The cryptocurrency sector regularly wonders what forms its adoption might take. This question has recently been raised again in relation to the United States, given data from 2023 that leaves little room for monetary use cases. Will things change with the arrival of Donald Trump?

In the United States, crypto remains a gamble, not a currency

Since the Trump administration arrived at the White House, the United States has undergone a regulatory revival with regard to the handling of cryptocurrencies. This momentum has been greatly accelerated by President Donald Trump himself, who wants to make his country the new global capital in this field. But behind the intentions, it is still necessary to monitor the figures. This is a way of taking stock of the situation in order to have an effective point of comparison when all the US regulatory frameworks related to the cryptocurrency sector come into effect.

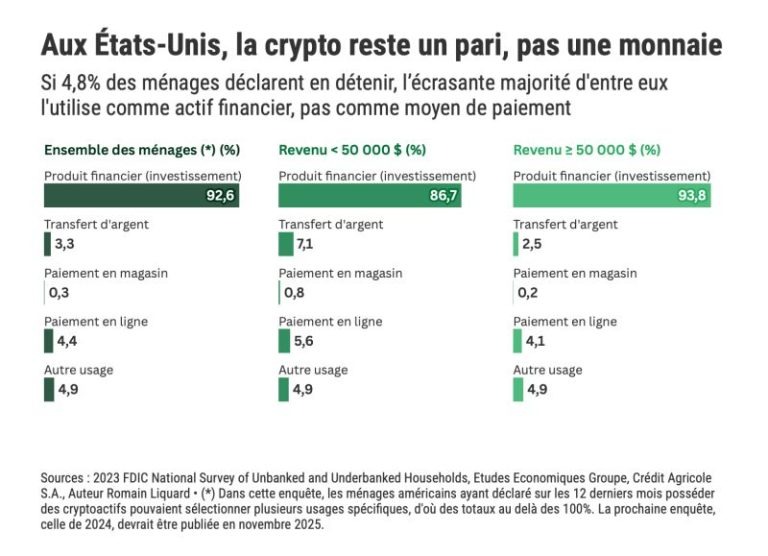

An exercise conducted by Romain Liquard on LinkedIn to measure the actual use cases of these crypto-assets in the habits of American households that own them, which represent 4.8% of the total population, according to data from a 2023 study.

And the least we can say is that their use applies almost exclusively to the field of investment, across all social categories.

The only real exception is lower-income households, 7% of which use cryptocurrencies for money transfers. It is difficult not to imagine a significant proportion of cross-border transactions intended to send money to certain emerging countries due to the low cost of this type of transaction compared to traditional offerings.

Cryptocurrency payments are struggling to gain acceptance

The big omission from this graph is the monetary nature often associated with cryptocurrencies. One of the main reasons for this is the predominance of the dollar as the national currency, which is powerful enough that there is no need to look for anything else—just as in Europe with the euro.

Once again, the poorest populations make more frequent use of cryptocurrencies for payments, even if this remains below 1% in stores and 6% on the Internet. At the same time, the conclusion of the latest FDIC National Survey clearly indicates that “cryptocurrency use was higher among banked households (5%) than among unbanked households (1.2%).”

However, one piece of data seems essential to take into account, given the proven weakness of payments made in cryptocurrencies. Indeed, the recent adoption of the GENIUS Act regulatory framework could well unlock the monetary potential of stablecoins—more than 99% of which are backed by the US dollar—within the United States and even beyond.

The next FDIC National Survey report is due in November for the year 2024. This will be an opportunity to measure the initial consequences of Donald Trump’s election, following his pro-crypto campaign. Will cryptocurrency payments become more widespread? Watch this space…