The capture of Nicolas Maduro by the United States is shaking up the Venezuelan political landscape, but its real impact on the oil market remains uncertain. Production, exports, stocks, and investor positioning suggest that the risk of an immediate supply shock is limited, despite already very high expectations.

Operational continuity despite the political shock

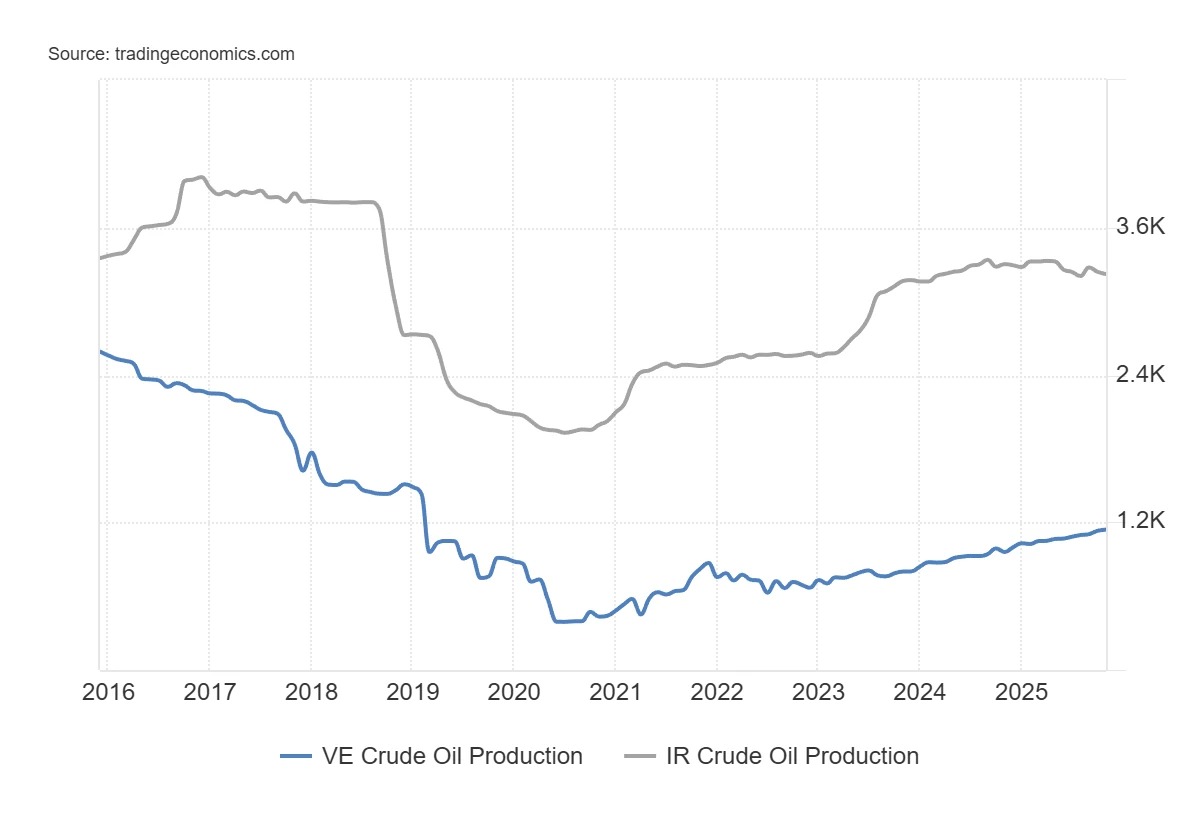

At this stage, the available data suggest continuity in Venezuelan flows. Venezuelan production fluctuates between 750,000 and 800,000 barrels per day, compared with more than 3 million in the early 2000s.

Exports remain consistent with this level, with domestic consumption absorbing a marginal share of the volumes. Onshore inventories did not show any significant variation during the rise in tensions. The net surplus observed since the beginning of the political sequence is estimated at around 100,000 barrels per day, a volume that current storage capacities can absorb for several weeks or even months. As long as these storage capacities exist, there is no immediate technical constraint requiring wells to be shut down. In the short term, a rapid interruption in flows would therefore not be the result of economic considerations, but of an operational shock: sabotage, terminal blockages, strikes, or logistical disruptions. In the absence of such events, flows will continue.

