")

As Layer 2 networks multiply on Ethereum, a question resurfaces: is their development really justified? Behind the promise of scalability, many projects are struggling to generate sustainable activity or concrete revenue.

Several major DeFi players, including Aave and Curve, are now questioning the relevance of maintaining costly deployments on these low-traction networks. Investigation.

One hundred and fifty-five: that’s the number of layer 2s currently deployed, according to data from L2BEAT. It’s a staggering number that reflects a problem everyone sees but no one talks about: the saturation of these blockchains built on Ethereum, most of which have nothing special to offer.

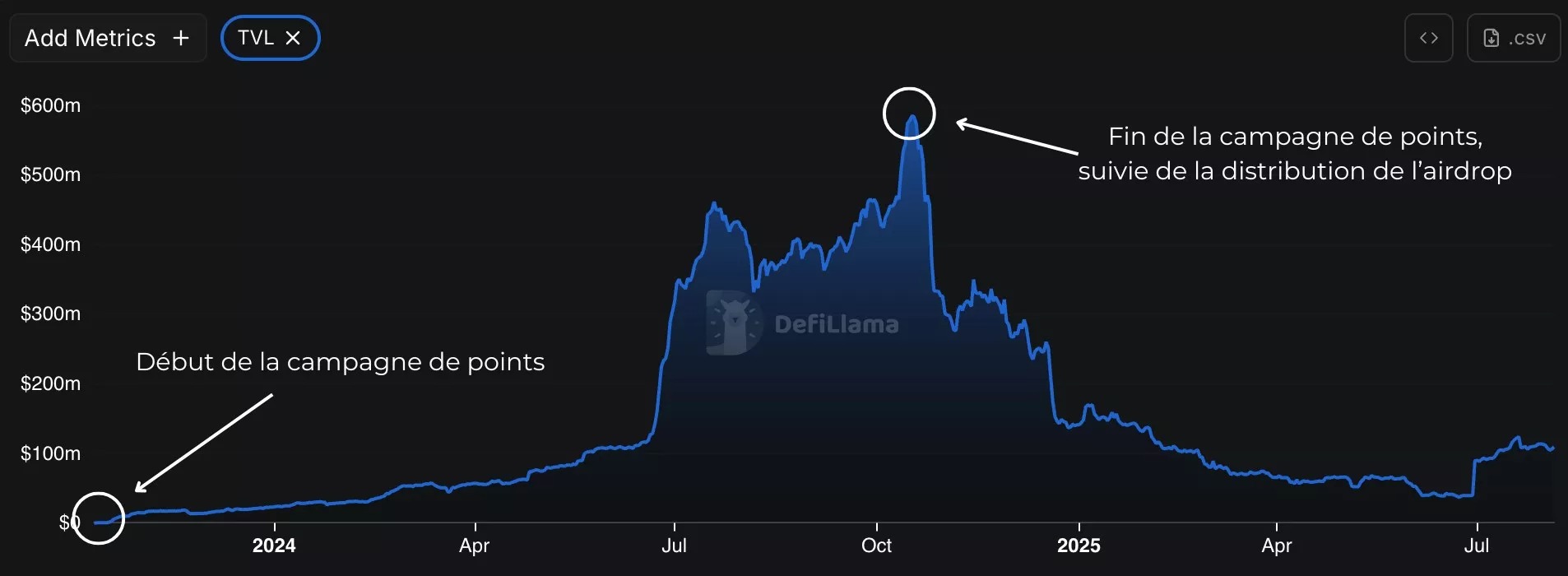

Often, when a layer 2 is launched and wants to get noticed, it conducts an airdrop. Whether official or not (mostly via a points system), this airdrop attracts investors and, therefore, liquidity. And liquidity means revenue. Generally speaking, layer 2s are launched with a few basic applications: bridge, swap, DEX, etc.

Apart from the points system, which directly translates into a speculative promise, investors will prefer to use an application for its place in the ecosystem (reliability, seniority, resilience, etc.) and for the tools it offers. In a given ecosystem, there are often several applications performing the same role (sometimes a dozen or more), which is why the adage “first come, first served” is particularly true in decentralized finance (DeFi).

For an application to work, it needs liquidity.

And this liquidity, outside of layer 2 itself, is provided by users. That’s why the faster an application makes a name for itself in a new ecosystem, the more investors it will attract.

The more investors a protocol attracts, the more liquidity it has available, and therefore the more volume it has. This gives it high visibility and creates a virtuous circle. That’s why multi-chain DeFi applications, which are worth billions of dollars, want their share of the pie: there’s no way they’re going to miss out on the next promising layer 2 and its potential millions of dollars in revenue. And that’s where we enter a game of heads or tails.

Heads, layer 2 continues its rise and manages to carve out a permanent place for itself in the ecosystem; tails, it collapses, like most projects before it after distributing their airdrop.

