")

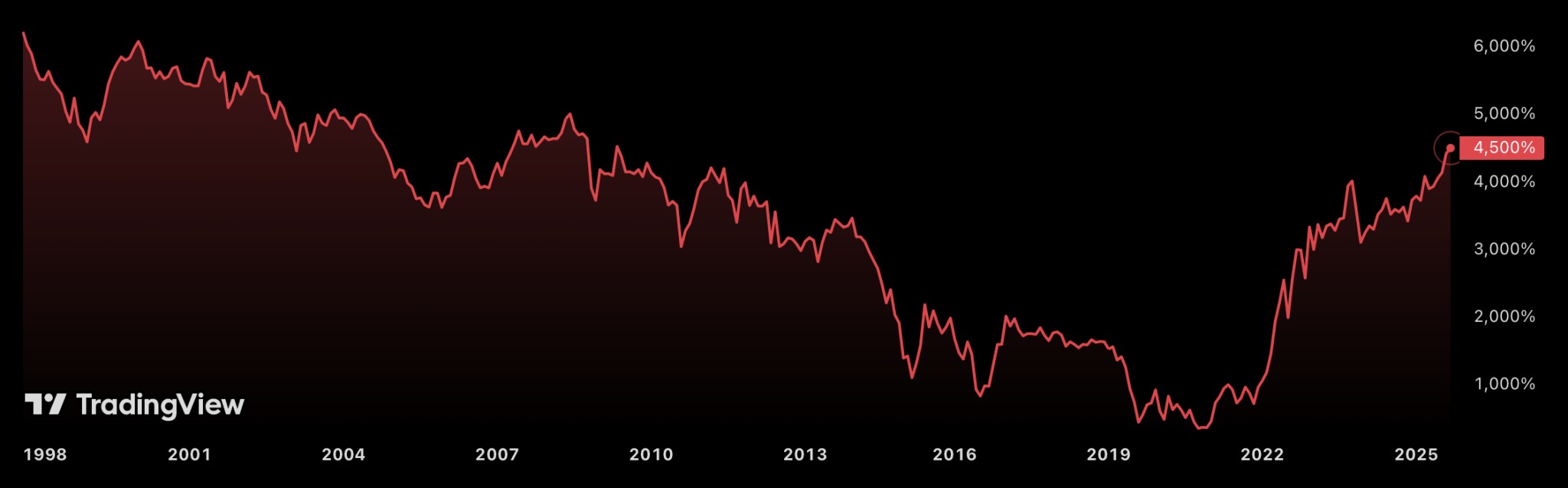

The French government is once again embroiled in a political crisis following the confidence vote requested by the Prime Minister in order to push through his austerity budget, which has been rejected across the board. As a result, the French debt rate has reached 4.50%.

French debt rate reaches 2009 levels

Since presenting his austerity budget aimed at reducing public debt, Prime Minister François Bayrou has found himself in a difficult position. His controversial proposals to save €44 billion—including the elimination of public holidays—have been criticized even within his own coalition.

This situation puts the head of government in the hot seat, with the prospect of a new government crisis similar to that of his predecessor, Michel Barnier, whose government fell victim to a motion of censure passed last December.

In this unfavorable context, the public debt market is sending out a clear warning signal, with the yield on 30-year French bonds returning to 4.50% on Tuesday, September 2. And with good reason: in times of political instability, the markets demand higher interest rates to lend to France, as they perceive a greater risk.

Why is this threshold important? Because it seemed to be a thing of the past since 2009 and the consequences of the subprime crisis, now 16 years ago. As a result, France will now have to pay more to borrow in the long term. And the situation on the 10-year market is not really any better (3.58%).

The same situation for other countries

According to data published by Reuters, France is not the only country experiencing this rise in borrowing rates. The UK is also recording a historic high not seen since 1998, following the reshuffle of Prime Minister Keir Starmer’s economic team just before the autumn budget was announced.

The situation is similar in the United States, where Donald Trump’s relentless attacks on Fed Chairman Jerome Powell pose a persistent threat to the institution’s independence. As a result, US 30-year bond yields have once again reached 5%.

According to data from the Banque de France, interest on the national debt currently amounts to an estimated €55 billion—9.5% of the state budget—payable each year. This figure could reach more than €70 billion in 2027, without even taking into account the current rise in interest rates.

This rise in yields on French bonds risks further weakening household purchasing power, with the prospect of higher bank lending rates and less business investment. At the same time, it weakens the entire eurozone, which is already in a difficult position.