In an unstable economic and political climate, young people in France will have to find new reference points to navigate the turmoil. What if Bitcoin became a way out for this new generation, faced with a system that is losing its meaning?

An uncertain climate: where is France headed?

The Patrimonia trade show, France’s largest event dedicated to wealth management professionals, was held at the end of September. On this occasion, we wanted to address the following question: Is Bitcoin becoming the investment of choice for the new generation in France?

This question seems relevant to us, given several signs that appear to be taking hold:

- Real estate crisis: Since the beginning of 2025, the real estate market seems to be regaining some momentum. However, this rate of growth should be put into perspective, as it is based on the particularly low levels seen at the beginning of 2024, according to the Crédit Logement/CSA barometer. The end of the MaPrimeRénov’ scheme in June also slowed down buyers. With an average interest rate of 3.08%, conditions remain unfavorable, particularly for first-time buyers.

- Debt, a double sword of Damocles: Poor budget management, combined with rising interest rates, is weighing on the French economy by increasing the debt burden.

- Reputation downgrade: In addition, the rating agency Standard & Poor’s downgraded France’s sovereign rating twice in 2024, from AA+ to AA and then to AA-. This situation is pushing bond markets to demand a higher risk premium, reflecting their doubts about the sustainability of public debt.

- A cloudy political horizon: Political instability and the lack of a budget agreement are blocking investment and paralyzing the economy. Businesses are operating in a climate of uncertainty, while public administrations are seeing their room for maneuver reduced. INSEE also forecasts an increase in the unemployment rate to 7.7% by the end of 2025.

- Household confidence in free fall: According to Dorian Roucher, head of the economic trends department at INSEE: “Real wages are still below their 2021 level.” He estimates that they have recovered only half of the 3 points lost during the inflationary crisis. In reality, gains in purchasing power are mainly driven by pensions and social benefits. The latest INSEE survey, published on Friday, May 23, shows a further decline in household confidence. Households feel that their financial situation is deteriorating and believe that now is not the right time to make major purchases.

So, in this uncertain economic climate, how is the younger generation adapting? How can they build their future on such unstable foundations?

Bitcoin adoption still marginal in France

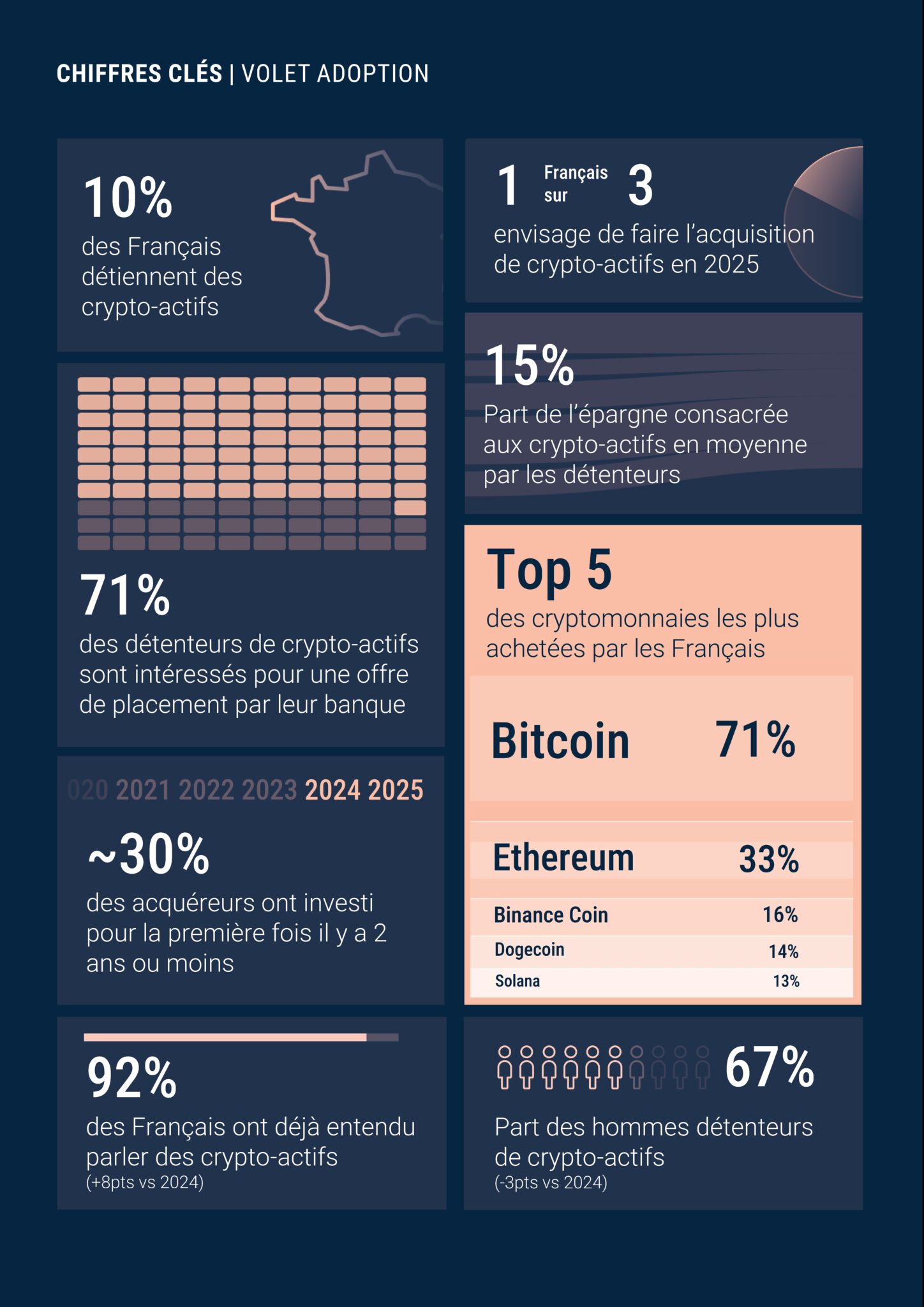

After three years of continuous growth, the ADAN’s 2025 report shows that the adoption of cryptocurrencies is stabilizing. This year, 10% of French people say they own cryptocurrencies, compared to around 12% in 2024, or nearly 5.5 million people.