The airdrop has been distributed, investors have taken their profits, and Layer 2 now has nothing left to offer. At the time of writing, the overwhelming majority of layer 2s have very low activity (whereas it was significant in the pre-airdrop period), with the exception of a few such as Arbitrum, Optimism, Base, and Unichain.

As a result, applications deployed on these same layer 2s find themselves with rapidly declining activity, even reduced to almost zero in the worst cases, and eventually see their revenues plummet. But keeping an application operational on a layer 2 comes at a cost, particularly to pay developers who must constantly provide updates.

Will the largest DeFi protocols eventually abandon layer 2?

The relevance of deploying DeFi applications on new layer 2s is now being questioned. In some cases, abandoning certain ones is even being considered, as the development cost/revenue ratio is so poor.

This situation was highlighted by Marc Zeller of the Aave Chan Initiative (ACI) on the governance forum of Aave, the largest protocol in the lending ecosystem, regarding a deployment on layer 2 BOB, a hybrid ZK combining Bitcoin and Ethereum.

Seven months after this governance proposal was initiated, the ACI has seen little growth in the BOB ecosystem. The Aave DAO has been too lenient in the past with deployments on new networks and is currently operating at a loss on several of them (Soneium, Celo, Linea, Zksync, Scroll). The competitive landscape includes low-quality CeDeFi platforms such as Avalon Labs and Euler, which are seeing almost zero traction.

Not enough to cover operating costs, according to Marc Zeller, which amount to at least $1 million annually:

Based on current data, and even with optimistic growth projections, the ACI believes it is virtually impossible for the DAO to generate at least $1 million in annual revenue from this instance, which we consider the bare minimum to add a new network to manage and oversee.

