Is the development of restaking through the EigenLayer protocol threatening Ethereum’s security? Could the Renzo protocol’s setbacks be the first tremor heralding a much more devastating earthquake for the Ethereum ecosystem? We take stock in this dossier.

Renzo’s ezETH goes off the rails

Here’s an event that’s likely to add fuel to an already raging fire. On Wednesday April 24, the Renzo protocol liquid restaking token (ezETH) broke away from the price of Ether (ETH), the asset to which it is supposed to be anchored.

With over $3 billion in assets locked up on its platform, Renzo is one of the leading liquid restaking protocols. Simply put, it allows investors to gain exposure to the EigenLayer platform while benefiting from a liquid asset, i.e. one that can be used in other decentralized finance (DeFi) applications.

Thus, users can deposit ETH on the protocol and receive ezETH in return, symbolizing the proof of their deposit. The latter is logically supposed to have a value perfectly equal to that of the underlying asset, the ETH, which ceased to be the case for a few hours on Wednesday.

According to on-chain data, the price of ezETH fell sharply in relation to the price of Ether, sometimes as low as $700. Since then, Renzo’s liquid restaking token has recovered most of its anchor.

Evolution of the ezETH/USD pair (1-hour data)

However, this unexpected event led to a huge number of liquidations on the decentralized finance protocols on which investors had placed their ezETH tokens in risky strategies, notably Pendle or Gearbox.

A cascade of liquidations

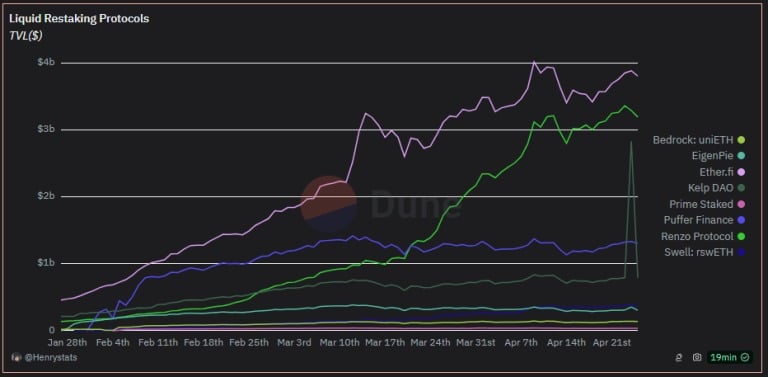

To understand how this event came about, it’s essential to look at liquid restaking protocols. At the time of writing, Ether.fi is the largest of these, capturing the majority of investors’ capital.

TVL of the main restaking protocols

To stay in the race for the top spot, competitors like Renzo have to employ a variety of strategies. The first of these is to block the possibility of exchanging ezETHs for 1-for-1 ETHs directly on the protocol, thus forcing users to hold on to their tokens for longer.

The second is to offer more possibilities with the ezETH token. For example, Renzo has focused on composability with other protocols such as Pendle or Gearbox, enabling investors to deposit their tokens in liquidity pools with strategies offering returns of several tens of percent.

However, this strategy is not without risk. As long as parity between ezETH and ETH is assured, these leveraged positions do not present any major dangers. However, when the ezETH began to detach, some high-risk positions were liquidated, leading to forced selling and a fall in the share price, which in turn led to further forced liquidations.

This is what we call a downward spiral, or more commonly in cryptocurrency parlance, cascading liquidations. That’s why ezETH’s price has plummeted so.

Renzo’s mismanagement

A little background on EigenLayer

However, there’s a brick missing from this explanation. How did the ezETH token begin to detach itself from its Ether anchor? Surprising as it may seem, the trigger was Renzo’s announcement of the launch of the REZ token and an airdrop to the community.

1/ We are excited to announce that April 30th, 2024 will be the beginning of the decentralization of the Renzo Protocol.$REZ

Full details in the post below: pic.twitter.com/jQ7pFStsM4

– Renzo (@RenzoProtocol) April 23, 2024

While this announcement may seem positive at first glance, it was not at all so in the eyes of users. According to them, the distribution of REZ tokens was not at all favorable to the community, particularly in comparison with the weight of Binance’s launchpool or the project team and private investors.

To understand this, let’s return to the deeper reasons for user disinterest. In reality, we need to understand that the EigenLayer protocol is particularly popular at the moment. The potential airdrop, reinforced by the points system awarded daily according to activity, is fuelling investor enthusiasm.

Added to this is the fact that Liquid Restaking protocols offer a doubly attractive opportunity: to accumulate EigenLayer points and points from their own protocol, potentially offering a second airdrop. In other words, users can benefit from 2 airdrops simultaneously by participating in these protocols.

The trigger: a derisory airdrop

However, the value of points remains the crucial element that binds users to the protocols. Until the project team officially announces the details of the airdrop and the value of the points, uncertainty remains: what are they worth, and is it really profitable? In the case of Renzo, the announcement of a derisory airdrop for users provided an answer to this uncertainty.

Faced with this disappointment, many users opted to retire their ezETHs, in favor of other protocols. However, Renzo does not allow native withdrawals, forcing users to turn to the secondary market to exchange their tokens.

This chain reaction led to a significant drop in the ezETH price. In the absence of Renzo’s natively-integrated arbitrage facility to stabilize prices, ezETH became a simple token on the secondary market, subject to the fluctuations of supply and demand. Unfortunately, in this scenario, supply far outstripped demand.

The wave of disgruntled users caused ezETH’s share price to start falling, triggering the famous liquidation spiral we mentioned earlier in this article, further exacerbating the downward pressure on the market.