Despite this slowdown, interest remains high, with one in three French people planning to invest in cryptocurrencies in 2025. This renewed interest is based in particular on a marked preference for Bitcoin, which alone accounts for 71% of the assets held by French people. However, as the study points out, “the transition from curiosity to actual use remains limited.”

The typical profile of the crypto investor remains largely unchanged: predominantly male (67%), young (42% are between 18 and 34 years old) and wealthy (45% are in the upper socio-professional categories). . One-third earn more than €48,000 per year, but 42% report less than €30,000, showing a certain diversity of profiles.

However, caution prevails, with 64% investing less than 10% of their savings, for an average amount of between €3,116 and €3,922. Two-thirds live in rural areas, confirming that adoption is nationwide and not exclusively urban.

A generational break with traditional assets?

The younger generations did not experience the “golden years” of their parents, marked by historically low interest rates, still affordable real estate prices, and dynamic economic growth.

Thus, even if “real estate remains a safe haven,” as explained in the introduction, it is becoming unattainable for a large proportion of first-time investors. The dream of home ownership, long at the heart of the French ideal of wealth, is crumbling. Younger generations, particularly those between the ages of 18 and 34, are struggling to envisage themselves buying property.

In this context, it might be logical to see a shift towards alternative assets that are more liquid, more mobile, and more in tune with the digital lifestyle of this new generation.

The crypto sector is gaining ground, thanks in particular to the emergence of new, simpler access channels that are integrated into the habits of younger generations. Revolut, for example, is now the second largest crypto acquisition platform in France, used by 24% of holders. However, as Thierry Lobjois, commercial director of Paymium, explains:

The vast majority of young people have not yet built up any wealth, so they are not particularly interested in investing. On the fringes, they are looking more at new digital assets, without understanding them. For the vast majority, crypto trading cannot be equated with investing, but rather with gambling.

French institutions paralyzed despite pressure from customers

According to Thierry Lobjois’ observations following the Patrimonia trade show, “the approach to Bitcoin/crypto remains very timid, even though retail demand is growing stronger.”

Several issues underlie this observation:

- Today, no French institution offers Bitcoin. As Paymium’s sales director explains, “this is specific to France, because in Spain, offers are coming or are already there, as at BBVA. Germany and Italy should not be far behind. Once again, we risk being the last.”

- Wealth management advisors (CMAs) also appear to be technically overwhelmed, “they don’t understand the subject and don’t know how to deal with it.”

- As Thierry Lobjois points out, traditional intermediaries (banks, insurance companies, management companies, etc.) do not offer this type of service. WPs therefore find themselves isolated in the face of demand that they cannot meet.

- The MiCA regulation also represents imperfect compliance, as it is criticized by the crypto industry as “costly, complex, time-consuming, and with limited short-term benefits.” This essential accreditation for trust remains an obstacle, since as of March 1, 2025, there are 105 registered PSANs in France, but only four accredited ones.

One cannot help but draw a striking parallel between the timid reception given to Bitcoin in France today and the rejection of the Internet by institutions in the 1990s.

The Théry report, commissioned by the Balladur government in 1994, is often cited as a symbol of this strategic error. It claimed that the internet, because it was decentralized and uncontrollable, had no future in France. The report therefore advocated continuing the development of Minitel. This is how France missed the digital revolution and fell considerably behind the major technological powers. As Thierry Lobjois so aptly put it: “Let’s hope that foreign pressure will speed things up!”

What future for Bitcoin in young people’s assets?

As Thierry Lobjois observes, to date “the vast majority of young people have not yet built up any assets and are therefore not very interested in investing.” However, there is strong latent growth potential, as 33% of French people say they want to buy crypto in 2025.

Despite a regulatory framework that is stabilizing, pressure from the “mobile first” generation could well push banks and their intermediaries to take an interest in financial investment offers in cryptocurrencies.

At the Patrimonia trade show, Paymium’s sales director noticed a clear change in attitude among the wealth management advisors visiting their stand. Compared to 2024, the discussions revealed clearer motivations and significantly more serious ambitions.

For Thierry Lobjois, BlackRock and its Bitcoin ETF will play a catalytic role in the coming years. With more than $150 billion in assets under management in Bitcoin ETFs in the United States, this pressure from abroad should push the major French players to accelerate their integration, lest they find themselves left behind.

In 2025, Bitcoin is still far from being the benchmark asset for the new generation. For some, it arouses mere curiosity; for the majority, who are still poorly informed, it remains a tool for speculation, and only a minority see it as a genuine asset of conviction.

But the road to understanding Bitcoin is long and fraught with pitfalls. In countries such as Argentina and Iran, where adoption has accelerated under the pressure of economic crises, the urgency has led to a rapid appropriation of its usefulness (protecting savings, circumventing restrictions, regaining a form of financial freedom).

Conversely, in relatively stable countries such as France, Bitcoin is still perceived as a luxury product, a tool for personal sovereignty and transparency, rather than an immediate necessity.

But that is the strength of Bitcoin: it does not impose itself, it offers itself. And when the need becomes a necessity, it will offer itself as a credible alternative to those who are ready to accept it.