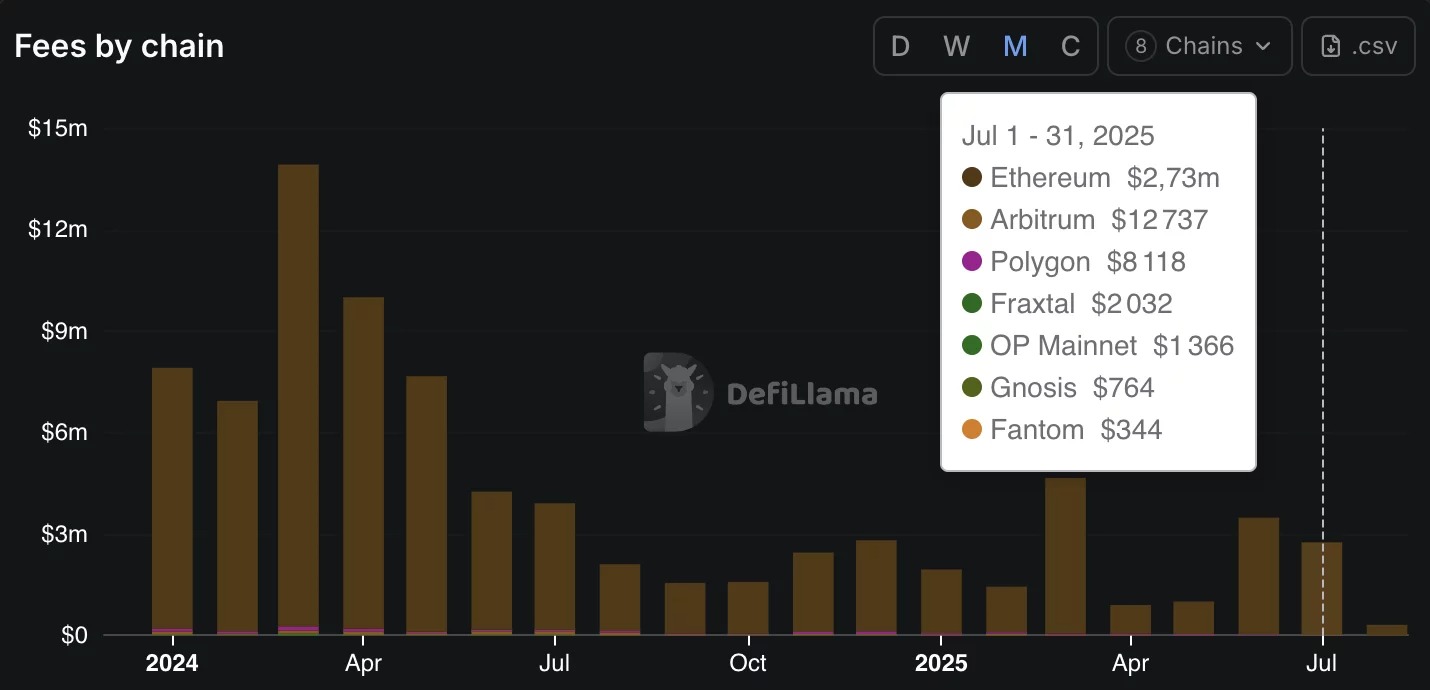

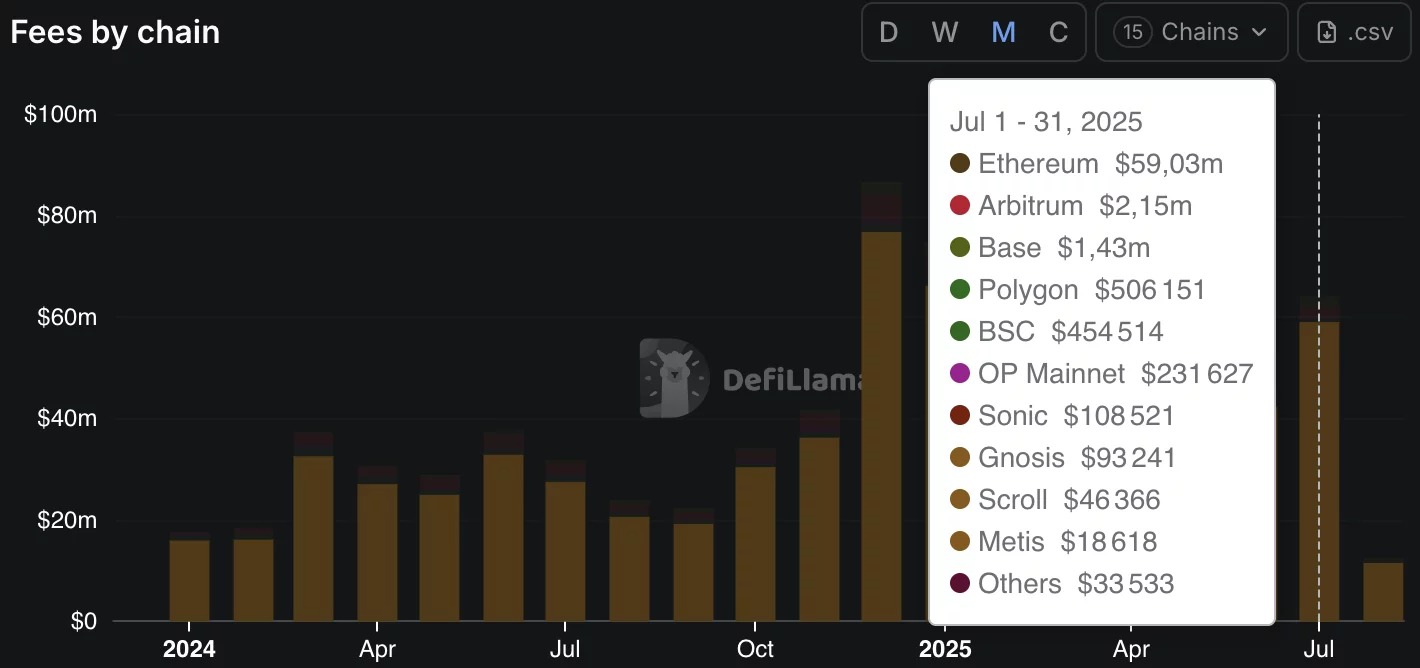

Here, Marc Zeller referred to operating at a loss on a few layer 2s, notably Soneium, Celo, Linea, Zksync, and Scroll. Indeed, looking at the layer 2s that generate the most revenue for Aave, we see that only a few are interesting in this regard:

As we can see, the overwhelming majority of Aave’s revenue comes from layer 1, namely Ethereum. The same is true for Curve, another long-standing protocol in the crypto ecosystem. Here too, the issue was raised in a post on the project’s governance forum:

L2s consume the time of talented developers. Each of these blockchains requires at least as much attention as Ethereum, while generating very little revenue. By halting all development in this direction, Curve can regain the mental space it needs to focus on more fruitful avenues. […] Bringing Curve to L2s has already been attempted, but the numbers speak for themselves.

Very little feedback (around $1,500 per day, all L2s combined) while consuming a lot of development time.

However, the Curve team does not seem ready to take the plunge. Responding to the discussions generated by the forum proposal, it admitted that it would not “take this decision”:

Interesting discussion about L2s. Let’s be clear: this message does not come from the team currently working on Curve, and no one on the team agrees with it (so we will probably not be going in this direction).

In any case, it is more evident than ever that, faced with this ocean of Layer 2 solutions with no added value, decisions will have to be made to ensure the sustainability of certain protocols.

As the Layer 2 landscape fragments, one thing is clear: experimentation has reached its limits.

What was once innovation is now, too often, meaningless duplication. Faced with a market where resources are limited (human, technical, financial), legacy protocols will have to make clear strategic choices: continue to spread themselves thin across Layer 2 solutions with no traction, or refocus their efforts on solid, sustainable, value-generating environments.