A marginal player in a well-supplied global market

Venezuela must also be viewed in a global context. With less than 1% of global production, the country no longer has the capacity to create a supply shock on its own. Its weight is incomparable to that of players such as Iran, which controls around 3% of global production and 25% of maritime oil trade in certain sensitive areas.

This interpretation is consistent with investors’ current positioning on oil. CFTC data show that systematic managers and follow-up funds are currently holding particularly high short positions. The share of net short positions held by managed money is at levels rarely seen since the late 2000s. In other words, much of the negative scenario is already priced into portfolios.

Conversely, commercial hedgers (players directly exposed to physical flows, such as producers) have gradually reduced their short positions and are approaching levels historically associated with low oil prices. This type of divergence between highly short speculators and more constructive hedgers generally appears when the market anticipates an abundance of supply that is slow to materialize. The positioning does not signal an immediate reversal, but it suggests that the bearish consensus is based more on expectations than on an observed deterioration in flows.

This configuration explains why prices may remain insensitive despite the enormous potential. The global oil market is currently evolving with comfortable overall inventories and supply dynamics that go far beyond the Venezuelan case alone. In recent weeks, global onshore inventories have even been in demand, with accumulation in China and drawdowns observed on the OPEC side.

Anticipated return of supply and structural limitations of Venezuelan crude oil

In the short term, the political turmoil in Venezuela may even fuel expectations of a surplus. The prospect of sanctions being eased or stocks being released is fueling the idea of a future influx of barrels. Some analysts are talking about tens of millions of barrels that could potentially be mobilized. However, this reasoning is based more on political assumptions than on industrial capacity.

In fact, much of Venezuela’s oil is extra-heavy crude, with higher gravity, higher sulfur content, and higher metal concentrations than in the rest of the world. This type of oil cannot be produced or exported without diluents, mainly condensate, which must be imported. At this stage, there are no clear signs of a significant recovery in these imports. In other words, without these diluents, Venezuelan production remains capped. In the long term, the figures also call for caution. Since 2010, annual increases in Venezuelan production have never exceeded 420,000 barrels per day, while some phases of decline have reached nearly 800,000 barrels per day. Envisioning a sustainable increase of more than 500,000 barrels per day per year would require a radical change of course. Such a shift would require massive investment. Estimates exceed $110 billion for exploration and production, to which approximately $50 billion would need to be added for ports, pre-refineries, and transportation infrastructure. However, with oil prices below $60 per barrel, the economic incentive is weak, especially in an unstable political environment. If these investments are delayed, expectations of a rapid return of supply are likely to be revised downward.

Severe structural constraints and highly targeted opportunities

These constraints are reflected in the analysis of companies in the sector. Venezuela has a number of deterrent factors: a history of expropriation, legal uncertainty, corruption, heavy bureaucracy, and degraded infrastructure. The very nature of the reserves, which are mainly heavy crude, further increases the cost and complexity of projects. Under these conditions, a massive influx of foreign capital remains unlikely unless there is a radical change in the country’s institutions and an increase in oil prices. Nevertheless, some companies have specific exposure. Chevron (CVX), already present in the country, could benefit from targeted commercial licenses granted by the US authorities. The Franco-American company Schlumberger (SLB) is naturally positioned when it comes to maintaining or refurbishing existing facilities, without necessarily committing heavy capital in the long term. The expropriation of its assets in 2007 gives it unique legal leverage in a context of transition. A government seeking to restore its international credibility could be inclined to settle certain emblematic disputes in order to send a signal to investors. In this specific case, the issue is not a rapid increase in production, but the recognition of a historical liability.

In conclusion, Maduro’s capture profoundly changes the Venezuelan political landscape, but its implications for oil will depend on very concrete factors that are unknown at this time: continuity of flows, availability of diluents, infrastructure security, and the ability to attract capital in a credible environment. As the market is already anticipating a return of supply, the real risk is not a pleasant surprise in terms of production, but rather that the expected increase will be slow to materialize.