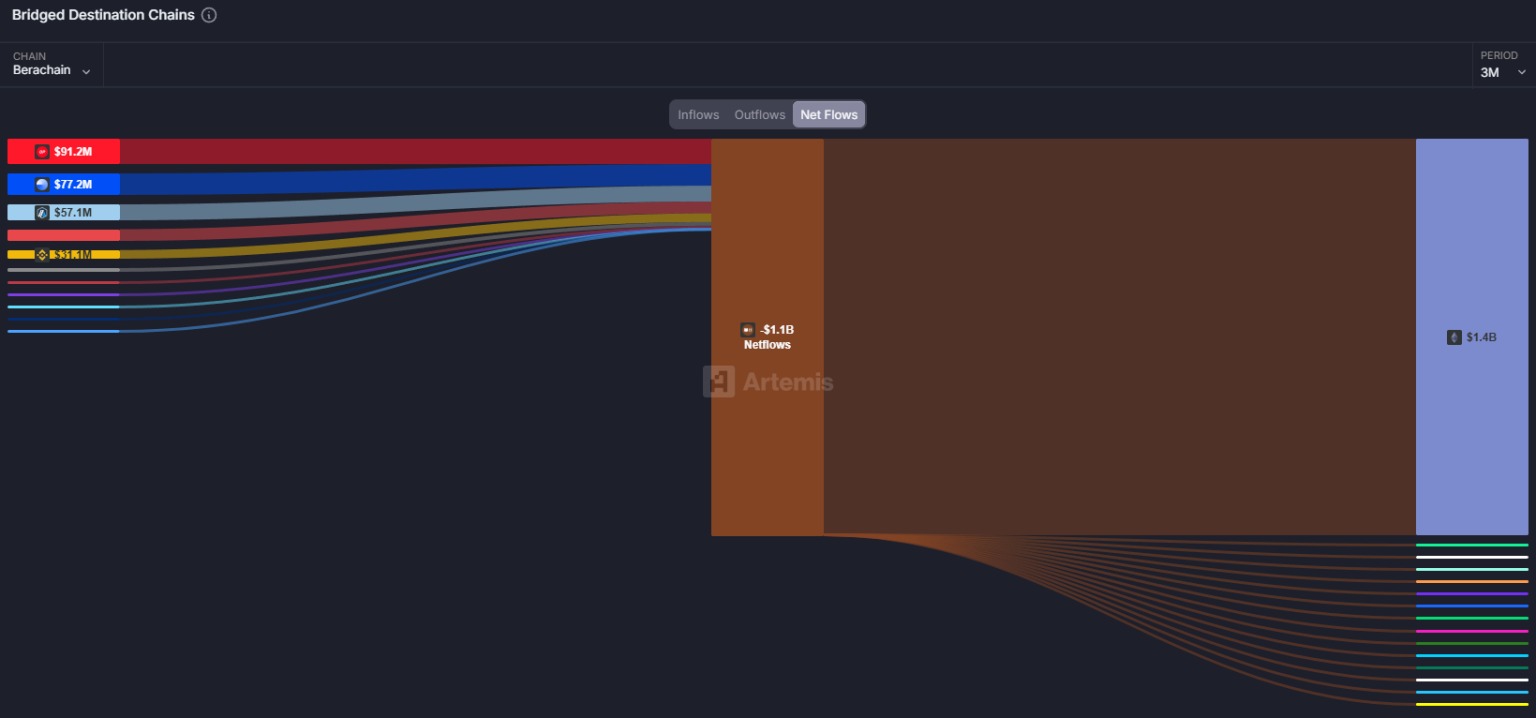

As we mentioned in our columns last April, Berachain was capturing significant capital from other blockchains (via bridges). Since then, the dynamic has completely reversed: economic incentives have been reduced, and liquidity providers—both individuals and professionals—have turned to more lucrative opportunities.

As we can see in the chart below, the Berachain blockchain has posted a negative net flow (inflow – outflow) of $1.1 billion over the last three months. In other words, more than $1 billion has left Berachain over this period in search of better opportunities:

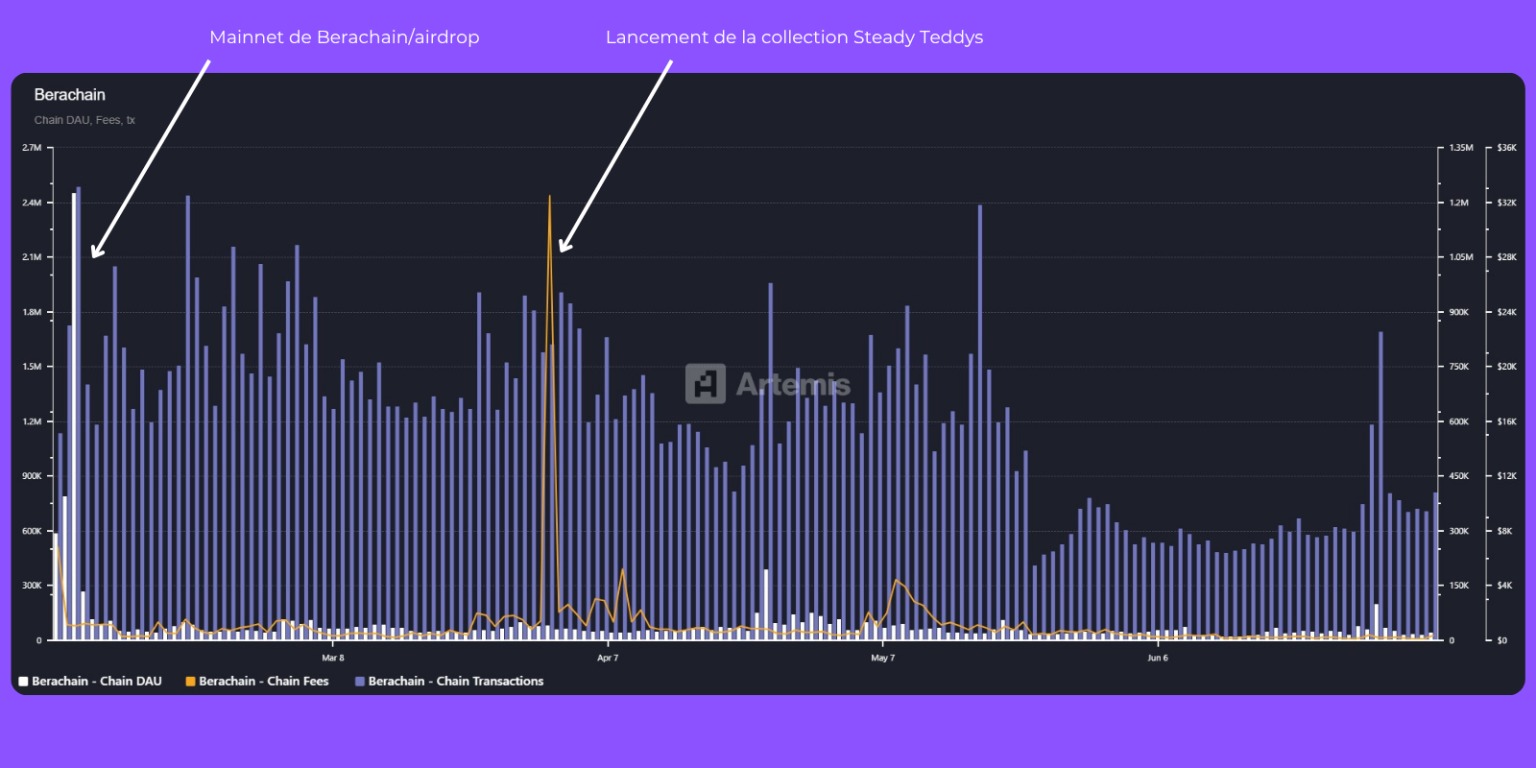

This is not the only factor that may have worked against the BERA cryptocurrency. As we already pointed out in our last article on the subject, Berachain’s on-chain activity is relatively limited.

As we can see from the graph above, Berachain’s on-chain activity has been boosted on an extremely ad hoc basis, notably:

- During the launch of the mainnet, accompanied by the BERA airdrop;

- At the launch of the Steady Teddys NFT collection, Berachain’s flagship collection.

Apart from these events (which we have indicated on the graph), on-chain activity on Berachain is very limited.

For example, Berachain generated only $111.6 in fees on July 6, which is rather alarming for the long-term sustainability of the PoL model.

Although the situation looks bleak for the future of Berachain, it is important not to count your chickens before they hatch. The pseudonymous team behind this project has raised $142 million in various funding rounds, so it is highly likely that new incentive programs will be launched in the future, capturing significant liquidity once again.

Nevertheless, the question of the sustainability of the PoL model remains open: how can a flow of liquidity be guaranteed in a situation where incentives are degraded?

As we have seen in this article, the degradation of incentives (whether at the protocol or blockchain level) frequently leads to capital flight.

It is therefore absolutely crucial for the future of Berachain to find a balance that allows it to attract liquidity again while trying to retain capital (and users) more effectively.